The intersection of politics and stock market trading has become both a controversial and popular subject as of late.

Most of the discourse on the topic concerns the unfair advantage that lawmakers have when it comes to investing in financial markets. Beyond a general informational edge and the ability to legislate, committee assignments provide representatives and senators with an even more nuanced overview of specific sectors.

On the flip side, large publicly traded companies with an excess of money at their disposal also frequently engage in lobbying. While this is purportedly a benign phenomenon that provides industry insights to lawmakers, it also has a habit of inducing corporate capture, legislation favorable to specific enterprises, or the allocation of government funds on a less-than-transparent basis.

To use the most straightforward example (although it hasn’t necessarily panned out as planned), Elon Musk’s funding of the Trump campaign has earned Tesla (NASDAQ: TSLA) a White House endorsement, as well as a comment from the President threatening to label those currently boycotting the company as domestic terrorists.

That’s a very specific example — but does lobbying correlate with higher returns? One market intelligence company thought that the idea was worth investigating — here’s what they found.

Focusing on lobbying stocks would have netted superior returns

So, what would taking an equal-weighted long position in the 10 publicly-traded companies that reported the highest lobbying spend growth on a quarterly basis, rebalanced monthly, provide in terms of results?

The answer is quite simple, thanks to one of market intelligence platform Quiver Quantitative’s automated trading bots. Since the start of the year, this strategy would have accrued a -1.53% loss.

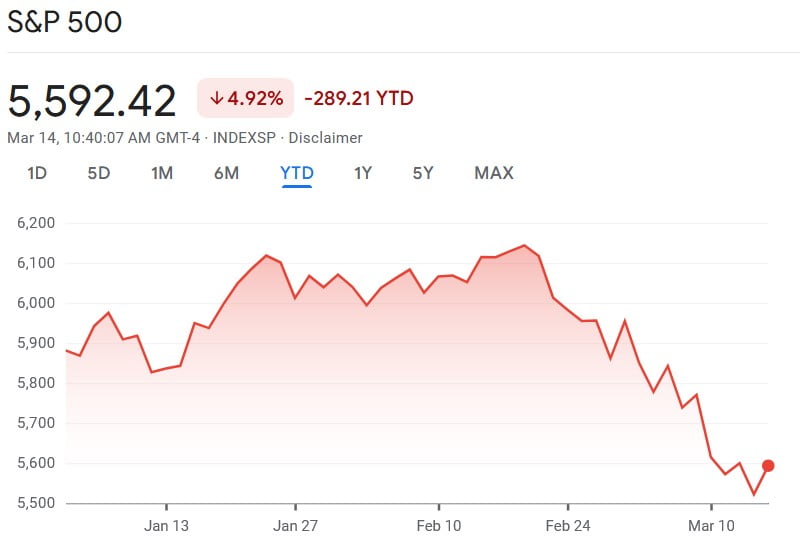

Let’s compare that with the wider market. In the same timeframe, the benchmark S&P 500 index has posted a -4.92% loss.

While the strategy has failed to secure a profit since the start of 2025, this does not imply that a correlation between increased lobbying spending and stock price growth does not exist.

Stepping back to take a look at the bigger picture, applying this strategy and investing in the top lobbying stocks 6 months ago would have provided a 15% return.

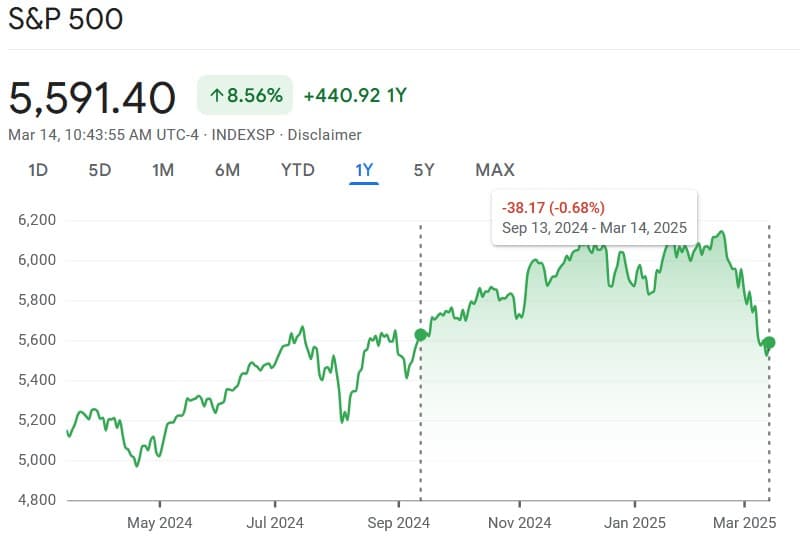

In contrast, an investment in the S&P 500 made on the same day would have accrued a 0.68% loss by press time on March 14. The difference is, to put it very mildly, quite significant.

While past performance is no guarantee of future results, it stands to reason that lobbying stocks are associated with growing businesses that are already doing well and have strong balance sheets, as they can afford to argue for their interests in this manner.

Featured image via Shutterstock