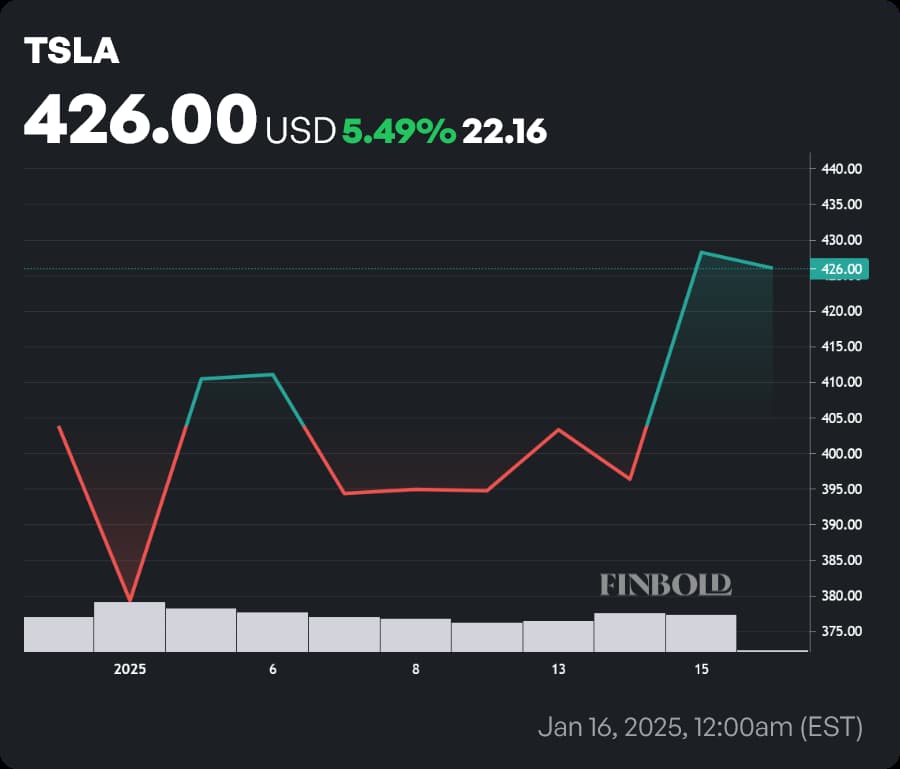

Since the start of 2025, the price of a Tesla (NASDAQ: TSLA) share has increased by 5.49% — at press time, TSLA stock was trading at $426.

The pioneering electric vehicle (EV) company isn’t without its fair share of detractors. The business, much like its co-founder, Elon Musk, is controversial — and its high valuation has been attracting criticism for years.

Opinions are quite split — some, like Gordon Johnson of GLJ Research, see disaster in the making — while others, like Morgan Stanley (NYSE: MS) analyst Adam Jonas, expect Tesla to outperform the wider market by a wide margin.

On the whole, however, Wall Street equity researchers are bearish. Tesla stock is a consensus ‘Hold’ based on 34 ratings — but the average price target of $293.76 equates to a pretty severe 31.22% downside.

In the midst of these strong opinions, investment banking giant Goldman Sachs (NYSE: GS) has updated its outlook on the EV company — providing a balanced, middle-of-the-road view of the carmaker’s future prospects.

Goldman deems Tesla an autonomous driving leader — but thinks the payoff is still far away

On December 11, Mark Delaney, an industrial tech and U.S. automotive equity analyst at Goldman Sachs, reiterated a prior ‘Neutral’ rating on Tesla stock, and maintained his $345 price target, which foresees a 19.01% downside. Delaney clarified his outlook in a note shared with investors.

The researcher cited third-party reviews, crowdsourced data, and Goldman Sachs’ own demo ride as causes for optimism when it comes to full self-driving (FSD), deeming the V13 update a meaningful improvement. While he deemed the company a leader in the space, the analyst cautioned that Tesla would have to make significant progress for it to become a situationally eyes-off product.

Goldman Sachs expects that the robotaxi business will begin commercial operations in the second half of 2026, and projects that it will contribute approximately $115 million to revenue in 2027. Interestingly enough, the investment bank believes scaling will move ahead slowly, and that the carmaker will opt to use geofencing and remote assistance to slowly improve technical performance.

Lastly, the analyst added that, while Tesla stock is trading at a full valuation, the long-term opportunities tied to FSD and robotics could cause it to remain trading at a higher multiple for an extended period. Delaney also noted that Tesla’s core automotive business is facing headwinds — but the company’s next earnings report, scheduled for January 29, should shed more light on that matter.

Featured image via Shutterstock