Wall Street analysts remain cautious on Lucid Group (NASDAQ: LCID), but their latest forecasts suggest the electric vehicle maker could deliver notable upside over the next 12 months.

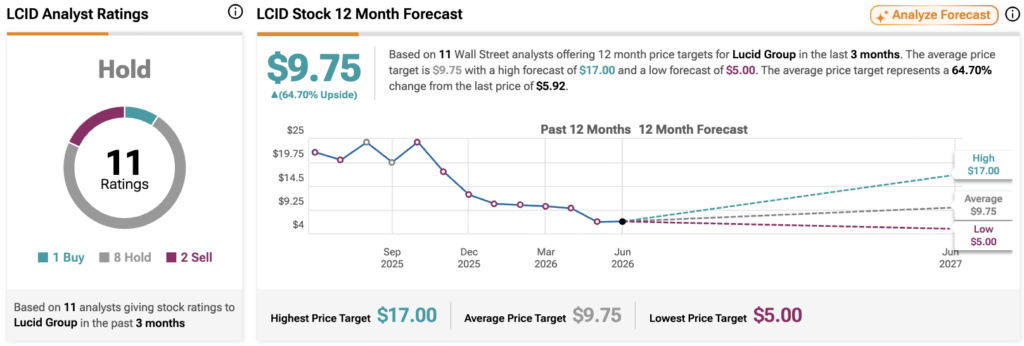

According to data compiled from 11 analysts on TipRanks, the average LCID stock price target stands at $9.75, representing a potential upside of about 64.7% from the closing price of $5.92.

The highest Lucid stock price target is $17, while the lowest is $5. The average target of $9.75 sits between those extremes and reflects Wall Street’s consensus expectation for the next 12 months.

The consensus rating is ‘Hold’. In this case, among the analysts covering the stock, one recommends ‘Buy’, eight rate it ‘Hold’, and two maintain ‘Sell’ ratings.

The outlook reflects a market that sees growth opportunities but remains cautious about the challenges facing the luxury EV maker, including profitability concerns and competition from larger automakers.

The bullish forecast suggests analysts see a path for Lucid to successfully execute its growth strategy and expand vehicle deliveries. Meanwhile, the bearish target indicates concerns about execution risks and broader industry headwinds.

LCID stock analyst breakdown

Among the analysts, Citi’s Michael Ward lowered his Lucid stock price target to $14 from $17 following weaker-than-expected first-quarter 2026 results and the withdrawal of the company’s full-year outlook, while maintaining a ‘Buy’ rating. Ward acknowledged concerns over Lucid’s $282 million in revenue, roughly $1 billion net loss, and ongoing execution challenges, but argued that the company’s long-term investment case remains intact. His bullish stance is largely tied to expected catalysts in 2027, particularly the launch of production at Lucid’s new Saudi Arabia plant and lower capital expenditures, which Citi believes could improve manufacturing economics and support the company’s path to profitability.

Needham’s Andrew Percoco, on the other hand, maintained a ‘Hold’ rating after Lucid’s first-quarter 2026 results, arguing that while the long-term growth story remains supported by initiatives such as the Uber-Nuro robotaxi partnership, the Gravity production ramp, and development of the Midsize platform, significant challenges persist. The firm noted that Lucid’s recent capital raise strengthens its liquidity position through the second half of 2027, but pointed to elevated inventory levels, deteriorating gross margins, negative unit economics, and weak EV demand as key risks.

On the other hand, Morgan Stanley analyst Adam Jonas reiterated his ‘Underweight’ rating and cut his price target to $5 from $10 following the company’s disappointing first-quarter 2026 results. Jonas cited several concerns, including the temporary stop-sale of the Gravity SUV due to a supplier-related quality issue, the withdrawal of Lucid’s 2026 production guidance, leadership uncertainty during the CEO transition, and ongoing operational challenges. He also highlighted weak delivery figures, deeply negative gross margins, and substantial cash burn, arguing that Lucid is likely to remain under pressure until management provides greater clarity on its strategy and execution plans.