Microsoft’s (NASDAQ: MSFT) rough start to 2026 may be easing as seasonality performance suggests the equity is on the verge of turning around heading into March.

In this context, seasonal trends suggest the coming weeks could offer a favorable window for investors considering Microsoft shares, with historical data indicating strong performance in March and April.

As of press time, MSFT stock was trading at $400, having plunged more than 17% year to date.

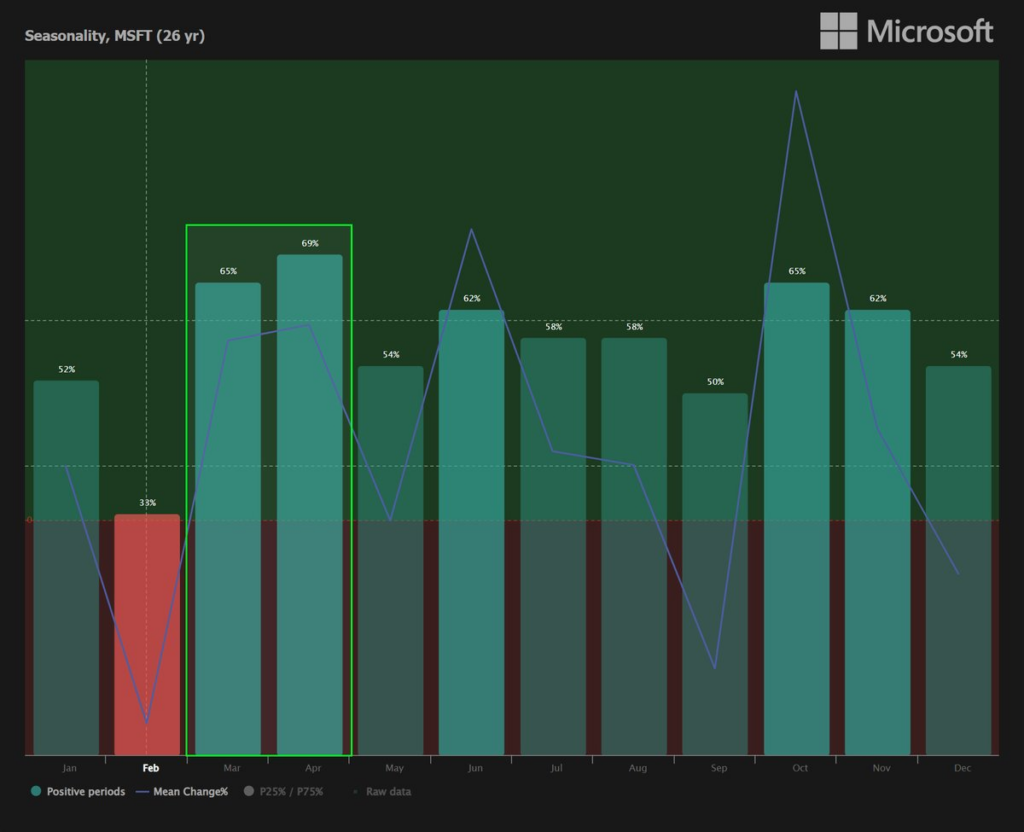

Now, the 26-year seasonality chart tracking Microsoft’s monthly performance shows that March and April consistently rank among the company’s strongest months.

According to insights from charting platform TrendSpider, March has delivered gains 65% of the time, with an average return of 2.1%, while April has posted an even higher 69% win rate and an average gain of 2.3%. The data places both months well above the 50% threshold that typically separates bullish from neutral seasonality trends.

Notably, February tends to be weaker, recording just a 33% positive rate. That softer performance has often been followed by a rebound into March and sustained strength through April, reinforcing the idea of a seasonal shift in momentum as the second quarter approaches.

Beyond the win rates, the mean change line rises into March and remains elevated through April.

Wall Street bullish on MSFT stock

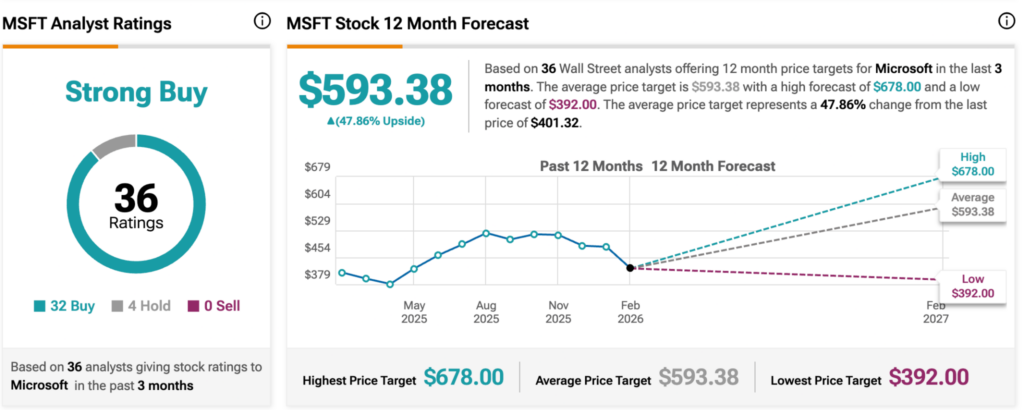

This outlook is supported by bullish sentiment from a segment of Wall Street analysts. On TipRanks, Microsoft holds a ‘Strong Buy’ consensus based on 36 recent reviews. The 12-month average price target stands at $593.38, implying potential upside of 47.86%.

Of the 36 analysts, 32 recommend buying, four suggest holding, and none advise selling. The highest target is $678, while the lowest forecast is $392.

Overall, Microsoft has faced headwinds in early 2026, with the stock pulling back after reaching all-time highs between $541 and $555 in October 2025. The correction reflects investor concerns over heavy AI-related capital spending and signs of moderating cloud growth.

Still, fiscal second-quarter results released in late January were strong, where revenue rose 17% year over year to $81.3 billion, while adjusted earnings per share came in at $4.14, beating expectations.

The Microsoft Cloud segment surpassed $50 billion in quarterly revenue for the first time, growing 26%, with Azure up 39% (38% in constant currency). Guidance suggested Azure growth could stabilize at 37%–38% in constant currency, a moderation from prior peaks that contributed to post-earnings volatility.

Despite short-term concerns around AI spending returns, cloud competition, and potential disruption to legacy products such as Office, Microsoft’s entrenched enterprise position and expanding AI integration continue to underpin a bullish long-term outlook for many investors.