Despite weakness in Amazon’s (NASDAQ: AMZN) stock following its earnings release, Wall Street analysts remain broadly bullish on the shares over the coming year.

Amazon ended the latest trading session down about 5.5%, trading near $210, as investors reacted to higher-than-expected capital expenditure plans.

Shares fell after the company signaled that capital spending could reach roughly $200 billion by 2026, raising concerns about how quickly its aggressive AI investments will translate into returns.

Amazon Q4 2025 earnings

In the final quarter of 2025, Amazon reported earnings per share of $1.95, slightly below Wall Street estimates of $1.97. Revenue rose to $213.39 billion, beating expectations of $211.33 billion.

Performance was supported by high-margin segments, with Amazon Web Services generating $35.58 billion in revenue versus forecasts of $34.93 billion, while advertising revenue reached $21.32 billion, also ahead of estimates.

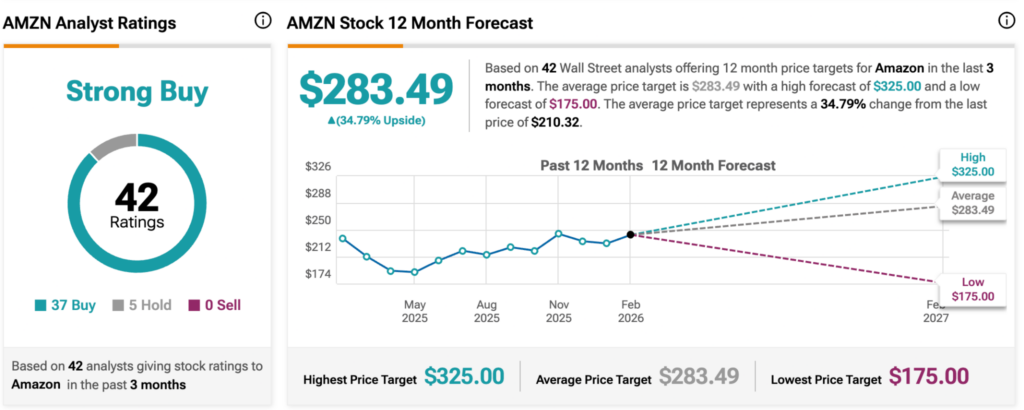

Despite near-term volatility, analysts tracked by TipRanks remain optimistic on the stock’s outlook. Based on ratings from 42 analysts, Amazon holds a ‘Strong Buy’ consensus, with 37 ‘Buy’ ratings, five holds, and no ‘Sell’ ratings. The average 12-month price target is $283.49, implying upside of about 34.8%. The highest target is $325, while the lowest is $175.

Analysts’ take on AMZN share price

Among the analysts on February 6, RBC Capital’s Brad Erickson reiterated an ‘Outperform’ rating with a $300 price target, citing confidence in Amazon’s long-term, AI-driven growth. He acknowledged risks from higher 2026 capital expenditures, intensifying cloud competition, and margin pressure from the Project Kuiper rollout, but said these are outweighed by Amazon’s strengthening leadership in AI and AWS. Erickson pointed to accelerating AWS momentum, rising custom chip revenue, expanding capacity, and resilient margins as signs that AWS monetization remains underappreciated.

Goldman Sachs analyst Eric Sheridan lowered his price target to $280 from $300 while maintaining a ‘Buy’ rating, citing increased investor sensitivity to Amazon’s expanding investment cycle. He noted that while AWS growth is re-accelerating on both AI and non-AI demand and margins reached a stronger-than-expected 35%, markets will focus on whether higher spending drives sustained AWS revenue and backlog growth.

Truist Securities analyst Youssef Squali also cut his price target to $280 from $290 but kept a ‘Buy’ rating. He cited higher near-term costs tied to aggressive investment, despite Q4 2025 results beating expectations across Online Stores, Advertising, and AWS, where growth accelerated to 24% year over year. Squali noted that Q1 2026 guidance points to softer operating income due to increased spending on low Earth orbit initiatives, quick commerce, and international expansion, while maintaining a positive long-term view.

By contrast, DA Davidson analyst Gil Luria downgraded Amazon to ‘Neutral’ from ‘Buy’ and lowered his price target to $175. He raised concerns about AWS losing ground to Microsoft and Google, forcing heavier investment to defend market share, and warned of longer-term risks to the retail business as the internet becomes more chat-driven, led by platforms such as Gemini and ChatGPT.

Featured image via Shutterstock