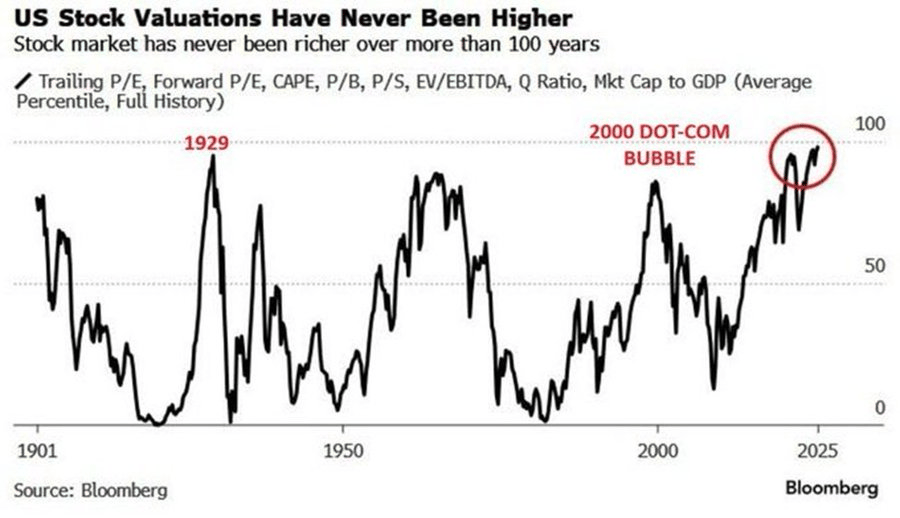

The U.S. stock market has entered valuation territory that now exceeds levels recorded before the 1929 crash that triggered the Great Depression.

Recent valuation data show the market trading at some of the most expensive levels in modern history, with composite measures averaging key indicators such as the Shiller CAPE ratio, price-to-book value, and other long-term metrics climbing beyond the extremes seen ahead of the 1929 collapse.

At the center of the warning is the Shiller CAPE ratio for the S&P 500, which stood between 39 and 41 as of late May 2026.

The reading is more than double its historical average of approximately 17 and has only been surpassed during the peak of the dot-com bubble in 2000.

The latest figures indicate that U.S. stock market valuations are now firmly within a range historically associated with periods of excessive investor optimism.

Notably, composite valuation measures have moved above the levels reached before the 1929 crash while remaining slightly below the peak recorded during the technology bubble of 2000.

The data suggests investors are paying historically high premiums for corporate earnings and assets despite a backdrop of economic and geopolitical uncertainty.

The rally has been driven largely by a handful of AI-linked technology giants whose strong earnings have pushed the broader market to record highs.

However, the growing concentration in mega-cap stocks leaves the market vulnerable if AI spending falls short of expectations.

History suggests such valuation extremes leave little room for error. The 1929 crash led to an 83% market decline, while the Dot-com bust wiped out trillions of dollars in investor wealth.

U.S. stock market risks

Several risks could threaten the U.S. stock market. Persistent inflation and potential disruptions to global energy supplies could keep interest rates higher for longer, increasing borrowing costs and pressuring valuations.

Higher rates would weigh on consumers and businesses carrying significant debt, while stress in private credit markets and growing U.S. fiscal challenges could push bond yields higher and pressure stocks, housing, and investment.

Meanwhile, softer hiring trends, partly linked to AI-driven efficiencies, may weaken consumer spending.

Still, a downturn is not inevitable. Strong earnings growth, AI-driven productivity gains, and resilient corporate balance sheets could continue supporting the U.S. stock market despite historically elevated valuations.