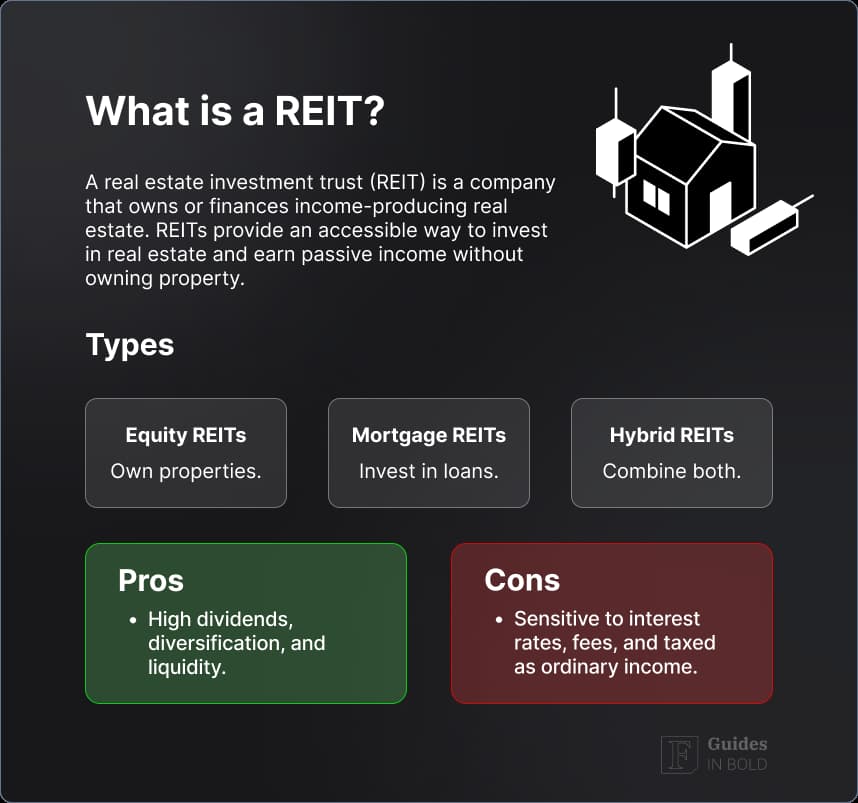

Real estate has long been considered a relatively safe and lucrative investment, but the hefty initial investment often makes it unattainable for most individuals. Fortunately, there’s a way to invest in real estate without the hassle of saving up for a down payment– real estate investment trusts.

This guide will examine real estate investment trusts (REITs) and how to start investing in them. Investors researching real estate opportunities may also benefit from this detailed PropStream Review, which covers property data analysis, lead generation, and market research tools used by many investors. We will investigate what REITs are, how they’re structured, the various types of REITs as well as the pros and cons of investing in them.

Highly Rated Stock Trading & Investing Platform

-

Invest in stocks, ETFs, options and crypto

-

Copy top-performing crypto-traders in real time, automatically.

-

0% commission on buying stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

eToro USA is registered with FINRA for securities trading.

Invest in REITs:

- Office REITs

- High Dividend REITs

- Data Center REITs

- Apartment REITs

- Self Storage REITs

- Farmland REITs

- Mortage REITs

- Cell Tower REITs

- Net Lease REITs

- Timber REITs

REIT definition

Equity REITs own and operate properties, generating revenue through collecting rental income and management fees. Additionally, they can be classified by the types of properties they own – residential, retail or office – and because the underlying property assets are so different, one category of REITs can have a different set of characteristics than the other.

Mortgage REITs, on the contrary, invest in real estate debt such as mortgages and mortgage-backed securities and generate revenue through interest income.

REITs can offer investors greater diversification, potentially bulkier total returns, and lower overall risk when constructing any equity or fixed-income portfolio. Using combined investments from a pool of investors is a way for you to invest in commercial real estate without actually purchasing and managing those properties yourself.

