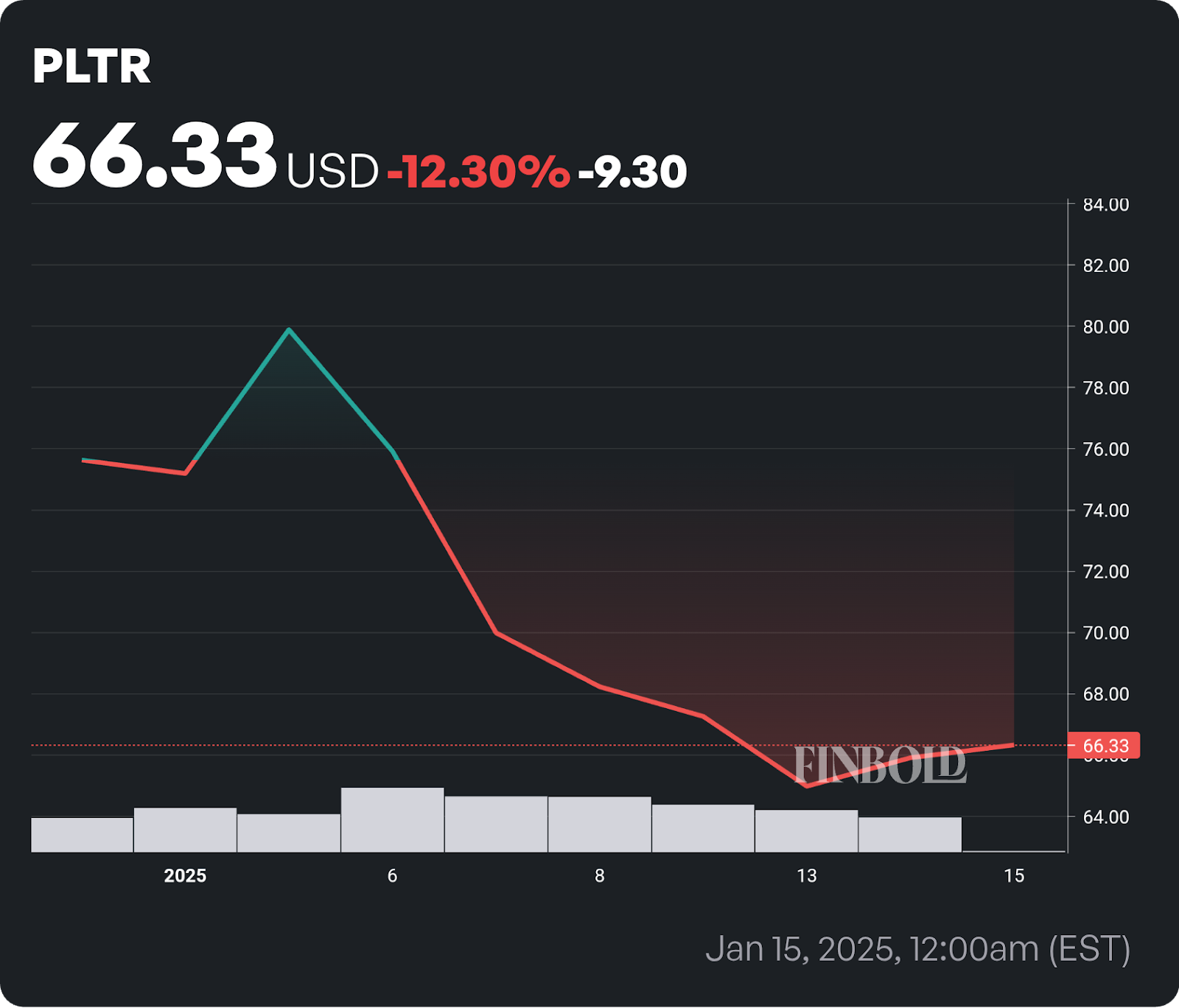

Raymond James analyst Brian Gesuale has reiterated a ‘Market Perform’ rating on Palantir (NASDAQ: PLTR) as the stock rebounded 1.4% during the latest trading session to $66.33, ending a multi-day losing streak.

Despite this, PLTR has had a rough start to 2025, dropping over 12% year-to-date, a period it has faced the threat of retesting lower support levels.

Gesuale updated his model to account for stock appreciation rights (SARs) vested when shares traded above $50 in Q4 2024.

In a January 15 investor note, he introduced an additional $120 million in stock compensation expense, reducing the firm’s GAAP EPS estimate for Q4 to $0.01 (from $0.06). However, adjusted EBITDA and adjusted EPS remain steady at $321.7 million and $0.11, respectively.

While highlighting potential headwinds in Palantir’s GAAP metrics, Gesuale emphasized that investors will likely focus on topline revenue, AEPS, and AEBITDA. However, he sees Palantir’s continued growth around its AI business.

“Looking further ahead, we remain enthusiastic about Palantir’s longer-term positioning in AI, though we are maintaining our Market Perform rating given our view that shares need to consolidate stellar gains over the last couple of years and grow into its rich valuation,” the expert said.

Palantir’s cautious outlook

The expert maintained a neutral stance, citing the need for shares to consolidate gains from recent years amid valuation concerns.

Other analysts share this cautious outlook. For example, Jefferies’ Brent Thill maintained an ‘Underperform’ rating with a $28 price target, citing valuation, volatility, insider selling, and competition in artificial intelligence (AI).

Similarly, Morgan Stanley downgraded Palantir to ‘Underweight’ with a $60 price target after a 340% surge in 2024, pointing to overvaluation despite strong performance in its government and commercial segments.

Palantir is trading at 36x forward sales and 258x forward earnings, fueling skepticism about its valuation.

Overall, speculation about Palantir’s future remains high, especially after Cathie Wood’s ARK Invest sold $15 million in PLTR shares across its ETFs.

This transaction has raised questions about whether the sale was a routine portfolio rebalance or a sign of potential challenges for the data analytics firm.

Palantir’s strong financials

Despite these concerns, Palantir continues to post strong financial results, which will likely determine the equity’s trajectory despite the valuation headwinds.

In Q3 2024, Palantir’s revenue grew 30% year-over-year to $726 million, driven by a 44% increase in U.S. business. U.S. commercial sales rose 54%, while government revenue climbed 40%, marking the strongest growth in 15 quarters.

Palantir closed 104 deals worth over $1 million, posted a 38% adjusted operating margin, and raised its 2024 revenue guidance to $2.807 billion.

Investors will closely monitor Palantir’s Q4 2024 earnings in February to gauge whether it can maintain its revenue momentum and how the stock might react.

Featured image via Shutterstock