Wall Street analysts project that Lucid (NASDAQ: LCID) stock could rally more than 50% over the next 12 months, despite the equity starting the year on a volatile note.

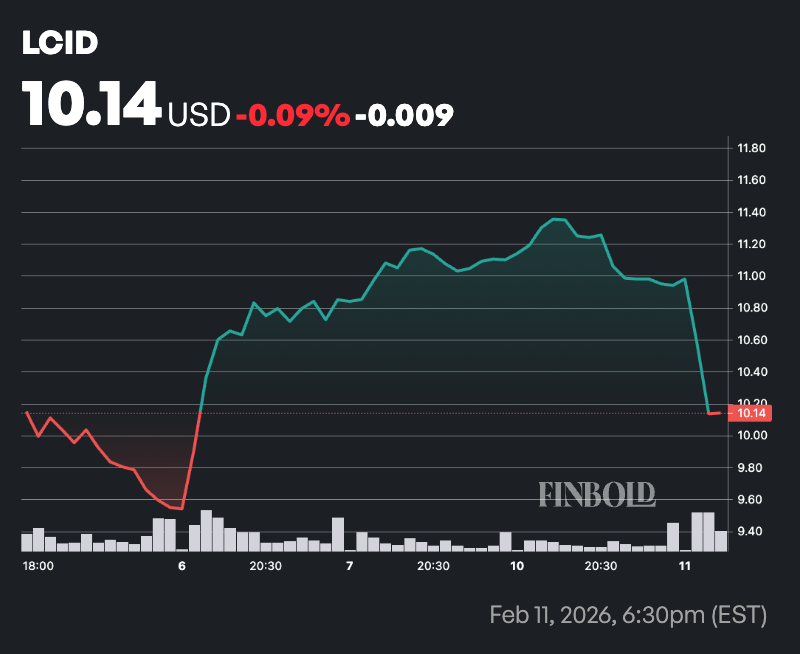

As of press time, LCID shares were trading at $10, down over 2% on the day and nearly 5% year-to-date, as the electric vehicle manufacturer continues to face pressure.

The stock is in focus ahead of the company’s fourth-quarter 2025 earnings report on February 24, when investors will closely watch revenue and vehicle deliveries.

Analysts expect revenue to surge nearly 97% year over year in Q4 to about $461.5 million. However, Lucid still faces ongoing losses, cash constraints, and intense competition in the EV sector.

Recent developments could influence price performance, such as the company’s appointment of Neil Marsons as Senior Vice President of Supply Chain to improve operational efficiency, the Lucid Air performing strongly in extreme cold tests, and institutional interest has increased, with UBS nearly doubling its stake in late 2025.

The upcoming earnings report should also provide clarity on production ramps, Gravity SUV momentum, and the path toward profitability.

Lucid stock outlook

According to TipRanks data based on six analysts, Lucid’s outlook carries one ‘Buy’, four ‘Hold’, and one ‘Sell’ rating, resulting in an overall ‘Hold’ consensus.

The average 12-month price target is $17, implying about 61% upside from current levels. Notably, LCID stock price targets range from a low of $10 to a high of $30.

Among the analysts, in November 2025, Stifel’s Stephen Gengaro lowered his price target to $17 from $21 while maintaining a ‘Hold’ rating after Lucid reported record third-quarter revenue of $336.6 million that still missed expectations. Although revenue grew 45.86% year over year, the company reduced its 2025 production guidance to 18,000 vehicles from a prior 18,000–20,000 range and indicated fourth-quarter output would be weighted toward the Gravity SUV. Stifel cited concerns about Lucid’s capital needs as it continues to burn cash, despite a current ratio of 1.81.

In late 2025, CFRA’s Garrett Nelson assigned a $10 price target and a ‘Strong Sell’ rating, arguing that while Lucid posted year-over-year volume growth, sales fell short of expectations even ahead of expiring federal EV tax credits that boosted demand for other automakers.

By contrast, Benchmark’s Mickey Legg set a $70 price target, citing expectations of stronger EV adoption in 2026, confidence in Lucid’s technology and vertically integrated manufacturing, and continued financial backing from Saudi Arabia.

Featured image via Shutterstock