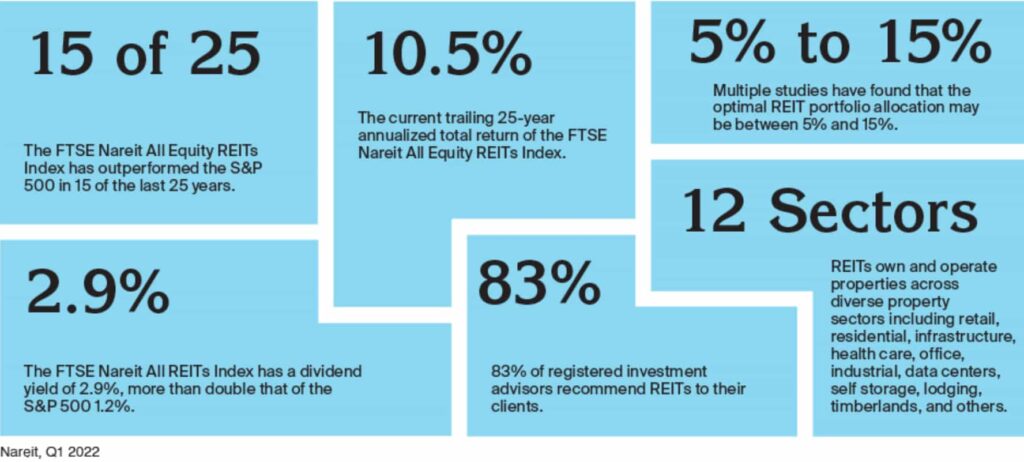

Moreover, one of the most significant benefits REITs offer is their high-yield dividends, as they are mandated to pay out 90% of taxable income to shareholders.

Investors can purchase shares in a REIT listed on major stock exchanges like any other public stock. In addition, investors may also buy shares in a REIT mutual fund or exchange-traded fund (ETF).

Beginners’ corner:

- What is Investing? Putting Money to Work

- 17 Common Investing Mistakes to Avoid

- 15 Top-Rated Investment Books of All Time

- How to Buy Stocks? Complete Beginner’s Guide

- 10 Best Stock Trading Books for Beginners

- 6 Basic Rules of Investing

- Dividend Investing for Beginners

- 5 Passive Income Investment Ideas

REITs historical returns

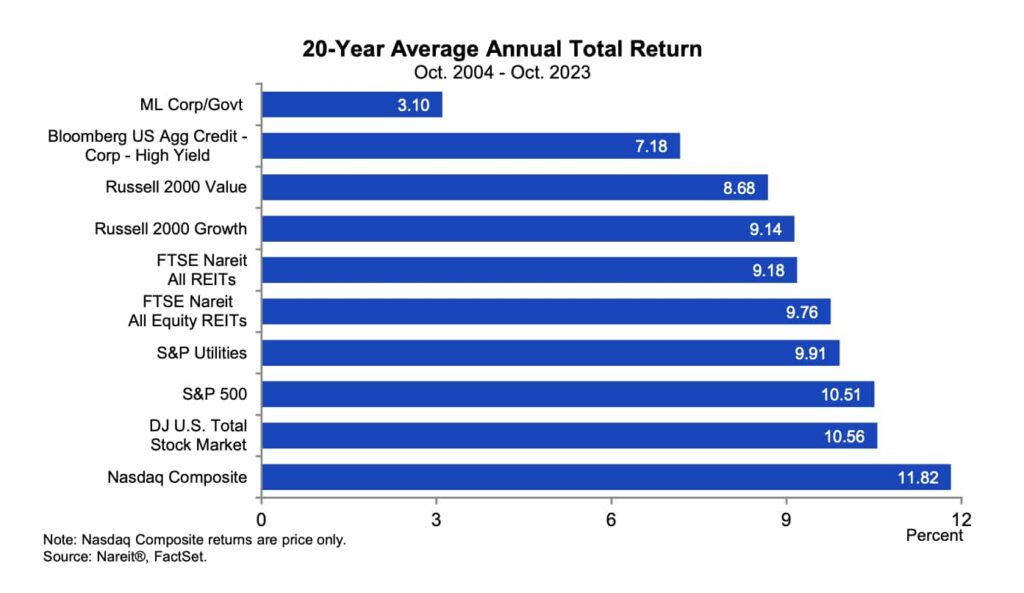

REITs have historically been one of the best-performing asset classes available. Most investors look at the FTSE NAREIT Equity REIT Index (a free-float adjusted, market capitalization-weighted index of U.S. equity REITs) to measure the performance of the U.S. real estate market.

