Advanced Micro Devices (NASDAQ: AMD) saw its stock fall over 10% on Wednesday, February 5, after missing Wall Street expectations for its key data center segment.

While the chipmaker exceeded revenue and earnings forecasts, its data center revenue came in at $3.86 billion—falling short of the $4.14 billion analysts had projected.

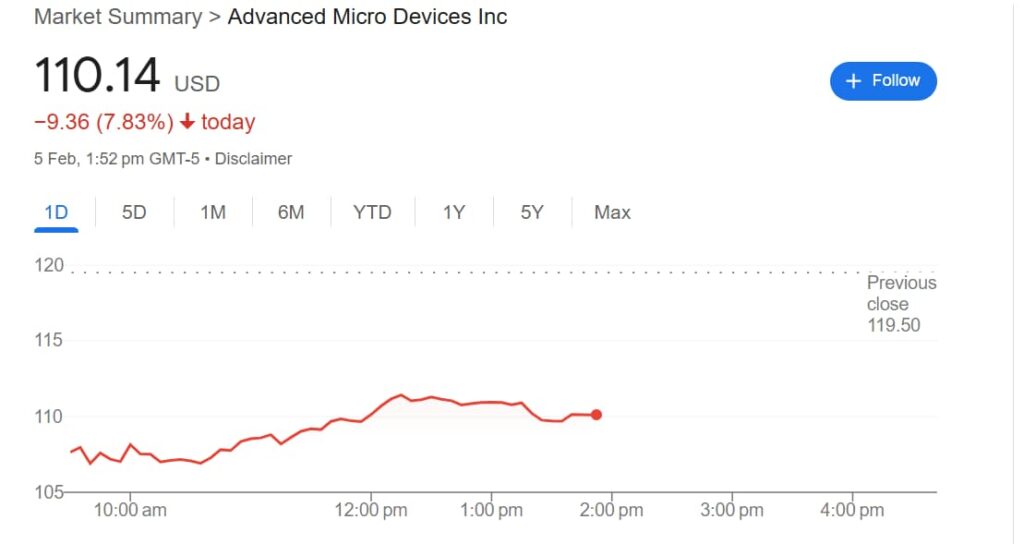

The disappointing figures sent AMD shares to a new 52-week low of $106.5 before rebounding. As of press time, the stock trades at $110, marking a 7% recovery on the day.

Picks for you

For the full year, AMD’s data center revenue surged 94% to $12.6 billion, with AI-focused Instinct GPUs contributing $5 billion. Yet, investors remain cautious as AMD struggles to gain meaningful ground against Nvidia (NASDAQ: NVDA).

Analyst reactions: A divided outlook

Following the earnings report, analysts have revised their price targets, with most firms cutting estimates but maintaining neutral to bullish stances on AMD’s long-term prospects.

Bearish projections

Citi lowered its price target from $175 to $110 and downgraded AMD to ‘Neutral’, citing the lack of AI revenue guidance and potential margin dilution. The firm expects AI revenue to remain flat or decline in the first half of 2025.

Goldman Sachs followed suit, lowering its price target from $129 to $125 while maintaining a ‘Neutral’ stance.

Analysts at the firm highlighted AMD’s underwhelming data center performance, noting that despite positive capital expenditure signals from hyperscalers like Microsoft (NASDAQ: MSFT) and Meta (NASDAQ: META) AI revenue visibility remains uncertain.

Meanwhile, BofA Securities pointed to AMD’s struggle to carve out a niche against Nvidia and lowered its price target to $135 due to weaker data center performance.

Neutral to bullish outlook

Despite near-term challenges, some analysts remain optimistic about AMD’s AI growth potential. Piper Sandler maintained an ‘Overweight’ rating with a $140 target, expecting AI growth to pick up in the second half of 2025 despite near-term setbacks.

KeyBanc also adjusted its outlook, trimming its price target to $140, but remained positive on AMD’s positioning in the AI market.

Meanwhile, on the more bullish end, Northland maintained its ‘Outperform’ rating with a $175 price target, projecting $9.2 billion in AI revenue for 2025, even as the first half remains flat.

UBS echoed this sentiment, lowering its target from $190 to $175 but retaining a ‘Buy’ rating, citing confidence in AMD’s AI roadmap.

The firm highlighted the early launch of the MI350 as a key factor in strengthening AMD’s competitive positioning against Nvidia’s B200.

Similarly, Barclays maintained an ‘Overweight’ rating with a $140 target, pointing to AMD’s rapid AI product transitions. With the MI350 set to launch mid-year and the MI400 following soon after, Barclays sees the recent stock weakness as a potential buying opportunity.

What comes next : Could AMD stock drop below $100?

With AI demand shaping the semiconductor landscape, AMD’s data center performance is now a major focal point for analysts and investors.

The earnings miss and overall market sentiment have sparked concerns that AMD stock could plunge below the $100 threshold. Analysts note that while AMD has made progress, uncertainties remain regarding its ability to capture a larger share of the AI chip market.

Adding to the pressure, the semiconductor industry faces potential headwinds from geopolitical factors, including the recent wave of U.S. tariffs on China, which could impact AMD and its competitors.

Additionally, the rise of AI models such as China’s DeepSeek has introduced new uncertainties as cost-efficient alternatives threaten the dominance of traditional Silicon Valley players.

While near-term uncertainty persists, analysts see AMD’s AI expansion as key to its future valuation, with a recovery expected in late 2025.

Featured image via Shutterstock