Jim Cramer, American author, journalist, and host of CNBC’s Mad Money, is once again living up to his title of Wall Street’s leading inverse indicator.

On Thursday, July 31, just hours ahead of Figma’s (NYSE: FIG) stock market debut, Cramer urged investors to stay clear of the web design company, suggesting it was “way too expensive” with nearly 54 times sales and assumed 40% growth.

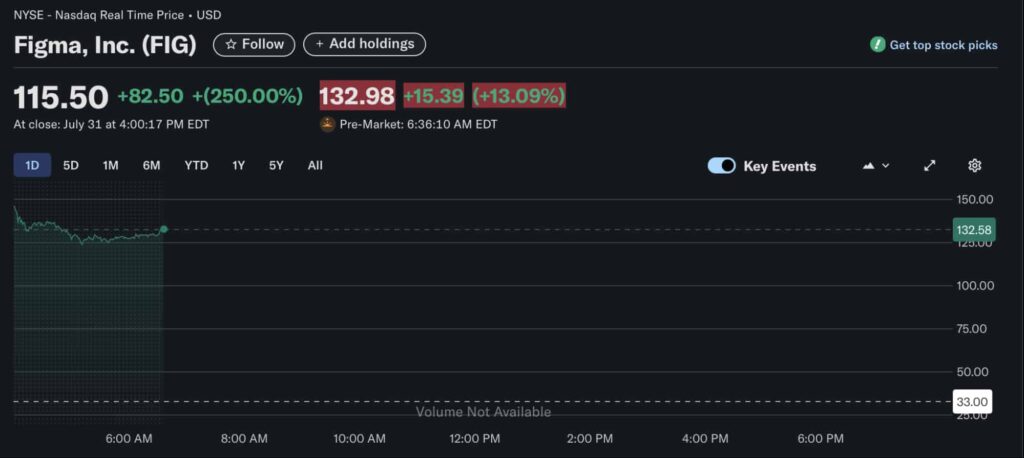

The company had priced its initial public offering (IPO) at $33 per share on July 30, raising roughly $411 million through the sale of 36.9 million Class A shares.

However, Figma shares skyrocketed 250% to close at $115.50 after the debut, proving Cramer’s forecast wrong and securing a market cap of $56.3 billion.

At press time, August 1, Figma shares were sitting at $132.51, up 13% in pre-market.

Every. Single. Time. https://t.co/NYxKTweU7d pic.twitter.com/RmrDhuoBEk

— Inverse Cramer (@CramerTracker) July 31, 2025

Figma IPO and Inverse Cramer theory

The quick surge added fuel to the so-called Inverse Cramer theory, the idea that stocks often do the opposite of what Cramer believes.

Indeed, despite valuation concerns voiced by the CNBC host, Figma’s financials appear strong. For instance, the San Francisco company posted a Net Dollar Retention Rate of 134% and $749 million in revenue for 2024, up 48% year-over-year.

Continuing the trend, its first quarter for fiscal 2025 saw an additional $228.2 million in revenue, with clients such as Microsoft (NASDAQ: MSFT) and Alphabet (NASDAQ: GOOGL) now relying on Figma’s tools and services.

Figma’s IPO comes less than a year after Adobe’s (NASDAQ: ADBE) failed $20 billion acquisition of the firm, which appears to have contributed to the successful launch, as it allowed the team to focus on product development in a period of positive sentiment toward cloud-based platforms.

Featured image via Shutterstock