Seagate Technology (NASDAQ: STX) stock has emerged as one of the strongest-performing artificial intelligence (AI) infrastructure plays of 2026.

Notably, over the past year, the data storage company’s stock has gained 594%, while year-to-date it is up 182%, having closed the last session at $812.

The rally has transformed Seagate from what was long viewed as a cyclical hard disk drive maker into a major beneficiary of the AI boom.

Part of the growing institutional confidence comes from BlackRock, which holds approximately 14.27 million Seagate shares, representing about 6.37% of the company’s outstanding stock.

Seagate’s recent financial results have strengthened bullish sentiment. In fiscal Q3 2026, the company reported revenue of $3.11 billion, up 44% year over year, while non-GAAP EPS surged 115% to $4.10, beating expectations. In Q2 2026, revenue reached $2.83 billion, with non-GAAP EPS of $3.11.

Growth has been driven by strong data center demand for nearline drives, helping gross margins expand into the low- to mid-40% range. Seagate has also advanced its Mozaic HAMR platform, now shipping 44TB drives to hyperscale cloud providers while targeting 100TB drives in the future.

Demand remains strong, with nearline production reportedly fully allocated through 2026 and customer discussions already extending into 2027 and 2028, supported by rising AI-related storage needs.

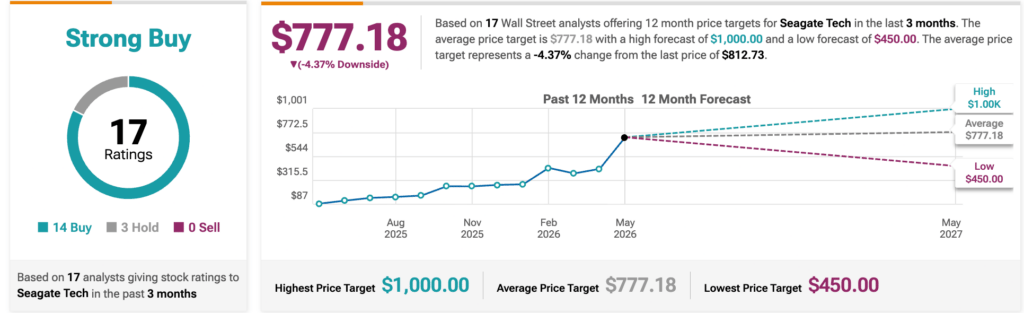

Wall Street analysts bullish on STX stock

Meanwhile, analysts remain bullish on Seagate Technology despite the stock’s explosive rally over the past year. According to data from TipRanks based on 17 Wall Street analysts, Seagate currently holds a ‘Strong Buy’ consensus rating, with 14 buy ratings, three holds, and no sell recommendations.

The average 12-month price target stands at $777.18, implying a modest 4.37% downside, with the highest target at $1,000 and the lowest at $450, reflecting mixed expectations after the stock’s sharp surge.

Concerns about STX stock

Seagate’s massive rally has also raised valuation concerns, with STX stock now trading at about 77 times trailing earnings, with a market capitalization above $180 billion, leaving it vulnerable to any slowdown in AI spending, easing storage demand, or faster adoption of alternative technologies.

Competition from Western Digital remains a key risk as both companies expand next-generation high-capacity drives. Investors are also watching Seagate’s ability to scale production and secure new customer deals.

However, Seagate’s manufacturing scale, sold-out order book, and leadership in HAMR technology continue to support its position in the AI infrastructure market.While long-term investors bullish on AI and data growth may still see upside, more cautious investors could wait for pullbacks or consider diversified AI-focused funds instead.