For example, between 2004 and 2023, the index’s average annual return was approximately 12%, well above the S&P 500, clocking in at 9.34%. In fact, over that period, REITs were the best performing asset class in the U.S., more than doubling the rate of return delivered by bonds.

Indeed, investors looking for yield have done better investing in real estate than in fixed income (typically government and corporate bonds). However, a carefully constructed and diversified portfolio should consider both.

In short, the right way to think about REITs versus bonds is according to your total asset allocation. REITs can account for a certain amount of the equity portion in your portfolio. Still, at the same time, bonds should be owned separately since they serve as capital preservation during a recession and in a bear market.

Understanding REIT structure

The government mandates REITs to abide by specific regulations, including that they:

- Distribute a minimum of 90% of taxable income to shareholders through dividends each year;

- Have at least 100 shareholders after their first year in business;

- Invest a minimum of 75% of its assets in real estate and cash:

- Receive a minimum of 75% of gross income from rent and mortgage interest sources;

- Have not more than 50% of shares held by five or fewer individuals during the last half of the taxable year.

Since REITs must distribute 90% of their earnings as dividends, they’re exempt from paying income taxes on the profits paid to shareholders, allowing them to finance real estate more cheaply than non-REIT companies. As a result, REITs generally have very high yields and payout ratios since they must disburse a significant chunk of their earnings. But, notably, the payout ratio is not a useful measure for investors evaluating REITs.

How to evaluate any REIT?

Key things to look out for when assessing a REIT:

- High dividend yields and long-term capital appreciation: Choose companies that have historically done a decent job at delivering both;

- Liquidity: Unlike traditional real estate, many REITs are traded on stock exchanges, meaning investors can get the diversification real estate delivers without being locked in long-term;

- Diversification: Consider buying a mutual fund or ETF that invests in REITs.

- Measure operating performance: Depreciation exaggerates an investment’s decline in property value. Therefore, rather than utilizing the payout ratio (what dividend investors use) to assess a REIT, look at its funds from operations (FFOs), calculated by taking the dividend per share and dividing it by the FFO per share. (the higher the yield, the better);

- Strong management: Look for companies that have been in business for a while or possess a management team with plenty of experience;

- Quality: Only invest in REITs with sound properties and tenants.

Types of REITs

REITs can be divided into three broad categories by their investment holdings: equity, mortgage, and hybrid REITs.

Each class further falls into three types by how the investment can be acquired:

- Publicly-traded REITs: registered with the U.S. Securities and Exchange Comission (SEC) and are publically traded;

- Non-traded REITs/non-exchange traded REITs: registered with the SEC but are not publicly traded;

- Private REITs.

Equity REITs

Equity REITs are the most prevalent type of REIT. They own the underlying real estate and take care of all the tasks typically associated with a landlord, like building, renovating, and managing the property. Their revenues are primarily generated through rental incomes on their real estate holdings. An equity REIT may invest broadly or focus on a particular segment.

All in all, equity REITs deliver stable income, and since they generate income by collecting rents, their revenue is relatively easy to forecast and tends to increase over time.

Retail REITs

With roughly a quarter of REIT investments concentrated in shopping malls and freestanding retail, these REITs are pivotal in the real estate sector. They focus on owning and managing retail properties.

However, there are longer-term concerns for the retail REIT space in that shopping is increasingly redirecting online. Moreover, although owners have continued to innovate to fill their space with offices and other non-retail-oriented tenants, the subsector is undoubtedly under pressure.

Before investing, investors should:

- Examine the retail industry itself. While it might be financially sound at the moment, it is crucial to evaluate its prospects. Because retail REITs earn money through the rent they charge tenants, any money issues due to poor sales might end in monthly payments going unpaid, eventually forcing them into bankruptcy;

- Look for strong anchor tenants like grocery and home improvement stores;

- Make an industry assessment, i.e., look for REITs with good profits, strong balance sheets, and as little debt as possible, especially short-term.

