The semiconductor industry has surged alongside the rise of artificial intelligence (AI), positioning companies like Arm Holdings (NASDAQ: ARM) to benefit from increased demand.

Known for its energy-efficient chip designs, Arm dominates the mobile device market and is now seeing heightened interest in its architectures as power-intensive AI applications continue to rise.

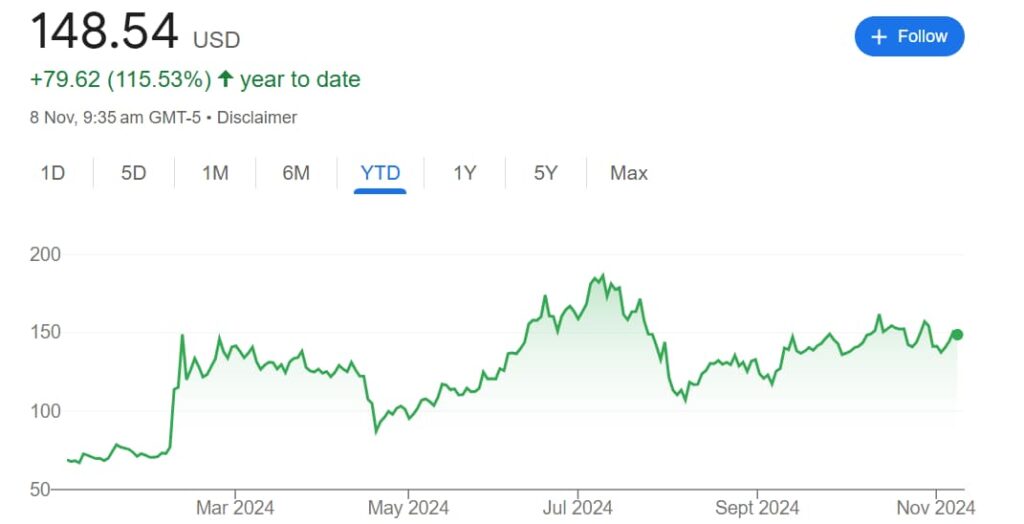

ARM, currently trading at $148 with a year-to-date gain of 115%, reflects the appeal of its expanding role in this AI-driven environment.

Q2 performance and market reaction

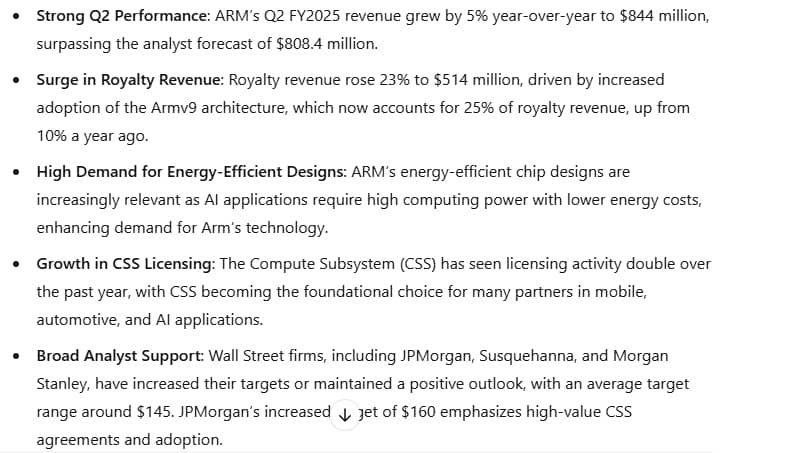

In its Q2 FY2025 report, Arm Holdings posted solid results, with revenue growing 5% year-over-year to $844 million, surpassing analyst expectations of $808.4 million.

Royalty revenue emerged as the key driver, increasing 23% to $514 million, spurred by the increased Armv9 penetration in smartphones. This contributes 25% of the company’s royalty revenue, up from 10% in the same period last year.

For context, Arm generates revenue by licensing its technology and collecting royalties on every device sold that utilizes its designs. With the surge in AI-driven demand, these revenue streams are expected to see significant growth.

However, Arm’s license revenue declined 15% to $330 million, which the company had anticipated due to the timing of high-value licensing and contributions from the backlog.

Despite these positive Q2 results, Arm’s guidance for Q3 revenue between $920 million and $970 million, while representing a 15% year-over-year increase, came in slightly below market expectations.

This prompted a pre-market dip in ARM stock, though shares quickly rebounded as investors focused on Arm’s ongoing strengths and broader market positioning.

Key growth drivers for ARM stock

Arm Holdings is strengthening its presence across multiple industries, particularly in AI and mobile processing.

A cornerstone of this strategy is the Armv9 architecture, which is increasingly adopted by major tech players like Apple Inc. (NASDAQ: AAPL).

This advanced architecture is crucial to ARM’s growth plan, as it powers popular products like MediaTek’s Dimensity 9400 processor and Apple’s iPhone 16, driving a surge in royalty revenues from smartphone application processors.

Another major growth driver is Arm’s Compute Subsystem (CSS), which has seen licensing activity double over the past year, making it a preferred choice for numerous partners’ chip designs.

CSS is now foundational in a range of innovative chip solutions, gaining traction in areas such as Advanced Driver Assistance Systems (ADAS) and In-Vehicle Infotainment (IVI) in the automotive sector.

Additionally, it is being integrated into Edge AI applications, where demand for AI solutions that utilize Arm’s v9 CPU architecture is on the rise.

Analyst projections and market sentiment

Wall Street analysts have largely maintained a positive outlook for ARM, seeing considerable growth potential as AI demand continues to expand.

JPMorgan raised its price target on ARM from $140 to $160 and maintains an Overweight rating on the shares.

Similarly, Susquehanna adjusted its price target from $115 to $118, noting a potential 5% downside risk to Q4 FY2025 consensus EPS but highlighting ARM’s resilience and sustained growth opportunities.

AI’s take on ARM’s year-end targets

To add depth to the analysis, Finbold consulted ChatGPT-4o, which projects ARM’s stock to reach between $145 and $160 by the end of 2024.

With ARM’s current price at $148, its growth potential is underpinned by robust Q2 earnings, a rise in royalty revenue, and high demand for its energy-efficient designs across AI and mobile sectors.

Despite a mixed market reaction to ARM’s Q3 guidance, strong Q2 results and ongoing demand for its Armv9 and CSS technologies showcase the company’s resilience.

ARM’s growth in AI and its expanding applications in consumer electronics, automotive, and edge computing support a solid foundation for long-term growth.

Featured image via Shutterstock