While the first two quarters were not the most impressive for Tesla (NASDAQ: TSLA), the automaker started picking up the pace in late summer 2025, with a 7.4% increase in total car deliveries.

As a result, the company’s shares have climbed 30% from around $329 on September 2 to $423 at press time on October 17, setting its year-to-date returns at 4.87%.

Tesla’s third-quarter earnings report is scheduled for October 22, and while earnings projections of $0.41 per share (EPS), according to Barchart, imply a significant drop from $0.62 in the same period last year, Tesla’s aforementioned delivery statistics suggest the result might actually be surprisingly positive.

What’s more, lower costs per vehicle and higher output could also stabilize despite the revenue, while the ever-growing focus on autonomous driving, artificial intelligence (AI), and robotics could shift the business model toward more high-margin services.

Nonetheless, the impressive Q3 delivery surge could be due to the federal EV tax credit of $7,500, which expired in September, prompting customers to accelerate their purchases. In other words, Elon Musk’s golden goose may have already reaped all of the benefits, meaning the low EPS estimates might have more to commend them.

Wall Street not so positive on Tesla

The cited earnings estimates have actually slipped by two cents over the past week, further supporting the idea that sentiment ahead of the report is turning bearish. Likewise, Tesla trades at roughly 370 times forward earnings, a number far exceeding the average automaker.

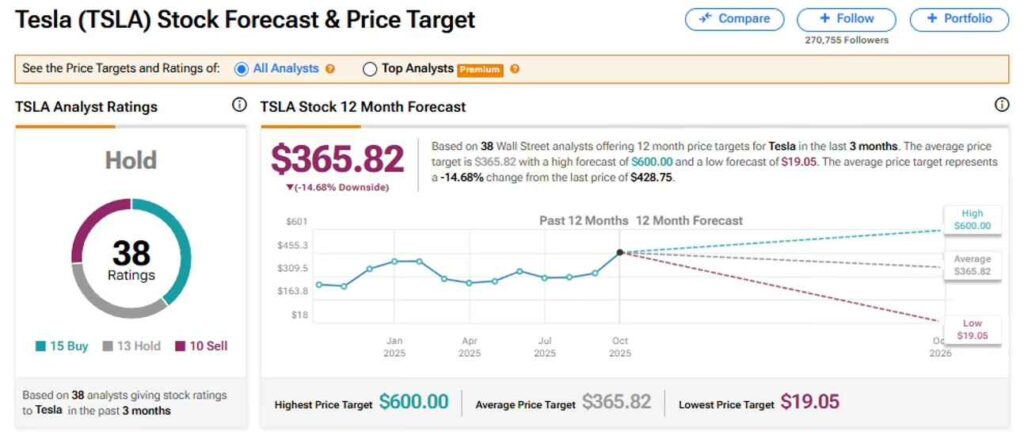

Accordingly, Wall Street is mixed on the electric vehicle (EV) leader. The 38 analysts that track it project an average Tesla stock price target of $365.28 for the next 12 months, indicating a -14.68% downside from the current levels, as per the market research platform TipRanks.

The Tesla price predictions span a wide range, some putting the figure as low as $19.05 and some as high as $600. Similarly, of all the aggregated ratings, 15 consider it a “Buy,” while 13 rate it a “Hold,” and the remaining 10 a “Sell.”

Ultimately, Tesla’s short-term performance will hinge on the quality of its Q3 earnings next week, while its long-term success appears to depend on a more complex set of parameters, the most important of which are likely to be the company’s very business model and the future state of the EV market.

Featured image via Shutterstock