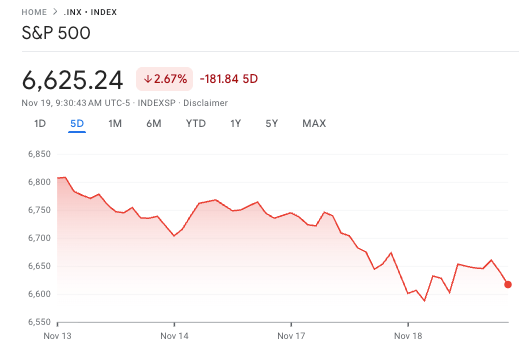

As the S&P 500 faces renewed bearish pressure, Yardeni Research has reaffirmed its expectation that the index is likely to reach a new record high by the end of 2025.

In line with this, the firm reiterated a 7,000 target for the benchmark this year, although it has raised concerns over increasing market risks. Such a target implies a 5.7% increase from the index’s 6,617 close on Tuesday.

The research firm, which had initially anticipated a “melt-up” scenario for the broader market, has now lowered the probability of such a rally, reducing it from 25% to 15%.

Instead, Yardeni has raised the odds of a bearish scenario to 30%, citing growing concerns about an AI-led market correction, weak consumer sentiment, and potential cracks in credit markets.

Despite these challenges, Yardeni Research remains optimistic about the S&P 500’s long-term prospects, arguing that fears of an “AI bubble” could be overblown, much like previous anxieties over a recession that never materialized.

The firm noted that extreme market fear often signals rebounds, supported by strong retail and Redbook sales.

Despite the S&P 500 and Nasdaq falling below their 50-day averages and retreating 4% and 6.4% from October highs, Yardeni maintained its year-end S&P 500 forecast of 7,000, with a 2026 target of 7,700.

Wall Street bullish on S&P 500

Overall, Wall Street analysts are increasingly optimistic on the S&P 500 for 2025, forecasting moderate to strong gains.

For instance, Citigroup raised its target to 6,600, citing robust corporate earnings and fiscal stimulus, with a bullish scenario reaching 7,200. Deutsche Bank lifted its target to 7,000 on expectations of continued earnings growth and supportive monetary policy.

Meanwhile, Goldman Sachs anticipates 7% earnings growth, supported by slight forward P/E expansion, while Edward Jones expects 11% growth but warns that valuations at 23x forward P/E could spur volatility.

Overall, the index is impacted by mega-cap technology performance, AI productivity gains, and favorable tax and spending policies are key tailwinds, though elevated valuations, margin pressures, and macroeconomic uncertainties remain risks.

Featured image via Shutterstock