As financial markets await the anticipated Federal Reserve interest rate cut this week, Wall Street analysts have issued a mixed outlook for the benchmark S&P 500.

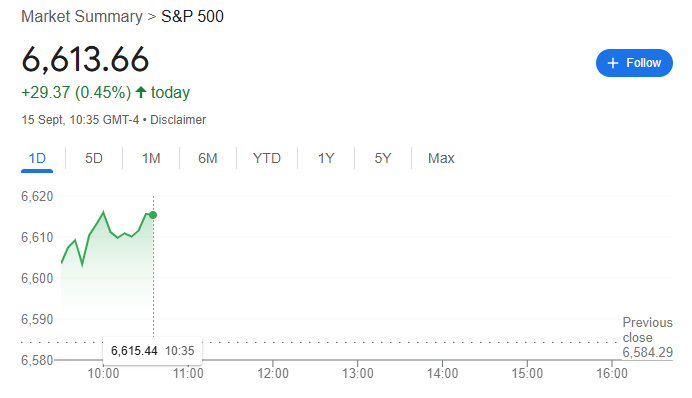

Expectations are building that the Fed may lower rates by 25 basis points. In the meantime, the S&P 500 has continued its record-setting rally since the early April dip, trading at 6,613 as of press time.

Among the analysts, Morgan Stanley’s Michael Wilson highlighted risks tied to weak labor data and slower Fed action but maintained a constructive long-term view. His bullish case projects the S&P 500 could climb as much as 9% to 7,200 points by mid-2026, encouraging investors to take advantage of short-term pullbacks.

“Near-term risk is centered on the tension between lagging, weak labor data and the Fed’s response that may not meet the markets’ need for speed,’” Wilson said.

Market resilience to be tested

On the other hand, JPMorgan, however, warned that the market’s resilience in the face of soft economic indicators may not last. The firm suggested that once the Fed resumes easing, equities could reassess current valuations and price in additional downside risks, tempering recent optimism.

“Once the easing resumes, equities could turn more cautious for a bit, and price in some more downside risk, in effect repricing the current, potentially complacent, stance,” the bank’s Mislav Matejka wrote.

Meanwhile, at Oppenheimer, John Stoltzfus acknowledged the likelihood of a near-term dip following the rate decision but expects any weakness to be temporary, supported by the broader strength of the U.S. economy.

Overall, strategists remain concerned that a modest cut may not fully address signs of economic slowdown, particularly in the labor market. With inflation still above the Fed’s 2% target and tariff pressures persisting, doubts remain about the effectiveness of the easing move.

Despite the warnings, the S&P 500 has stayed on a bullish trajectory, fueled largely by gains in technology stocks.

Featured image via Shutterstock