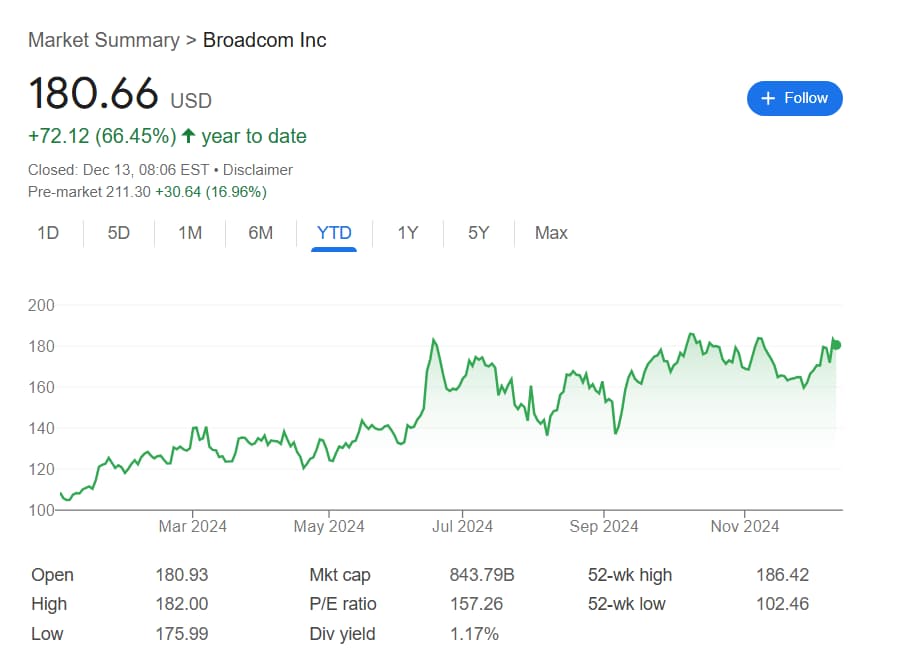

Despite trading with significant volatility throughout the year, Broadcom (NASDAQ: AVGO) stock has been, without doubt, a strong performer in 2024.

Indeed, year-to-date (YTD), AVGO shares are so far 66.45% in the green.

Still, the biggest Broadcom news in recent weeks has been the company’s fourth-quarter (Q4) earnings report, published on December 12, as it enabled the stock to surge 16.96% in the Friday pre-market, from the latest closing price of $180.66 to the press time price of $211.30.

Wall Street analysts weren’t unaffected by the report either, and on the morning of December 13, a variable deluge of overwhelmingly positive price target revisions started coming in.

Analysts set Broadcom stock price target after earnings

Out of the 20 reassessments unveiled by press time, some of the standouts include Morgan Stanley’s (NYSE: MS) price target increase from $180 to $233, JPMorgan’s (NYSE: JPM) from $210 to $250, KeyBanc’s from $210 to $260, and Evercore ISI’s from $201 to $250.

HSBC’s revision was likewise interesting as it is one of the few that came out after the report to rank AVGO as ‘hold.’ As could be expected, the change in the accompanying price prediction was likewise conservative – if positive – as the forecast increased from $160 to $175.

The comments provided by UBS and Raymond James also offer some insight into the experts’ bullishness. Indeed, both institutions commented positively on Broadcom’s results – particularly noting they were better than many feared ahead of the print – but both focused extensively on artificial intelligence (AI)-related aspects.

Specifically, AI XPUs and Ethernet networking portfolio were noted as particularly strong during the quarter and, per UBS’ Timothy Arcuri and Raymond James’ Srini Pajjuri, are likely to lead to significant expansion for Broadcom’s AI SAM in the coming years.

Furthermore, Broadcom is expected to extensively benefit from its two current hyperscale customers – OpenAI and Apple (NASDAQ: AAPL) – and see further tailwinds from the 2027 hyperscale customers – rumored to be Google (NASDAQ: GOOGL), Meta (NASDAQ: META), and ByteDance.

Despite the positivity, UBS maintained the ‘buy’ rating, with Arcury raising the price target from $200 to $220, but Pajjuri stuck to the ‘neutral’ rating.

How strong was Broadcom’s latest earnings report?

The cause for the hints of bearishness at worst, and caution for certain can be found in the report itself. Though the AI growth was widely lauded for its strength, it is worth pointing out that Broadcom’s revenue came at $14.05 billion, below the expected $14.09 billion.

Similarly, more traditional elements of the giant’s business, such as semiconductors, remain well below their historic highs, and the outlook for the ASIC business for the first half of 2025 remains flat.