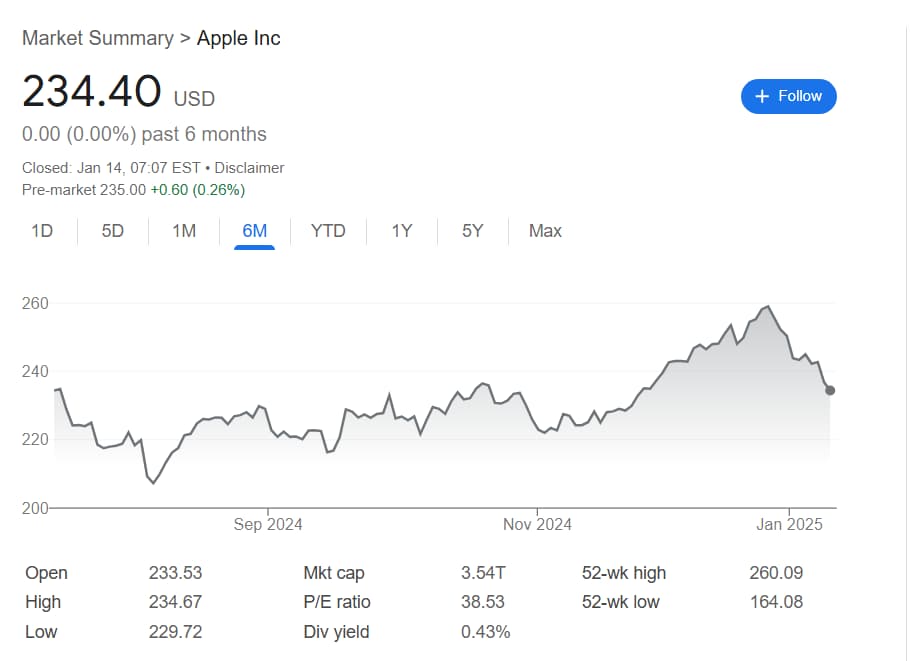

Having annulled the entirety of its price action in the last 6 months and collapsed 9.5% since its December highs, Apple (NASDAQ: AAPL) stock has strayed dangerously close to technical correction territory that might see it plunge as low as $207.

Given the rapid decline, it might come as no surprise that the latest revision of AAPL share price target has been bearish, with KeyBanc rating the technology giant as ‘underweight’ – ‘sell’ – on January 14.

Though it acknowledged year-over-year (YoY) improvements in some areas, such as Indexed Spending, KeyBanc’ Brandon Nispel identified four critical areas in which headwinds prevail.

Why KeyBanc estimates Apple stock price crash is in the cards

The first of these is the lack of a strong upgrade cycle after the release of the iPhone 16 and the associated Apple Intelligence – the company’s artificial intelligence (AI) – rollout.

Multiple analysts, including Wedbush’s Dan Ives, perhaps being the most notable, previously talked about the likely strong impact of the new product when forecasting exceptional growth for Apple.

Ives, for example, interpreted the significant number of iPhone users who haven’t upgraded their device in years as a particularly bullish factor, though already ahead of the September release, some were pointing out that the lack of cyclical electronics buying may have emerged from inflationary pressure consumers have not yet entirely absorbed.

Whatever the reasons behind the lackluster upgrade, the other limiting factor identified by KeyBanc also pertains to the iPhone 16: Indonesia’s ban on the sale of the smartphone model.

Indeed, due to failing to meet the country’s 35% domestic production requirement and despite agreeing to construct a plant in the archipelago nation, Apple is, by press time, bereft of access to the world’s fourth most-populous country.

Why AAPL shares are likely overvalued

Finally, KeyBanc estimated that the data from China demonstrates a modest negative gain with continuously strong competition and that FX is also likely to translate into headwinds. Generally, the strengthening of a currency reduces export competitiveness, and the U.S. dollar has been gaining against nearly all other currencies.

The four factors, per the analyst report, indicate that Apple is suffering from a mix of overly optimistic expectations, the low likelihood of a growth inflection across regions and products, and a valuation that isn’t justified by the technology giant’s fundamentals.

No bearish consensus on Wall Street for Apple stock

Despite KeyBanc’s scathing analysis, the bearishness is far from universal among Wall Street experts. Out of the six revisions in January, Apple received two ‘sell’ ratings, one ‘neutral,’ and three ‘buy’ ratings.

Specifically, JPMorgan (NYSE: JPM) retained its bullish outlook, while Argus raised its price target from $250 to $280 and Bernstein from $240 to $260.

Meanwhile, UBS confirmed it is ‘neutral’ about the big tech firm, and Moffett Nathanson decided to downgrade its outlook for AAPL shares from ‘neutral’ to ‘sell.’

Featured image via Shutterstock