Residential REITs

These REITs own and operate multi-family rental apartment buildings and manufactured housing.

Before investing, investors should consider factors like:

- Low home affordability: the best apartment markets tend to be where home affordability is low relative to the rest of the country. The best residential rates are usually in large urban areas where apartment supply is low, and demand is rising, driving up the price landlords can charge each month;

- Population and job growth: a net inflow of people to a city generally indicates that jobs are readily available and that the economy is booming. Similarly, a falling vacancy rate coupled with rising rents suggests that demand is improving;

- Low apartment supply: as long as the supply of housing remains low and demand rises, residential REITs should do well;

- Solid balance sheets and available capital.

Healthcare REITs

Healthcare REITs invest in medical centers, hospitals, retirement homes, and nursing facilities. Their success is directly tied to the healthcare system since the bulk of the operators of these establishments depend on occupancy fees, Medicare and Medicaid reimbursements, and private pay.

As Americans age and healthcare costs rise, healthcare REITs will continue to become a compelling subsector. However, as long as healthcare funding remains up for dispute, so are healthcare REITs.

Things to look for in a healthcare REIT include:

- A diversified group of customers and investments in several different property sectors to manage risk;

- Growing demand for healthcare services, which should ensue with an aging population;

- Customer and property-type diversification;

- Companies with significant healthcare experience, solid balance sheets, and high access to low-cost capital.

Office REITs

Office REITs invest in office facilities and receive rental income from tenants who have typically signed long-term leases.

Investors interested in investing in an office REIT should consider the following factors:

- The state of the economy and the unemployment rate. Investors should favor REITs that invest in economic strongholds, e.g., it is more profitable to own several average buildings in Washington, D.C., rather than prime office space in Detroit;

- Vacancy rates;

- The economic viability of the area in which the REIT invests;

- Amount of capital for acquisitions.

Mortgage REITs

Unlike equity REITs, mortgage REITs (mREITs) do not own the underlying property; instead, they own debt securities backed by the property. While equity REITs typically generate revenue through rents, mortgage REITs earn income from the interest on their investments (mortgages, mortgage-backed securities (MBS)).

Approximately 10% of REIT investments are in mortgages instead of real estate. The best-known investments are Fannie Mae and Freddie Mac, government-sponsored enterprises that purchase mortgages on the secondary market.

Things to keep in mind about mortgage REITs:

- Rising interest rates would translate into a decrease in mortgage REIT book values, driving stock prices lower;

- Mortgage REITs get a notable amount of their capital through secured and unsecured debt offerings. An increase in interest rates will make future financing more expensive, reducing the value of a portfolio of loans;

- In a low-interest-rate environment with the prospect of rising rates, most mortgage REITs trade at a discount to net asset value per share;

- Mortgage REITs are typically riskier than equity REITs and tend to pay out higher dividends;

- However, mortgage REITs tend to do better than equity REITs when interest rates rise.

Mortage vs. equity REIT example

Let’s imagine a REIT company X purchases an office building with the funds generated from investors and rents out office space. They own and operate this real estate property and collect monthly rent payments from its tenants. Company X is thus considered an equity REIT.

Conversely, imagine another REIT qualified company called Y that lends money to a real estate developer. However, unlike company X, company Y generates income from the interest earned on the loans. Company Y is thus a mortgage REIT.

Hybrid REITs

Hybrid REITs are a combination of equity and mortgage REITs. They own and manage real estate properties as well as own commercial property mortgages in their portfolio.

REIT types by trading status and where to buy them

REITs can further be classified by how the investment is acquired:

Publicly traded REITs

Like stocks and ETFs, publicly-traded REITs are traded on exchanges and are available for purchase using an ordinary brokerage account (eToro, Interactive Brokers) or simply via a challenger bank app such as Revolut. According to the National Association of Real Estate Investment Trusts (Nareit), more than 200 publicly-traded REITs are on the market.

Publicly traded REITs tend to be more transparent and have better governance standards. Moreover, they offer the most liquid stock, meaning investors can buy and sell the REIT’s stock much faster than purchasing and selling a property yourself. For these reasons, they are favored among REIT investors.

