American data cloud storage company Snowflake (NYSE: SNOW) is signaling a potential bullish shift after the stock struggled in recent months.

SNOW’s momentum is largely tied to the company’s inroads in the artificial intelligence (AI) sector, where it has at least 1,000 deployed use cases and more than 3,200 accounts utilizing its AI features.

Snowflake’s growing prowess in AI can be attributed to its product being deemed to support interoperability and data transformation capabilities. At the same time, the firm’s potential is reaffirmed by its existing key partnerships with entities such as Microsoft (NASDAQ: MSFT).

Regarding stock price movement, SNOW has gained 21% year to date, ending the last trading session at $187.60. These short-term gains are crucial as the equity attempts to erase the 18% losses incurred over the past year.

SNOW is ‘starting to turn heads’

Now, analysis from charting platform TrendSpider in an X post on February 14 highlighted that Snowflake is ‘starting to turn heads’ due to its price movement and several fundamental developments.

For instance, after struggling with a prolonged downtrend, SNOW is breaking out of a major monthly base. The stock has recently pushed above a long-term descending trendline below $150, which has acted as resistance since early 2022. This breakout, strong insider buying, and improving fundamentals suggest that SNOW could be setting up for a significantly higher move.

On June 7, 2024, Michael Speiser, a director at the firm, acquired $10 million worth of shares, while CEO Sridhar Ramaswamy made a $5 million purchase on March 25.

Historically, such substantial insider activity—especially near the stock’s lows—suggests growing confidence in Snowflake’s prospects.

Adding to its appeal, Snowflake has demonstrated strong and consistent revenue growth in recent quarters, highlighting its potential for further expansion in a high-demand sector.

In the most recent quarter, ending October 31, 2024, Snowflake exceeded analyst expectations. The company reported adjusted earnings of $0.20 per share, surpassing the $0.15 expected by analysts.

Revenue came in at $942 million, beating estimates of $897 million. Product revenue accounted for 96% of total sales, with the company now forecasting $3.43 billion in fiscal 2025 product revenue, implying 29% growth.

Despite the 28% year-over-year revenue growth, Snowflake’s net loss widened to $324.3 million compared to $214.3 million in the same period last year.

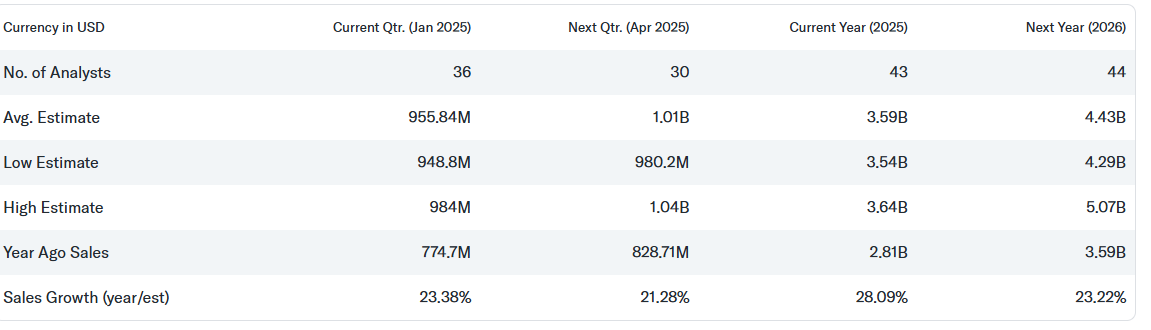

Looking ahead, Snowflake is expected to report $955.84 million in revenue for the January 2025 quarter, a 23.38% increase year over year. Analysts project $3.59 billion in revenue for fiscal 2025, up 28.09%, with 2026 estimates reaching $4.43 billion, reflecting 23.22% growth.

Snowflake AI potential

Regarding Snowflake’s future growth, the stock has the potential for further momentum, primarily due to the company’s investment in AI technology. Snowflake’s AI-powered solutions enable customers to interact with data using natural language processing, retrieve insights quickly, and customize models without coding expertise.

Indeed, this user-friendly approach positions Snowflake for significant interest, especially as the company expects its total addressable market to double to $342 billion by 2028.

In summary, Snowflake’s AI-driven growth and insider confidence signal upside potential, but risks remain. Ongoing net losses, competition, and the need for sustained growth could challenge its momentum. Still, its expanding market and strategic positioning make it a stock to watch.

Featured image via Shutterstock