A Wall Street analyst has reiterated a bullish call on Apple’s (NASDAQ: AAPL) stock price target, even as the equity continues to show short-term weakness.

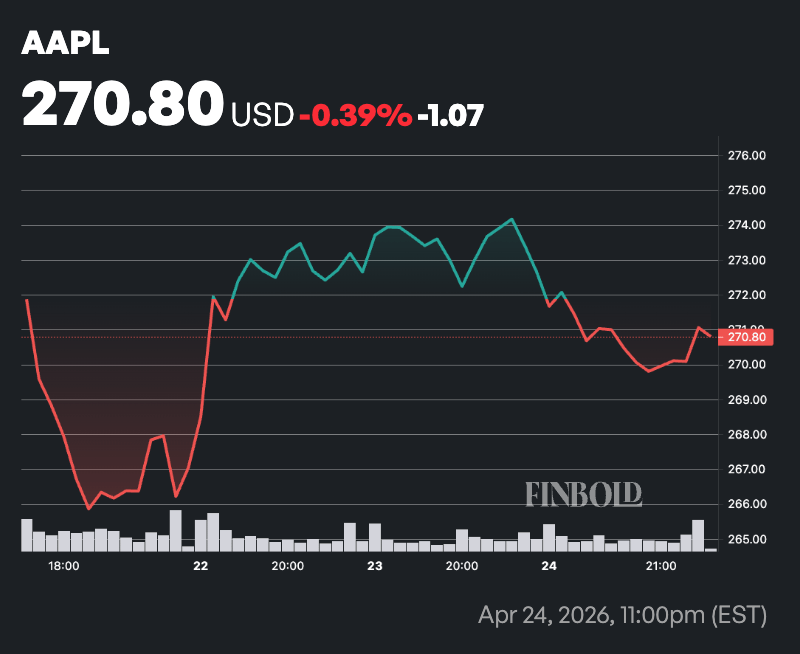

As of press time, AAPL shares were valued at $271, having ended the last session down 0.87%. In pre-market trading on Monday, Apple stock was down 1.57% to $266.

Regarding the outlook, Amit Daryanani of Evercore assigned AAPL an ‘Outperform’ rating and maintained a $330 price target.

The updated view signals confidence in Apple’s near-term fundamentals, driven by stronger iPhone performance.

Revenue from the flagship product is expected to grow about 20% year over year, beating broader market expectations, with demand for higher-end models supporting pricing and reinforcing its premium positioning.

The analyst also pointed to Apple’s services segment, which is projected to sustain mid-teens growth, led by strength in Apple Pay, iCloud, and licensing.

Despite some moderation in App Store trends, overall services revenue remains resilient, supported by a growing installed base and higher user engagement.

Improving demand in China is also lifting the outlook, with unit growth returning to double digits, signaling stabilizing conditions in a key market.

Margins remain in focus, with March-quarter gross margin expected in the high-40% range before a slight dip in June. Cost discipline and premium pricing are likely to help offset pressures.

Wall Street bullish on Apple

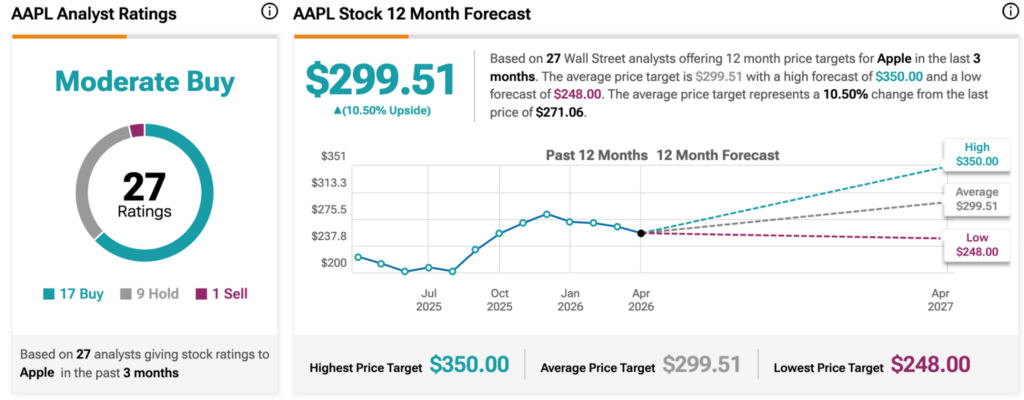

Meanwhile, the Evercore target is higher compared to the broader Wall Street consensus, as tracked by TipRanks. According to 27 analysts, Apple carries a ‘Moderate Buy’ rating. Of these, 17 recommend buying the stock, nine suggest holding, and one advises selling, underscoring continued confidence in the company’s fundamentals.

The average 12-month price target stands at $299.51, implying roughly 10.5% upside from the most recent trading level of $271.06. Projections vary, with the highest estimate reaching $350 and the lowest coming in at $248.

The bullish outlook comes as Apple continues to post solid growth in its iPhone segment. In this line, according to Bernstein SocGen Group, iPhone revenue rose 13% year over year in the March quarter, supported by an approximate 10% increase in unit sales.

Growth was largely driven by strong demand for more affordable models such as the iPhone 17e, which helped lift overall shipment volumes.

However, the shift toward lower-priced devices has weighed on average selling prices, creating some pressure on margins despite the top-line gains.

This performance comes against the backdrop of a subdued global smartphone market, where Apple still managed to gain market share and secure the top position in unit sales for the quarter.