Nvidia (NASDAQ: NVDA) may be flashing the ‘biggest green flag’ in stock investing, potentially positioning the technology giant to target new highs, possibly even the $200 level.

Specifically, this bullish signal lies in the fact that as the company’s shares rise, its valuation multiple continues to shrink.

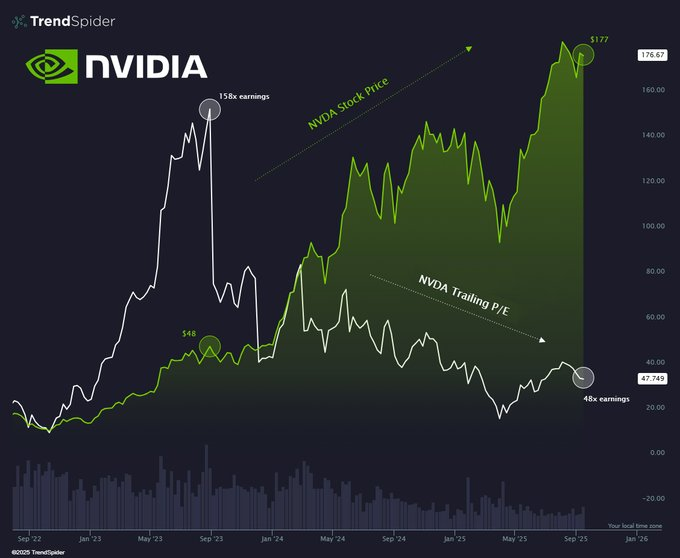

Data from charting platform TrendSpider shows that Nvidia’s stock has surged from around $48 in late 2022 to nearly $177 in September 2025, marking an explosive run.

Over the same period, the company’s trailing price-to-earnings (P/E) ratio has fallen sharply, dropping from a peak of 158x earnings in 2023 to about 48x today.

This divergence suggests that Nvidia’s earnings growth is outpacing market expectations, fueling optimism for further upside.

Notably, analysts often view this scenario as a bullish setup, indicating that strong fundamentals, rather than overvaluation, are driving the rally.

NVDA stock fundamentals

At the same time, the stock’s fundamentals support this view. For instance, Nvidia has posted extraordinary revenue growth, with fiscal 2025 sales reaching about $130.5 billion, more than double the prior year.

In the most recent quarter, revenue climbed to $46.7 billion, representing 56% year-on-year growth.

However, the American semiconductor giant is not without risks. For instance, ongoing U.S. restrictions on chip exports to China have already led to inventory write-downs and threaten to weigh on future revenue.

At the same time, Nvidia has been caught in the escalating technology rift between the United States and China. Markets recently reacted to reports that China’s internet regulator ordered its biggest tech firms to stop buying Nvidia’s artificial intelligence chips.

Overall, with evidence showing that price gains are underpinned by real earnings growth, Nvidia’s rally appears more sustainable than one driven solely by multiple expansion.

Featured image via Shutterstock