As China undergoes an economic crisis that has coincided with a difficult post-pandemic recovery period, many borrowers are defaulting on loans at unprecedented levels.

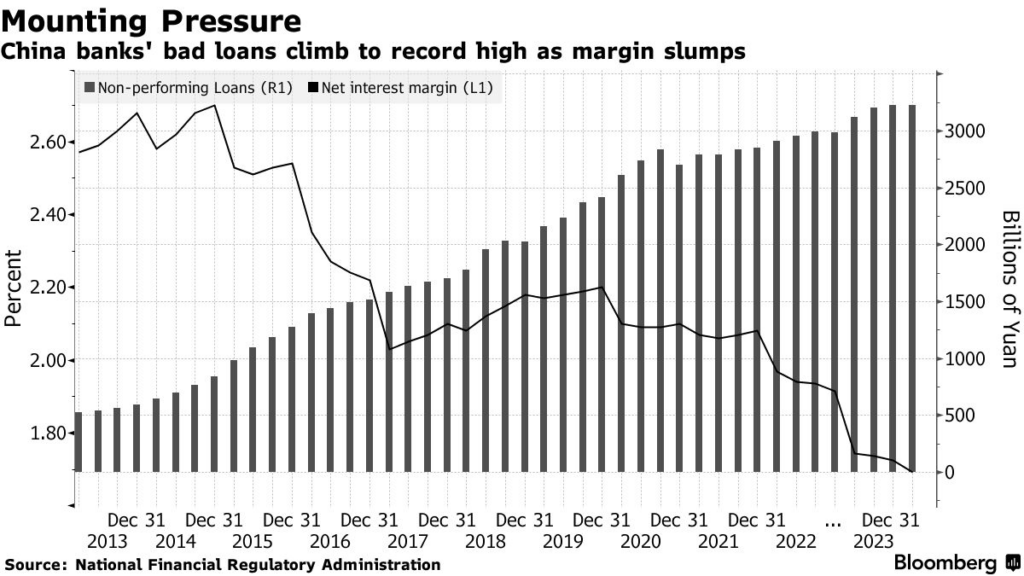

Particularly, as of March 28, the value of China’s banking bad loans had hit a record high of 3.28 trillion yuan ($0.45 trillion), Bloomberg data indicates.

The default figures have come in the wake of China’s prolonged property downturn with the bad loans significantly impacting some of the country’s largest lenders.

For instance, Bank of Communications recorded a surge in its property bad loan ratio from 2.8% to 4.99% by the end of last year, with special mention loans for the segment rising 23% to 9.88 billion yuan ($1.4 billion).

At the same time, Industrial & Commercial Bank of China Ltd. noted a 9.6% increase in bad loans from residential mortgages, reaching 27.8 billion yuan. Agricultural Bank of China saw a 4.7% uptick in soured residential mortgage loans, with the NPL ratio for the property sector surpassing other industries.

China’s property crisis

Indeed, the bad loan growth comes as the country’s property sector is in a transition from a state-dominated model to a more market-oriented approach.

Notably, the Chinese real estate market serves as a gauge of the country’s overall economic well-being. Given its intricate ties to diverse sectors such as construction and financial services, the sector’s vitality is indicative of the nation’s economic stability at large.

As previously reported by Reuters, Chinese banks accelerated the sale of bad loans at an unprecedented rate, driven by regulatory pressure to swiftly dispose of sour debts amidst a surge in consumer defaults.

In China, loans are typically classified as nonperforming if payments are overdue by more than 90 days.

Eroding confidence

In general, the increasing number of defaulters is contributing to a partial erosion of consumer confidence in China. This situation also highlights the absence of personal bankruptcy laws in the country, which could potentially mitigate the financial and social repercussions of escalating debt burdens.

At the same time, authorities are ramping up enforcement efforts, penalizing financial institutions for mishandling debts. The National Administration of Financial Regulation (NAFR), a newly established banking regulator, has issued several punishments in this regard.