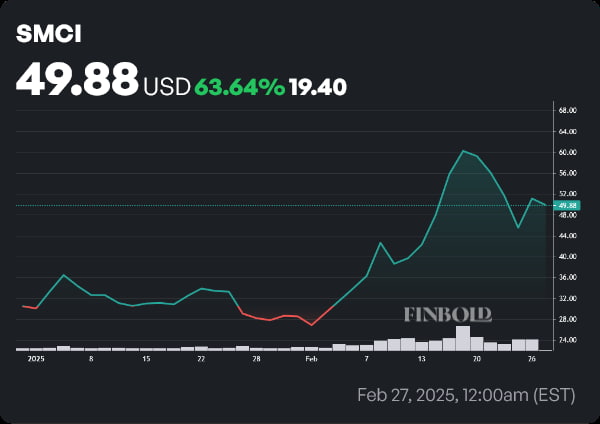

For most of 2024 and early 2025, Super Micro Computer was at risk of being delisted from the NASDAQ exchange. An August report from defunct short-selling group Hindenburg Research led SMCI stock (NASDAQ: SMCI) to drop to as low as $18 by mid-November.

However, in the aftermath of that low, one positive development after another occurred. Super Micro found a new auditor, and then held its Q2 2025 earnings call. Despite posting a double miss, the semiconductor company raised guidance for 2025 and 2026 quite significantly — and SMCI shares rallied to $50.93.

While it ended up being a net positive, the quarterly report did not see Super Micro regain compliance, although the business expressed confidence that it would be able to file the relevant documentation on time. That happened on February 25, and Super Micro shares surged to $56.22 — a 24.73% increase compared to the price of $45.54 per share seen a day prior.

By press time on February 27, SMCI stock was trading at a price of $49.88, bringing year-to-date (YTD) returns up to 63.64%.

As positive as these recent developments are, Super Micro will have to do a lot more to regain investor confidence. One Wall Street analyst, however, has already outlined his careful yet optimistic view of the company’s future prospects.

Barclays resumes SMCI stock coverage with cautiously bullish outlook

On February 27, Barclays analyst George Wan reinstated coverage on SMCI stock. Wan set an ‘Equal Weight’ rating on Super Micro Computer shares, as well as a $59 price target. The researcher’s price forecast implies an 18.28% upside from current prices.

In a note shared with investors, the Barclays analyst first noted Super Micro’s leading position in AI servers and direct cooling. He went on to note that he expects that the company will be among the first to ship B200 HGX servers in the March quarter.

Despite this optimistic beginning, the researcher’s note then turns more cautious. Wan believes that the business’s economic moat is shrinking. In addition, he highlighted that its “checkered past” could limit the price-to-earnings (P/E) multiples that investors are willing to pay for SMCI stock.

Finally, the analyst stated that Barclays “remains on the sidelines,” as it holds the opinion that Super Micro stock is still subject to future risks from financial controls, as well as the ongoing overhang of potential capital raises to fund the working capital needs for Blackwell purchases.

Wan utilized a 13x multiple based on a $4.52 earnings per share (EPS) estimate for CY 2026, in line with Barclays’ coverage on Dell, and ended the note by referring to the risk/reward of SMCI stock as balanced.

Featured image via Shutterstock