Although Lucid stock (NASDAQ: LCID) is facing bearish sentiment in the short term, Wall Street analysts project possible upside in the coming year.

At the close of the last session, LCID was valued at $22, down 8.3%, while year-to-date the shares have plunged nearly 30%.

The decline follows weaker-than-expected deliveries and a cut in annual production guidance. Notably, Lucid delivered 4,078 vehicles in Q3, up 47% year over year but short of Wall Street’s 4,286 estimate. The company now expects 18,000–20,000 vehicles this year, below earlier targets.

The sell-off has also been fueled by the expiration of the $7,500 U.S. EV tax credit, a recent 1-for-10 reverse stock split viewed negatively by investors, and persistent concerns over cash burn.

Lucid stock price prediction

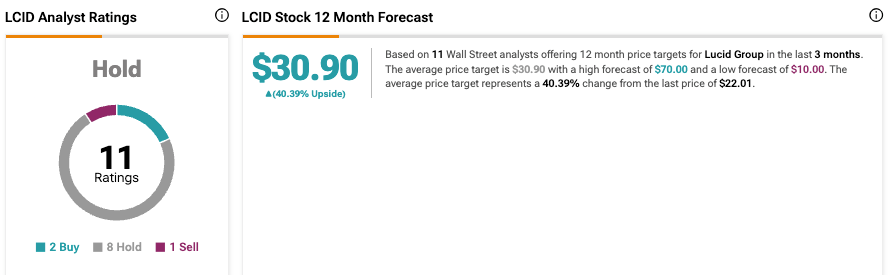

On Wall Street, 11 analyst ratings compiled by TipRanks give Lucid a consensus rating of ‘Hold’. Of the 11, two recommend buying the stock, eight suggest holding, and one advises selling.

Analysts’ 12-month price forecasts place Lucid at an average target of $30.90, implying a potential upside of about 40% from current levels. The most optimistic forecast values the stock at $70, while the lowest projects $10.

On October 6, Cantor Fitzgerald’s Andres Sheppard reaffirmed a ‘Neutral’ rating and $26 price target, citing Lucid’s strong balance sheet and production momentum, with over 10,000 vehicles delivered in 2024 and more than 6,400 in the first half of 2025.

Earlier in September, Stifel analyst Stephen Gengaro raised Lucid’s price target to $21 from $2.10 to reflect its 1-for-10 reverse stock split, while maintaining a ‘Hold’ rating. He emphasized the move was technical and not a fundamental change in the firm’s outlook, despite Lucid’s efforts to stabilize its share price and maintain listing compliance.

Featured image via Shutterstock