Palantir (NASDAQ: PLTR) saw its stock plummet 12% on February 19, following reports that CEO Alex Karp had adopted a new stock trading plan, allowing him to sell nearly 10 million shares over the next six months.

The decline was further compounded by reports that the Pentagon has been ordered to prepare for an 8% annual reduction in the U.S. defense budget for the next five years, posing a significant challenge for the company, which relies heavily on government contracts.

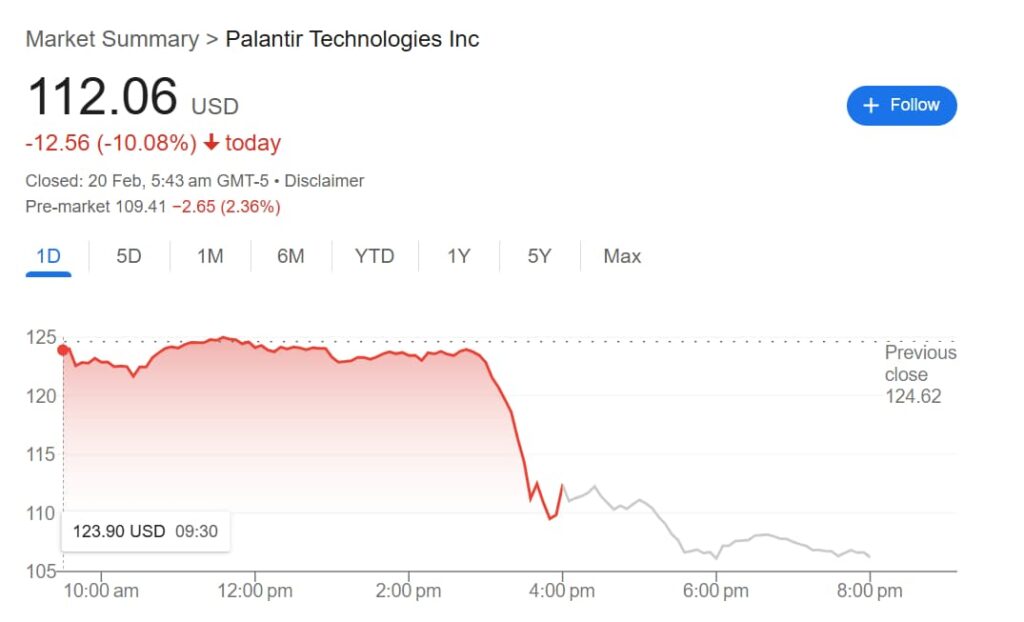

The sell-off erased a portion of the company’s impressive 2025 rally, which had seen shares climb nearly 50% year-to-date. Palantir, which had been one of the best-performing U.S. stocks over the past two years, closed February 19 at $112.06 per share, down 10% on the day.

Palantir’s slide didn’t stop there—the stock extended losses in premarket trading, dropping another 2.36% to trade at $109.41.

The decline comes not long after Palantir’s strong Q4 2024 results, which saw the company generate $828 million in revenue and report adjusted earnings of $0.14 per share.

Analyst sets Palantir stock price target

Although Palantir has enjoyed strong revenue growth and high-profile partnerships, its lofty valuation remains a persistent concern, with Wall Street analysts generally pricing in downside risk, setting an average price target well below current levels.

To put valuation concerns into perspective—even with the double-digit price pullback, Palantir still trades at 202 times this year’s expected earnings and 69 times this year’s expected sales, according to data retrieved from StockAnalysis.

However, not all analysts share the bearish outlook. Loop Capital has initiated coverage with a ‘Buy’ rating, with analyst Rob Sanderson setting a $141 price target, citing the company’s foothold in artificial intelligence (AI) and generative AI (GenAI) sectors, which represent massive market opportunities. Notably, Sanderson did not mention Karp’s stock sale or its impact on Palantir’s share price.

Loop Capital’s bullish stance is rooted in Palantir’s AI data platform, which integrates analytical tools, data infrastructure software, and AI solutions to enable government agencies and enterprises to identify complex patterns in large datasets.

Sanderson views Palantir’s go-to-market strategy as a key strength, allowing the company to rapidly expand its customer base. For instance, Palantir added 214 net new customers in 2024, up from 130 in 2023, while revenue from its top 20 customers grew to $64.6 million from $54.6 million.

Despite Palantir’s AI-driven growth, its valuation remains a concern. The stock is trading at nearly 44x EV/2027E revenue, a multiple that analysts recognize as steep.

Still, the firm sees parallels between Palantir’s potential and companies like Adobe (NASDAQ: ADBE) in digital marketing and Salesforce (NYSE: CRM) in cloud services, further strengthening its long-term appeal.

Loop Capital believes that Palantir’s dominance in AI-driven data analytics justifies its premium pricing, suggesting investors to ‘hold their nose on valuation’ and establish a position, with plans to add aggressively on pullbacks.

Featured image via Shutterstock