International Business Machines (NYSE: IBM) beat all Q2 2025 expectations in regard to profit, reporting $17 billion in revenue, a number far exceeding Wall Street’s forecast of $16.6 billion.

The numbers marked an 8% year-over-year increase, with adjusted earnings per share coming in at $2.80 versus the projected $2.65.

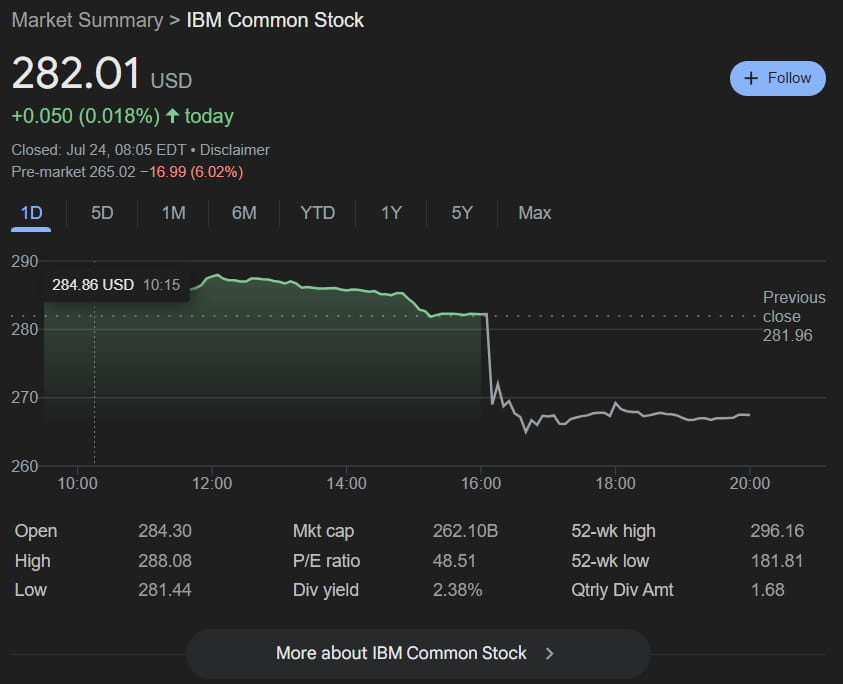

Despite the success, however, the IBM stock took a nosedive on Thursday, July 24, dropping 6.02% with a pre-market price of $265.02.

Why is IBM stock down?

IBM’s growing revenue was largely chalked up to its involvement with artificial intelligence (AI). However, investors were quick to note that the company’s software segment, which is also its largest business unit, only delivered $7.4 billion in revenue.

While this number marks an increase of 10% from a year ago, it still only met analyst expectations, leaving a portion of investors disappointed given that the stock had been gaining a lot of momentum leading up to the report.

Indeed, at Wednesday’s close, IBM shares were up 28% year-to-date, outpacing even Nvidia (NASDAQ: NVDA), whose stock was up 23.5%.

Wall Street IBN price projections

According to market analysis platform TipRanks, the average target price for IBN sits at $287.53 for the next 12 months, while the most optimistic analysts predict it could go as high as $350. The most bearish outlook, on the other hand, sees the stock sinking as low as $190.

IBM stock prediction. Source: TipRanks

Following the company’s second-quarter results, UBS raised the IBM stock price target from $195 to $200 on July 24, while reiterating a “Sell” rating.

Jefferies, on the other hand, reiterated its “Hold” rating on the same day, while maintaining the previous target price of $280.

As reported by TipRanks, UBS was concerned that the projected 5% growth in 2026 might be difficult to achieve with the software segment lagging behind.

Featured image via Shutterstock