Wall Street analysts are maintaining a bullish outlook on Broadcom (NASDAQ: AVGO) stock for the next 12 months as the company solidifies its position as one of the leading beneficiaries of the artificial intelligence infrastructure boom.

Notably, Broadcom shares have posted impressive gains over the past year amid investor enthusiasm for AI-related plays.

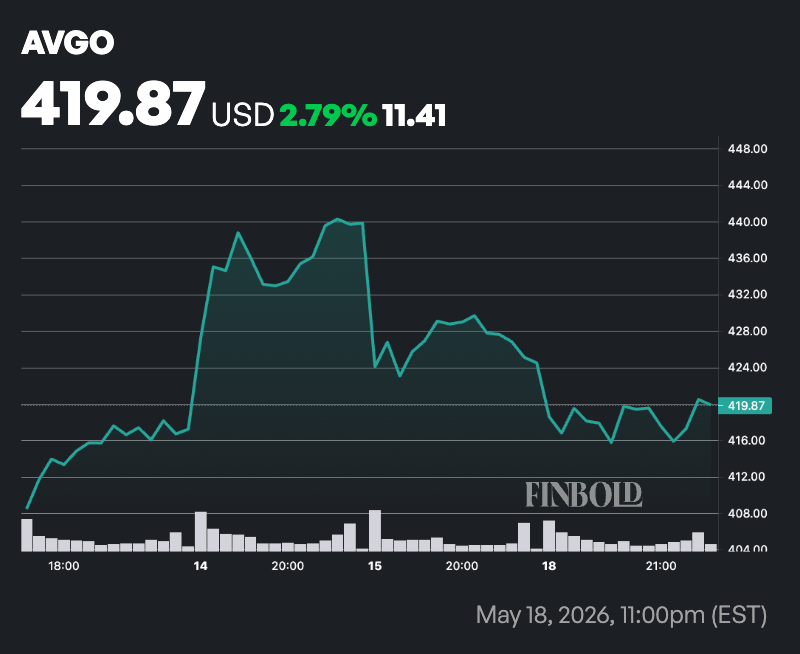

At the close of the last trading session, AVGO stock was trading at $420 after ending the day down 1%. Year to date, the equity has rallied about 21%.

Despite the short-term struggle, Broadcom’s fundamentals remain strong. In the first quarter of fiscal 2026, the company posted record revenue of $19.31 billion, up 29% year over year.

AI semiconductor revenue surged to $8.4 billion, more than doubling from a year earlier, fueled by strong demand for custom XPUs and Ethernet switches from hyperscalers such as Google, Meta, Anthropic, and OpenAI.

Management projected second-quarter AI semiconductor revenue of $10.7 billion and said it expects cumulative AI silicon revenue to surpass $100 billion by 2027.

At the same time, the integration of VMware has strengthened Broadcom’s business model, contributing about $6.8 billion in high-margin infrastructure software revenue during the quarter.

The business is increasingly shifting toward recurring subscription revenue, improving visibility and helping balance the cyclical semiconductor segment. Strong free cash flow has also supported share buybacks and dividend growth, boosting investor confidence.

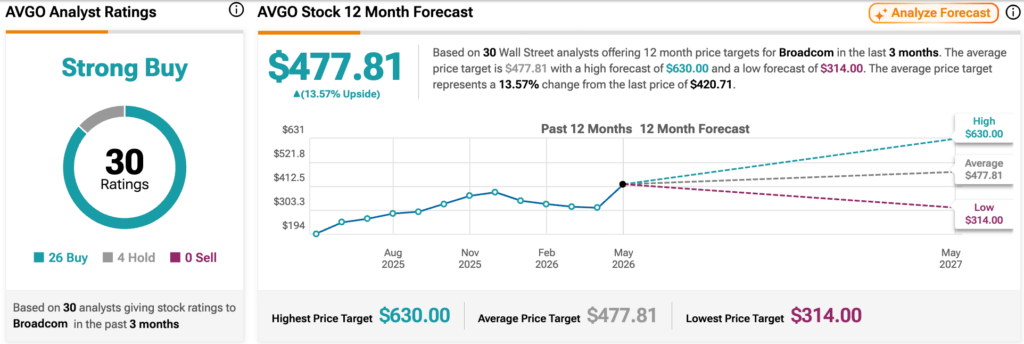

For the stock outlook, Wall Street analysts have established a strongly bullish consensus on AVGO shares. Based on 30 analysts tracked by TipRanks, the average 12-month price target stands at $477.81, implying a potential 13.57% upside.

The ratings breakdown includes 26 ‘Buy’ recommendations and four ‘Holds,’ resulting in an overall ‘Strong Buy’ consensus with no Sell ratings. Targets range from a low of $314 to a high of $630.

AVGO analysts take breakdown

Among the analysts, Mark Lipacis of Evercore ISI on May 18 raised his price target on Broadcom to $582 from $490 while maintaining an ‘Outperform’ rating, citing stronger confidence in the company’s AI positioning. Following first-quarter AI supply chain checks, the analyst said the market is expected to transition from training-focused AI workloads to inference-driven demand by late 2026, pushing cloud providers to prioritize lower costs, improved returns on investment, and total cost efficiency.

On the same date, UBS also raised its AVGO price target to $490 from $475 while maintaining a ‘Buy’ rating ahead of the company’s June earnings report, arguing that improved profitability from AI chip deals could outweigh lower revenue projections. Analyst Timothy Arcuri noted that Broadcom restructured its agreement with Anthropic by shifting from full-rack systems to a standardized ASIC model, reducing expected revenue contribution while significantly improving margins. Despite trimming long-term AI revenue and earnings forecasts, UBS remains optimistic on Broadcom’s outlook, citing strong AI demand, expectations for revenue guidance above Wall Street estimates, and the company’s rapid AI-related growth.

TD Cowen analyst Joshua Buchalter raised the firm’s price target on Broadcom to $500 from $405 while maintaining a ‘Buy’ rating, citing continued strength in AI-related demand and shifting priorities within AI infrastructure. The firm said investors are increasingly focused on identifying the next supply constraints beyond AI accelerators, with optical networking companies outperforming as hyperscalers expand data center capacity.