Warren Buffett’s Berkshire Hathaway (NYSE: BRK.A, BRK.B) attracted significant attention earlier in 2024 for its aggressive stock selling, which included trimming sizable holdings in Bank of America (NYSE: BAC) and Apple (NASDAQ: AAPL).

Recently, however, the legendary ‘Oracle of Omaha’ has shifted gears, making notable purchases that have once again captured headlines. Among these is a recent $28 million investment in shares of VeriSign Inc. (NASDAQ: VRSN), as revealed in SEC filings.

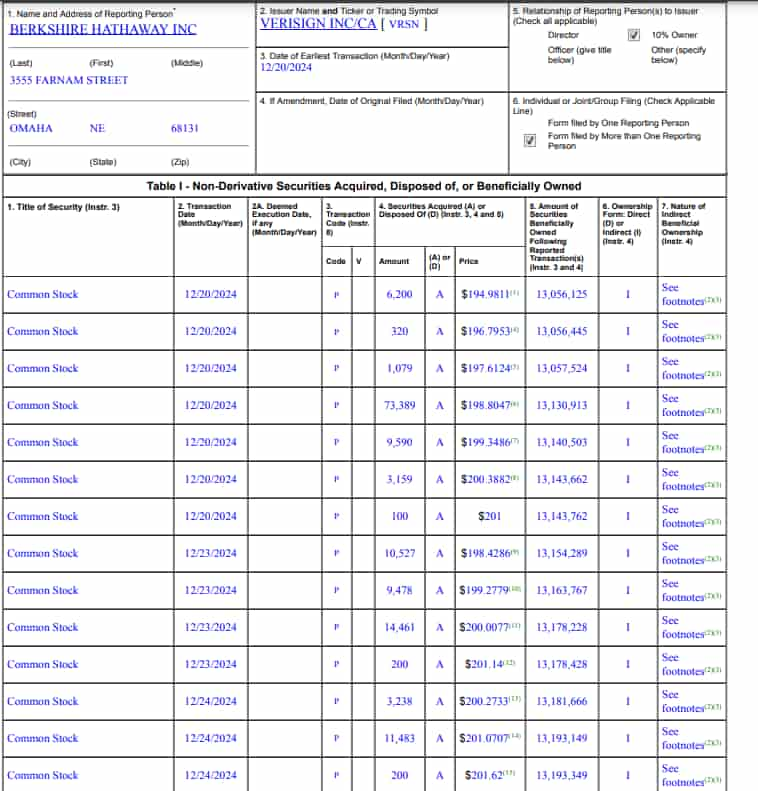

According to the filings, Berkshire purchased 139,930 shares of VeriSign between December 20 and December 24, 2024, at prices ranging from $194.94 to $201.62 per share.

These purchases bring Berkshire’s total holding in the company to approximately 13.2 million shares.

A decade-long relationship with VeriSign

Berkshire Hathaway first took a position in VeriSign during Q4 2012, acquiring 3.69 million shares at an average price of $41.62.

According to data from Stockcircle, the company steadily increased its stake through mid-2014, including a notable addition of 1.13 million shares in Q2 2014.

However, after trimming its holdings slightly in early 2020, the company had not made any further purchases—until this month.

On December 20, 2024, Berkshire Hathaway added 145,000 shares at an average price of $188.82, signaling renewed confidence in VeriSign’s strong fundamentals and long-term growth potential.

Why VeriSign fits Buffett’s strategy

The recent addition aligns with Warren Buffett’s value-investing philosophy, which prioritizes businesses with enduring competitive advantages and predictable revenue streams.

VeriSign, a leader in domain registry services, manages the .com and .net domains under long-term contracts that extend through 2030 and 2029, respectively.

The company has consistently renewed these contracts since acquiring the rights in 2000, ensuring uninterrupted operations and a stable revenue stream.

Financial performance and market dynamics

The company’s financials further support its appeal. In Q3 2024, VeriSign posted a 3.8% year-over-year revenue growth to $390.6 million, while net income rose to $201 million, with earnings per share (EPS) increasing from $1.83 to $2.07. Operating income also improved, rising to $269 million from $254 million a year earlier.

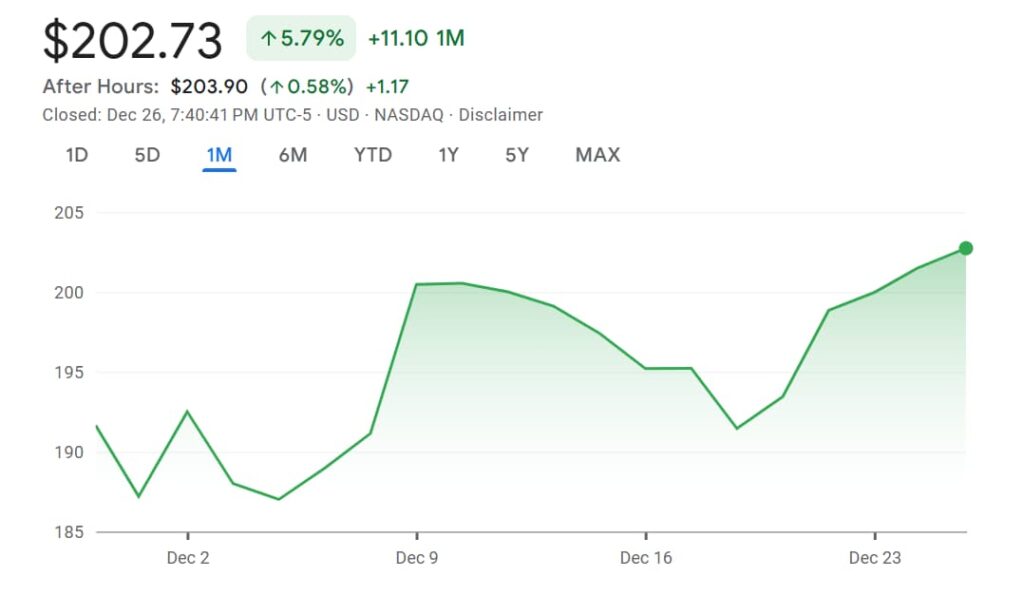

VeriSign’s stock has also outperformed the broader market, gaining 5.79% over the past month compared to the S&P 500 Index’s (SPX) modest 0.42% rise.

At press time, the stock is trading at $202.73, reflecting a 6% gain over the past week. Over the last six months, it has risen 13%, highlighting its strong momentum.

Despite this performance, the stock remains 4% below its 52-week high of $212, suggesting potential for further growth.

Long-term potential

VeriSign’s valuation metrics further highlight its appeal as a solid investment for traders seeking a balance between stability and growth.

With a trailing P/E ratio of 23.56 and a forward P/E ratio of 24.11, retrieved from StockAnalysis, the stock appears reasonably priced relative to its earnings.

This is particularly evident given VeriSign’s consistent profitability and predictable revenue streams, backed by its long-term contracts.

For those navigating uncertain markets, Warren Buffett’s renewed interest in VeriSign serves as a clear signal of its potential, reaffirming the value of aligning with proven investment strategies.

Featured image via Shutterstock