Wall Street analysts are reacting to Advanced Micro Devices’ (NASDAQ: AMD) Q4 2025 earnings with mixed price outlooks, even as the stock suffers short-term losses.

For the quarter, the chipmaker posted stronger-than-expected results, but a softer-than-hoped outlook for the current quarter weighed on investor sentiment and sent the stock sharply lower.

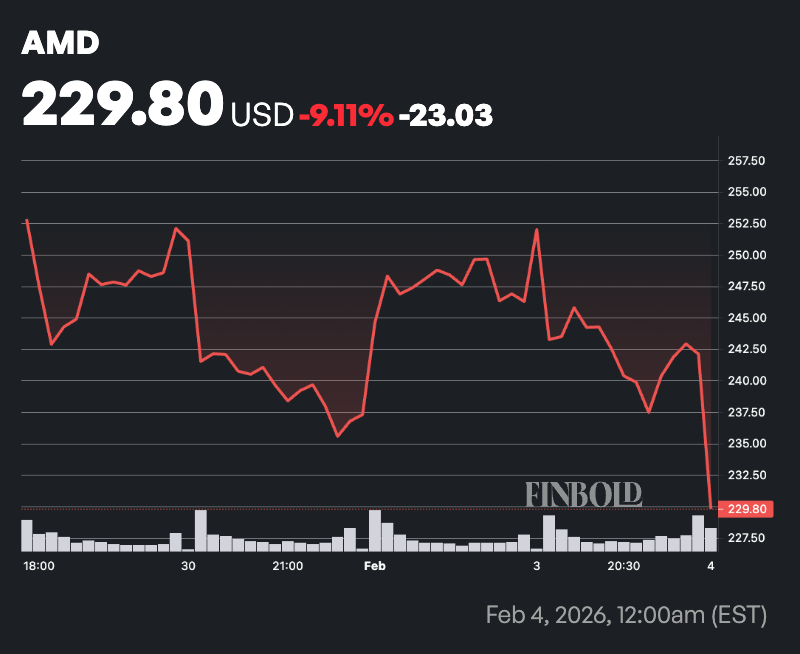

By the close of Tuesday’s session, AMD shares were down 1.6% at $242. Losses extended in premarket trading on Wednesday, with the stock down 7.6% to about $223.

AMD earnings

AMD reported earnings of $1.53 per share on revenue of $10.27 billion, comfortably beating LSEG consensus estimates of $1.32 per share and $9.67 billion in revenue. Net income surged to $1.51 billion, or 92 cents per share, from $482 million, or 29 cents per share, a year earlier, as revenue rose 34% year over year.

Despite the strong quarter, AMD’s first-quarter revenue forecast of about $9.8 billion, plus or minus $300 million, disappointed some analysts who had expected stronger guidance amid accelerating artificial intelligence spending.

Following the earnings report, Wall Street analysts remain cautiously optimistic on AMD shares. According to TipRanks, the stock carries a Strong Buy rating based on 35 analyst reviews.

Of those, 27 analysts rate AMD a Buy, eight recommend holding the shares, and none suggest selling.

The analysts have set an average 12-month price target of $286.50, implying upside of about 18.3% from the recent price. The most bullish forecasts see the stock reaching $377, while the lowest target stands at $210.

Analysts’ take on AMD stock

Among recent updates, KeyBanc Capital Markets on February 4 raised its AMD price target to $300 from $270 and maintained an ‘Overweight’ rating. The firm’s analyst John Vinh, cited stronger fundamentals led by the data center business and a more resilient near-term outlook than typical seasonality.

KeyBanc said data center results continue to outperform, with quarter-over-quarter growth holding up even as other segments soften, underscoring AMD’s increasing reliance on high-performance computing and AI demand. While recent results and guidance benefited in part from MI308 shipments to China that are not expected to recur, the firm said the long-term thesis remains intact, with next-generation MI450 and Helios products set to ramp from the third quarter of 2026 and reach meaningful volumes by the fourth quarter.

TD Cowen analyst Joshua Buchalter reiterated a ‘Buy’ rating on AMD with a $290 price target, saying the company continues to execute well despite a challenging operating backdrop. He said the latest quarter and outlook beat consensus after adjusting for one-off China-related factors, showing AMD is managing volatility in data center and PC demand better than peers.

Buchalter added that expected sequential growth in data center GPUs and server CPUs during the typically weak March quarter supports the view that AI-driven demand and AMD’s competitive positioning remain strong. He said the long-term thesis is anchored in the MI450 and Helios accelerator ramp beginning in the third quarter of 2026 and accelerating into 2027, followed by the MI500 platform.

In a separate note, Roth MKM also reiterated a ‘Buy’ rating on AMD and maintained its $300 price target, citing the company’s expanding presence in data center and AI markets and its ability to sustain momentum across key product cycles.

Featured image via Shutterstock