Highly Rated Stock Trading & Investing Platform

-

Invest in stocks, ETFs, options and crypto

-

Copy top-performing crypto-traders in real time, automatically.

-

0% commission on buying stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

eToro USA is registered with FINRA for securities trading.

Non-traded REITs

Non-traded REITs are registered with the SEC but not available on an exchange. Instead, investors can acquire them from a broker that participates in non-traded offerings, like the online real estate broker Fundrise.

However, according to the Financial Industry Regulatory Authority, these REITs are highly illiquid, often for eight years or more, because they aren’t publicly traded.

Non-listed REITs also can be hard to evaluate. The SEC warns that these REITs frequently don’t assess their value for investors until 18 months after their offering ends, often years after your investment.

Finally, several online trading platforms authorize investors to purchase shares in non-traded REITs, including Modiv, the DiversyFund, and Realty Mogul.

Private REITs

Private REITs are unlisted, making them more challenging to evaluate and trade. In addition, they are generally exempt from SEC registration. And as a result, they have fewer disclosure requirements, and they might carry additional risks, thus making them less attractive to investors.

To begin trading, public non-traded REITs and private REITs can also have much higher account minimums, i.e., $25,000 or more, and heftier fees than publicly-traded REITs. Therefore, private REITs and many non-traded REITs are open only to ratified investors with a net worth of at least $1 million.

Fees and taxes associated with REITs

Consider the following costs when investing in REITs:

Trading fees

Publicly traded REITs can be purchased through an ordinary broker, where typical brokerage fees apply.

On the other hand, non-traded REITs are sold by a specific broker or financial adviser and thus have high up-front costs. Commissions and upfront offering fees can total roughly 9 to 10 percent of the investment, lowering the investment value significantly.

Tax considerations

Most REITS pay out at least 90 percent of their taxable income to their shareholders, making the shareholders responsible for paying taxes on the dividends and any capital gains they receive. Dividends paid by REITs are generally treated as ordinary income and are not entitled to the reduced tax rates on other corporate dividends.

How to avoid fraud?

Beware of anyone trying to sell REITs that are not registered with the SEC. You can confirm the registration of both publicly traded and non-traded REITs through the SEC’s EDGAR system. This database provides free public access to corporate information, allowing you to research a public company’s financial information and operations by reviewing the company’s filings with the SEC.

