Summary

⚈ AMD’s Q1 2025 earnings beat expectations, but export controls impact revenue projections.

⚈ Evercore ISI maintains a $126 target, citing growth in AMD’s data center GPU segment.

Banking giant Jefferies revised its AMD stock price target following the semiconductor company’s Q1 2025 earnings report on May 6.

The chipmaker’s earnings per share (EPS) came in at $0.96, outpacing estimates of $0.94. Revenues of $7.44 billion likewise outperformed consensus expectations of $7.13 billion.

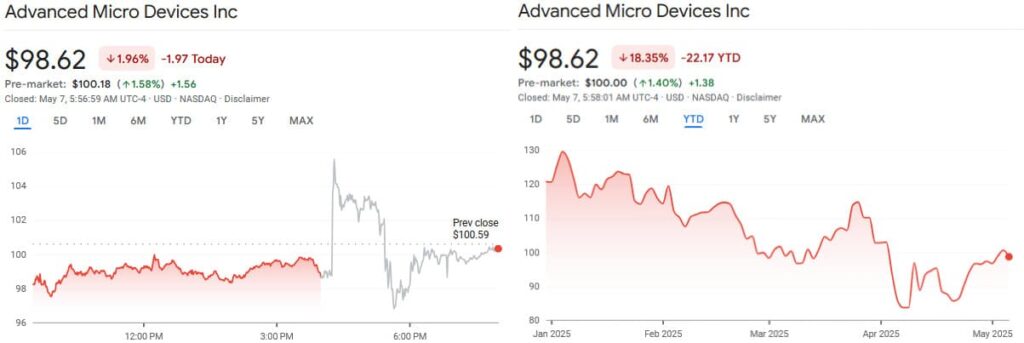

In the aftermath of the earnings call, Advanced Micro Devices’ stock prices decreased by 1.96%, although they had rebounded to $100.18 as of press time in the pre-market trading session on May 7. AMD shares are down 18.35% on a year-to-date (YTD) basis at the time of writing.

Despite better-than-anticipated results, several headwinds are also at play. The company has already incurred $700 million in lost revenue owing to export controls — and expects that the final tally will reach $1.5 billion by the end of the fiscal year.

Jefferies cuts AMD stock price target to $100

On May 7, Jefferies equity researcher Blayne Curtis maintained a ‘Hold’ rating on AMD stock, but cut his 12-month price forecast from $120 to $100.

While he did note strength in the server and client segments, Curtis maintains that artificial intelligence (AI) growth remains the key metric for AMD — and that there has been little progress on that front. According to the analyst, growth in that sector will depend chiefly on the 2H25 ramp driven by the MI350 launch — and Jefferies has not seen any meaningful traction thus far.

Curtis’ price target implies a 1.39% upside compared to current prices. Once all was said and done, the analyst summarized the investment bank’s revised outlook thusly: “We remain on the sidelines as there is really no upside without an AI story.”

Evercore ISI doubles down on bullish AMD stock price forecast

Conversely, Evercore ISI equity analyst Mark Lipacis, the head of the investment bank’s semiconductor research, reiterated an ‘Outperform’ rating on AMD stock, and kept a $126 price target, which implies a 27.76% upside compared to current prices.

The chipmaker expects to see a growth of 60% on a sequential basis in its data center GPU segment — which aligns with Evercore’s AI channel checks. In addition, Lipacis expects that hyperscalers will make AMD a larger part of their internal workloads going forward.

Featured image from Shutterstock