Despite mounting an impressive rally in the closing months of 2024, Tesla (NASDAQ: TSLA) has been struggling in recent times. Tesla stock has experienced significant losses — meanwhile, no clear consensus has arisen. The company remains as controversial as its co-founder, Elon Musk.

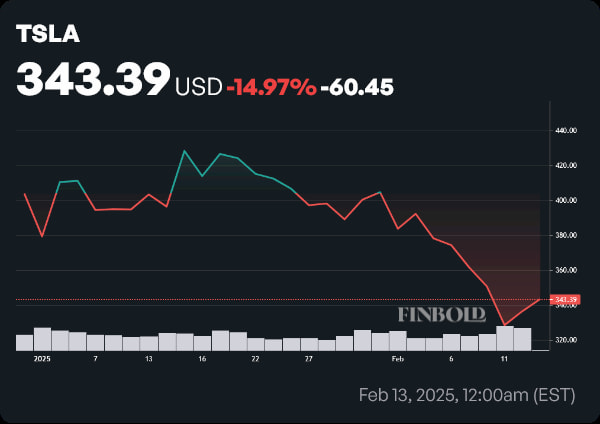

By press time on February 13, the price of Tesla shares had dropped to $343.39. That amounts to a 14.97% loss on the year-to-date (YTD) chart. The company’s losing streak has been going on since December 17 — in that time, the business has lost a staggering $500 billion in market capitalization.

Several factors have led to this steep correction. For one, the late 2024 rally was mostly based on hype — although the carmaker did have an unexpectedly strong earnings call, it was far and away from something that would justify the rally that ensued.

Picks for you

Hype tends to have a shelf-life — on top of that, Tesla’s next quarterly report was a dud — with both earnings and revenues coming in below consensus estimates, and vehicle deliveries marking their first year-over-year (YoY) decline.

Some have called into question chief executive officer (CEO) Elon Musk’s commitment to the company — bearing in mind his involvement with SpaceX, X, xAI, and the Department of Government Efficiency (DOGE). The CEO’s political affiliation has also reportedly polarized Tesla’s customer base.

As a disruptive business that has ignited a paradigm shift in an old, established industry, Tesla stock receives a lot of attention from analysts. However, one Wall Street firm has initiated coverage on Tesla in mid-February — and its outlook is quite bullish.

Benchmark confident Tesla stock will reach $475

On February 12, Benchmark analyst Michael Legg initiated coverage on Tesla stock. The researcher issued a ‘Buy’ rating with a $475 price target. If met, Legg’s forecast would imply a 38.32% upside from the current price of a TSLA share.

In a note shared with investors, the Benchmark equity researcher harkened to autonomous vehicles, robotics, and energy generation as potential growth drivers. In addition, he noted that further electric vehicle (EV) market penetration could also serve as a tailwind.

Further clarifying his decision, Legg highlighted several bullish developments. The analyst stated that the company has outlined a path for growth with a more affordable vehicle scheduled for the first half of 2025, unsupervised full self-driving (FSD) as a paid service in June, and Optimus robot production ramp through 2026 and beyond.

What’s quite interesting is that, unlike most analysts who cover the EV company and issue ratings for Tesla stock, the model Legg used to arrive at a $475 price target only incorporates vehicle growth. Per the analyst, if autonomous vehicles and Optimus, Tesla’s humanoid robot, achieve scale, there could be significant potential upside beyond what was set in the price target.

Featured image via Shutterstock