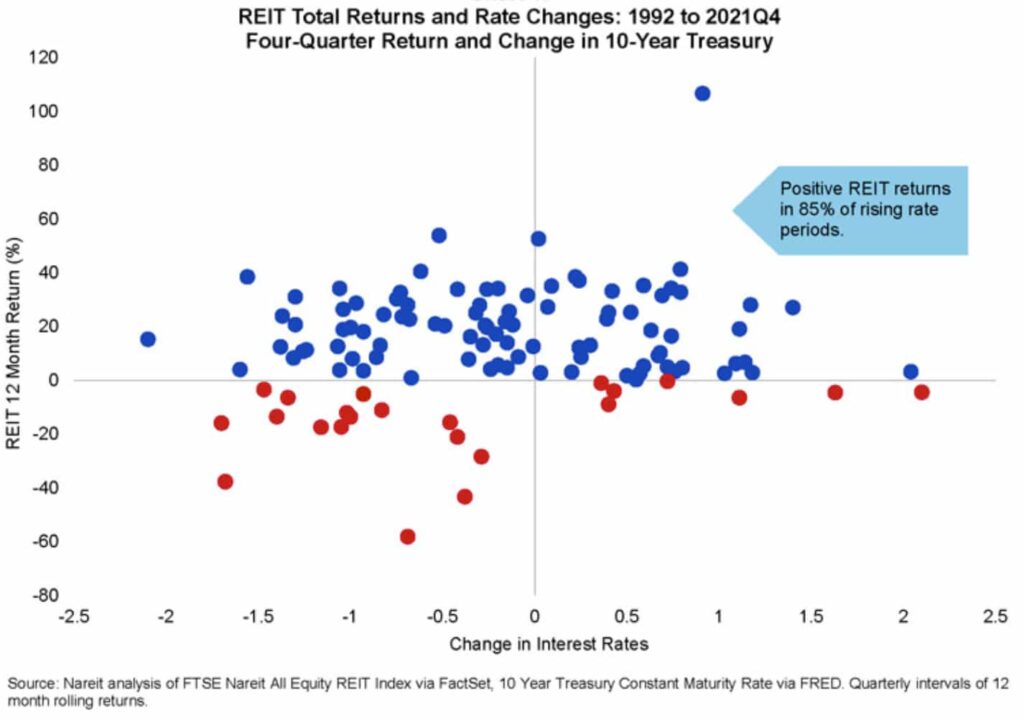

Rising interest rates and REIT performance

Like the broader stock market, REIT share prices have been sensitive to changes in interest rates, both long-term rates influenced by market forces and the short-term rates set by the Federal Reserve. Because of the current inflationary environment, the Federal Reserve has raised its benchmark interest rate by half a percentage point to address concerns about inflation.

Historically, REITs have performed well during rising long-term interest rates, with an average four-quarter return of 16.55% compared to 10.68% in non-rising rate periods from the first quarter of 1992 to the fourth quarter of 2021.

Moreover, REITs outperformed the S&P 500 in half of the periods when Treasury yields increased. Notably, the positive association between rising rates and REIT returns is consistent with the progress in the underlying fundamentals.

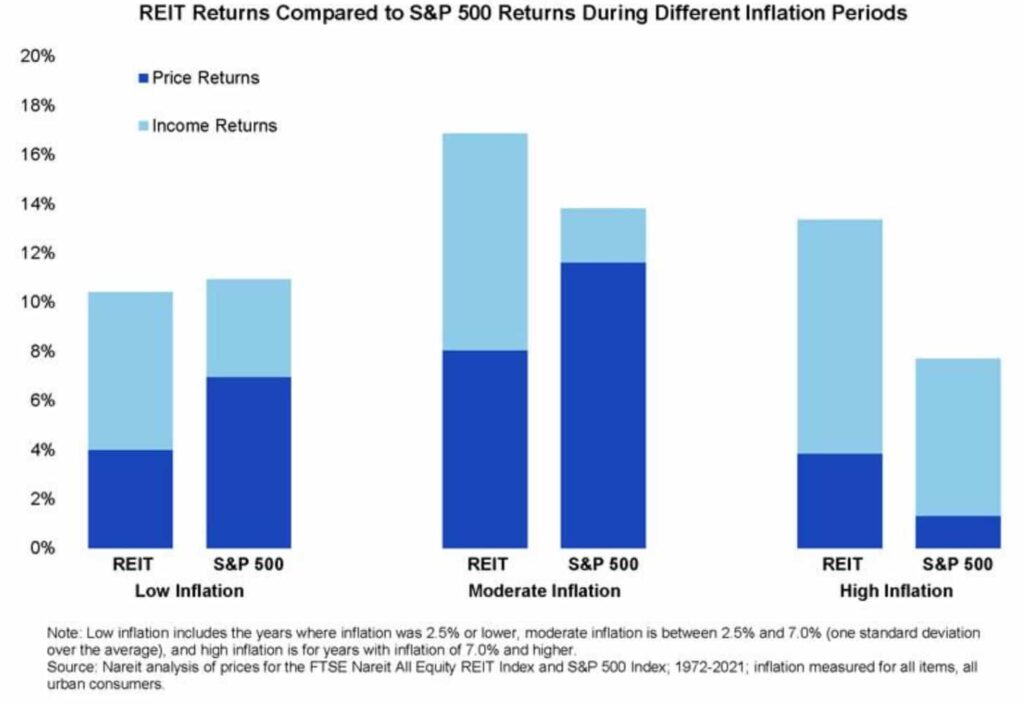

Impact of inflation on REITs

Consumer prices have risen dramatically as the economy had to work through supply chain issues during the ongoing recovery from COVID-19 induced shut-downs. As a result, annual inflation measured by the Consumer Price Index reached 8.5% in March 2022, the highest yearly rate in 40 years.

