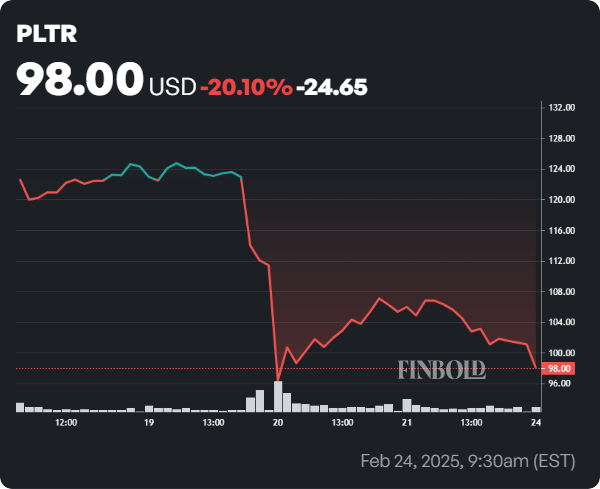

Palantir’s (NASDAQ: PLTR) stock losses are accelerating, with the equity sliding below the critical $100 support level, a key anchor to its record high of nearly $125.

The sustained downturn reflects investor reaction to a series of pessimistic developments surrounding the company, particularly concerning its government contracts and insider trading activity.

As of press time, PLTR stock has extended its losing streak from the past week, trading at $98.42, down over 4%. On the weekly chart, the stock has plunged by a staggering 20%.

Picks for you

Why PLTR stock is plunging

While broader stock market volatility has played a role, several catalysts are contributing to PLTR’s decline as investors become increasingly cautious about its future trajectory.

A key factor behind the sell-off is a report indicating that the Donald Trump administration intends to slash defense spending.

Notably, a significant portion of Palantir’s revenue comes from defense contracts, where it provides software and artificial intelligence (AI) solutions to the Department of Defense (DoD).

Much of PLTR’s meteoric rise can be attributed to its consistent success in securing high-profile DoD contracts. Therefore, as a leading defense contractor, slashing the budget will likely impact the company’s future growth.

At the same time, insider selling plans appear to be unsettling investors. CEO Alex Karp is reportedly planning to offload up to $1.2 billion worth of shares. Such large-scale insider sales are generally perceived as a lack of confidence in a company’s short-term outlook, leading to weakened investor sentiment.

Wall Street divided on PLTR stock

Palantir’s decline may not surprise some market players, as some Wall Street analysts have been warning of an impending crash for the software giant. For instance, as reported by Finbold, Jefferies expects the stock to drop to $60, citing its high valuation.

Beyond valuation concerns, the firm’s analyst Brent Thill, who holds an ‘Underperform’ rating on PLTR, flagged slowing hiring growth as a significant concern. He suggested this could indicate limited AI opportunities, cost-cutting in non-engineering roles, or over-hiring in previous years.

Thill also noted an imbalance in Palantir’s revenue growth. While U.S. revenue surged 38% year-over-year in 2024, up from 32% in 2023, international revenue stagnated at 14% growth. This disparity raises concerns about Palantir’s ability to scale globally as its non-U.S. business struggles to keep up with domestic expansion.

Wedbush Securities analyst Dan Ives has a dissenting opinion on PLTR, stating that the company is poised to lead the software AI segment. Interestingly, he has dismissed overvaluation concerns, labeling Palantir the ‘Messi of AI.’

Meanwhile, Loop Capital initiated coverage with a ‘Buy’ rating and a $141 price target, citing Palantir’s strong position in AI and GenAI as major market opportunities.

Featured image via Shutterstock