A Wall Street analyst has reaffirmed a bullish outlook on Meta Platforms (NASDAQ: META), while highlighting a potential $20 billion subscription revenue opportunity that could support long-term growth.

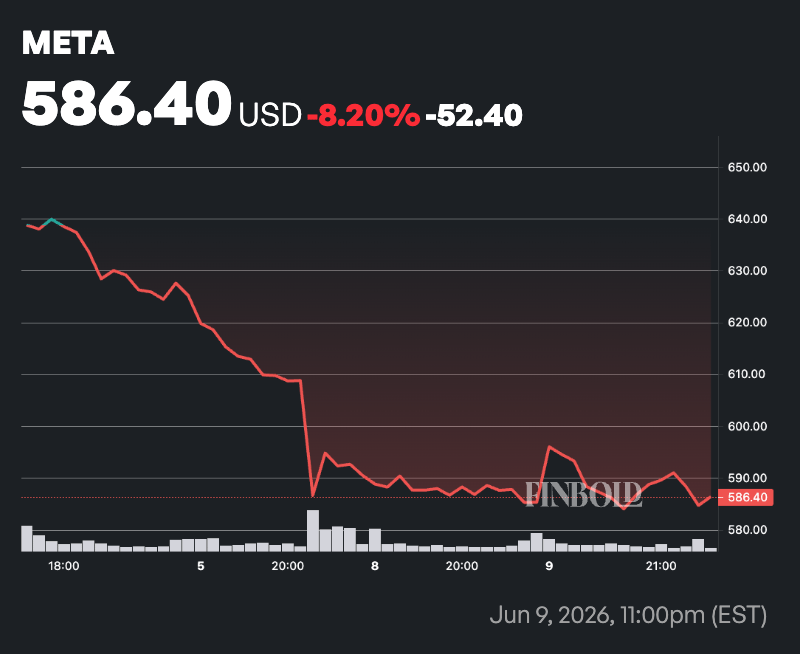

On June 9, Truist Securities analyst Youssef Squali reiterated his ‘Buy’ rating on Meta and maintained its $840 price target. Based on the stock’s price of $584 at the time of the update, the target implies upside potential of about 43%.

The firm remains optimistic about Meta’s ability to outgrow the broader digital advertising market while expanding into new high-margin revenue streams.

According to Truist, subscriptions could become a meaningful contributor to the company’s business by fiscal 2030.

The firm’s bullish thesis centers on Meta’s expanding subscription strategy across platforms, including Facebook, Instagram, WhatsApp, and Meta AI.

Truist estimates subscription products could generate more than $20 billion in annual high-margin revenue by fiscal 2030, representing roughly 5% of Meta’s total revenue. The forecast assumes user adoption levels similar to Google’s subscription penetration rate of about 3%.

Meta has launched several premium subscription offerings across its platforms, which Truist believes could diversify revenue beyond advertising.

The firm expects subscriptions to support long-term growth, reduce reliance on ad sales, and boost profitability through high-margin recurring revenue.

Wall Street bullish on Meta stock outlook

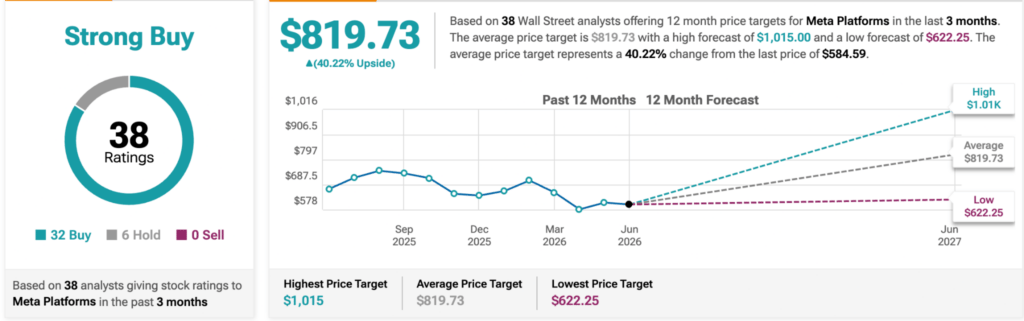

Meta continues to enjoy strong support from Wall Street analysts, with the average 12-month price target implying more than 40% upside from current levels.

According to data from TipRanks, Meta holds a consensus ‘Strong Buy’ rating based on 38 analyst ratings, including 32 ‘Buy’ recommendations, six ‘Holds’, and no ‘Sell’ ratings.

The average Meta stock price target stands at $819, implying upside of about 40% from the latest share price. Analyst targets range from a low of $622 to a high of $1,015 over the next 12 months.

The positive sentiment reflects confidence in Meta’s ability to sustain growth in digital advertising while expanding revenue opportunities tied to artificial intelligence and subscription services.

Although analysts differ on the magnitude of future gains, the absence of any Sell ratings underscores broad confidence in Meta’s long-term outlook.