REITs have historically protected against inflation and outperformed the broader stock market during moderate and high inflation periods. For example, in 2021, with inflation running well above recent trends, REITs outperformed the S&P 500 by 12.6 percentage points.

Their success is due to long-term leases typically having built-in inflation protection and because shorter-term leases are based on current price levels. Additionally, REITs keep a portfolio of leases, a portion of which is negotiated every year, so even REITs with longer-term leases have opportunities to reprice.

Finally, as owners of tangible assets, REITs generally enjoy an appreciation in portfolio value and the price level. With rents and values tending to increase with prices, REIT dividends help provide a reliable stream of income even during inflationary periods.

Pros and cons of REITs

REITs are popular instruments for investors due to their high yields and relatively steady cash flow. However, as with any investment, they still include a certain degree of risk, and careful research is needed to separate high-quality players from those in decline. There are advantages to investing in REITs, particularly those that are publicly traded:

Pros

- Steady dividends with high yields: Because REITs must distribute 90% of their annual taxable income as shareholder dividends, they consistently deliver some of the heftiest dividend yields in the stock market. Therefore, REIT dividends are often much higher than the average stock on the S&P 500;

- Portfolio diversification: Not too many people are capable of purchasing a piece of commercial real estate to generate passive income. Yet, REITs offer the general public the ability to invest in a commercial income portfolio;

- Longer cycle: REITs can offer diversification benefits since they tend to follow the real estate cycle, which generally lasts a decade or even longer, whereas bond- and stock-market cycles typically last an average of approximately 5.75 years;

- Sound returns: Returns from REITs often beat equity indexes, which is another reason they are an attractive option for portfolio diversification;

- Liquidity: Publicly traded REITs can be bought and sold with a click of a button, making them far more accessible than actually buying, operating, and selling commercial properties;

- Inflation hedge: REITs can effectively hedge against rising inflation rates. In particular, REITs with commercial holdings frequently have agreements that allow them to raise rents in tandem with inflation;

- Lower volatility: REITs tend to be less volatile than traditional stocks because of their higher dividend payouts. Furthermore, REITs can act as a hedge against the anxiety-ridden fluctuations of other asset classes, but no investment is immune to volatility.

Cons

- Severe debt: REITs are usually among the most indebted companies. However, REITs typically have long-term contracts that generate regular cash flow, such as leases, to support their debt payments and ensure shareholder dividends;

- Tax burden: While REITs pay no taxes, shareholders must pay taxes on dividends and any capital gains received unless they are collected in a tax-advantaged account. Notably, most REIT dividends don’t meet the IRS definition of “qualified dividends,” meaning they are taxed higher than other dividends. They do qualify for the 20% pass-through deduction, though. However, most investors will need to pay substantial taxes on REIT dividends if they hold REITs in a standard brokerage account. That’s one reason REITs can be an excellent fit for IRAs (Individual retirement accounts);

- Sensitivity to interest rates: Real estate is typically susceptible to changes in interest rates, which can affect property values and occupancy demand. Usually, when the Federal Reserve raises interest rates to tighten up spending, REIT prices fall;

- Property specific risks: Hotel REITs, for example, often do extremely poorly during times of economic downfall. Beware, too, of retail REITs since the bulk of business is moving online;

- Occupancy risk: REITs must hold certain occupancy levels to maintain dividend payouts, which closely correlate with the rent these properties can request. Therefore, lower rents and occupancy rates can negatively impact REITs;

- Geographic risk: REITs may have a narrow geographic focus, in which most of the property is located in urban centers;

- Natural disasters: Damage from hurricanes, floods, tornados etc. can affect property values and income;

- Market risk: REITs closely follow the real estate market and are subject to similar dangers, including fluctuations in property value, leasing occupancy, and geographic demand.

Notable drawbacks for non-traded REITs:

- Costly: An initial investment in a non-traded REIT can be expensive, sometimes $25,000 or more, and may be limited to accredited investors. Non-traded REITs also may have higher trading fees than publicly-traded REITs;

- Low liquidity: Non-listed REITs are illiquid investments, as they typically cannot be sold readily on the open market and must be held for years to realize potential gains;

- Share value: It can be challenging to determine the value of a share of a non-traded REIT compared to a publicly-traded REIT. Non-traded REITs typically do not estimate their value per share until 18 months after their offering closes, often years after making your investment. As a result, you may be unable to assess the value of your non-traded REIT investment and its volatility for a significant period;

- Deceptive distributions: Compared to publicly-traded REITs, investors may be attracted to non-traded REITs by their relatively high dividend yields. However, unlike publicly-traded REITs, non-traded REITs frequently distribute more than their operations funds by offering proceeds and borrowings. This practice, typically not used by publicly-traded REITs, diminishes the value of the shares and the cash available to the business to acquire additional assets;

- Conflicts of interest: Non-traded REITs generally have an external manager instead of their own employees, leading to possible conflicts of interest with shareholders. For instance, the REIT may pay the external manager considerable fees based on the number of property acquisitions and assets under management, even though these fee incentives may not necessarily align with the interests of shareholders.

Read also: Top 6 Real Estate Investing Books for Beginners

In conclusion

Suppose you’re interested in real estate’s income and growth potential. In that case, REITs can provide a way to add that exposure to your portfolio without dealing with the nuisances involved in buying, operating, and owning individual pieces of property.

Additionally, REITs offer high dividend yields, and their legal setup demands that they distribute 90% of their income to shareholders, making them attractive dividend options for a diversified income portfolio.

All in all, much like with any financial decision you choose to take, you should continually evaluate your financial goals and determine how your next move will help you get closer to that goal.

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.

FAQs about REITs

What are REITs?

REITs are companies that own, operate, or finance income-producing real estate across various property sectors. Investors can purchase two primary types of REITs: equity REITs and mortgage REITs. Each class further falls into three types by how the investment can be acquired: publicly-traded REITs, non-traded REITs, and private REITs.

How are REITs structured?

To qualify as a REIT, a company must have 75% of its assets in real estate or cash, and 75% of total income must come from real estate sources such as rent or mortgage interest. Moreover, REITs must pay out 90% of taxable income in shareholder dividends as well as have a minimum of 100 shareholders after their first year in business.

What are the benefits of investing in REITs?

REITs can offer investors greater diversification, potentially more significant total returns, steady high-yield dividends, and lower overall risk when constructing any equity or fixed-income portfolio. They are, essentially, a way for individuals to invest in commercial real estate without actually purchasing and managing those properties themselves.

Are REITs risky?

In general, REITs are not considered particularly risky, especially when they have diversified holdings, solid management, quality properties based on contemporary trends, and are publicly traded. However, REITs can be sensitive to interest rates and may not be as tax-friendly as other investments. In addition, if a REIT is too concentrated in a particular sector and that sector is negatively impacted (e.g., pandemic, natural disaster), you can see amplified losses.

What are the best REITs to invest in?

The best REITs to invest in generally include those with strong portfolios in high-demand sectors, stable income streams, and solid growth prospects. Popular categories include residential, commercial, healthcare, and industrial REITs. Investors often look for REITs with a consistent track record of dividend payments and potential for capital appreciation. The specific choice of REITs can vary based on individual investment goals, risk tolerance, and market conditions. It’s crucial to conduct thorough research or consult with a financial advisor before investing.

Why not to invest in REITs?

Investing in REITs may not be ideal for some due to market volatility, sensitivity to interest rate changes, potential liquidity issues, and the taxation of dividends at higher income rates. Additionally, overconcentration in REITs can lead to a lack of diversification, exposing investors to sector-specific risks inherent in real estate markets.

What is the difference between investing in REITs vs rental property?

Investing in REITs provides exposure to real estate through a diversified portfolio of properties or real estate loans. It offers liquidity, as REITs are typically traded on major stock exchanges, but investors don’t have direct control over the properties. In contrast, investing in rental properties involves direct ownership, offering more control and potential for higher personal involvement in property management. However, it requires more capital upfront and can be less liquid compared to REITs.

Highly Rated Stock Trading & Investing Platform

-

Invest in stocks, ETFs, options and crypto

-

Copy top-performing crypto-traders in real time, automatically.

-

0% commission on buying stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

eToro USA is registered with FINRA for securities trading.