Following a slow beginning to the year, the entire electric vehicle sector, including major players like Lucid (NASDAQ: LCID), faced setbacks resulting in significant drops in their stock values.

While the year started challenging, the past month proved even more difficult for LCID stock, experiencing a staggering decline of -26.63% in value.

However, there are signs that the situation is improving, offering a glimmer of hope and raising the possibility of this stock returning to a valuation above $3.

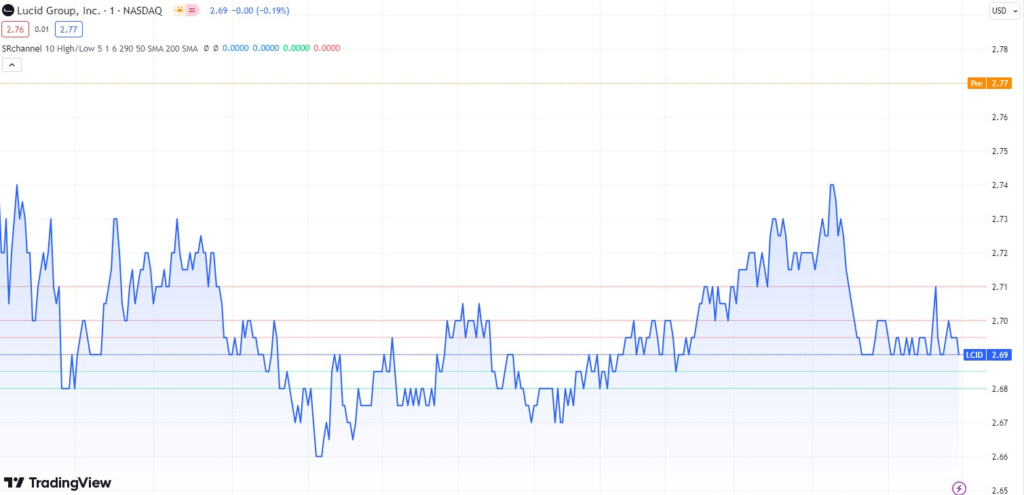

LCID stock price chart

As of the latest closing on March 15, LCID stock was trading at $2.70, reflecting a gain of 2.66% from the previous closing price. Additionally, there was an extra gain of 1.85% in pre-market trading.

Looking at the support and resistance levels for LCID stock, a support zone exists between $2.62 and $2.64, formed by multiple trend lines across various time frames.

In terms of resistance, notable areas include a zone from $2.91 to $2.93 and another from $3.04 to $3.08, both formed by intersecting trend lines across different time frames.

Pro reasons for LCID stock

For Lucid Motors to possibly recover and thrive, investors should focus on two key factors.

Firstly, it benefits from substantial backing from the Saudi Arabian Public Investment Fund. This financial support is likely to remain crucial as it introduces its second electric vehicle model.

Moreover, Lucid recently unveiled its latest product, the Gravity SUV, to boost sales and delve into the untapped realm of electric vehicles. This move could position Lucid Motors as a frontrunner in this segment of the industry.

It appears that the newest offering is already making a positive impact on sales, with Lucid experiencing a 32.5% increase in sales in February 2024 compared to the same month last year in the US, selling an estimated 603 units. This brings Lucid’s total sales for January and February 2024 in the US to 1,042 units, marking a 22.9% increase over the same period in 2023.

On March 15, Lucid Motors revealed its partnership with NeueHouse, in an attempt to diversify its portfolio of collaborations, and possibly provide an innovative approach to the EV industry, seeking collaborations that may seem unusual at first, but might prove to be beneficial in the long run.

Many reasons to be worried about

However, there is still a growing list of worrying factors with Lucid Group’s vehicle production remaining modest, hinting at a limited delivery volume (just 6,001 units in all of 2023).

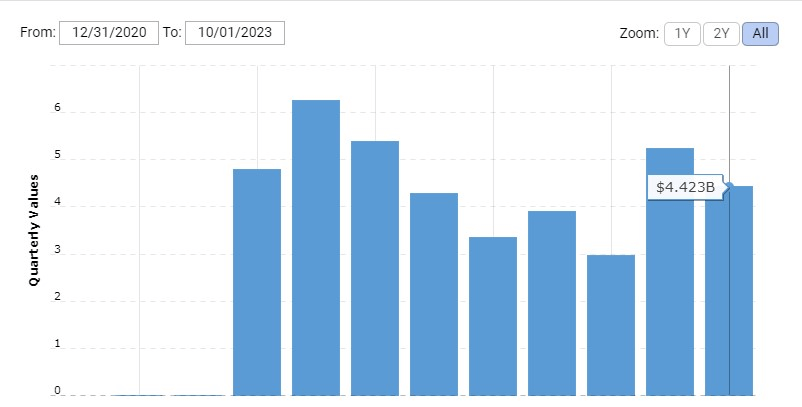

CEO Peter Rawlinson openly acknowledged the company’s significant cash burn rate, estimated at around $1 billion per quarter, indicating a precarious cash position. With only $4.42 billion in cash reserves at the end of last year, Lucid may soon need to seek additional capital. Rawlinson’s acknowledgment of the inevitable need for future fundraising underscores this necessity.

Interestingly, Lucid Group’s Arizona factory can manufacture 90,000 vehicles annually, a striking contrast to the anticipated production of only about 9,000 EVs in 2024. This glaring disparity suggests potential financial strain.

Considering these circumstances, it wouldn’t be surprising if Lucid Group sought significant borrowing soon, although this would entail repayment with high interest rates prevailing.

Alternatively, the company might resort to issuing new stock shares to raise capital, potentially diluting the value of existing shares, and leading to LCID stock being devalued further.

Conclusion

Although promising aspects are suggesting that LCID stock could exceed the $3 mark in the short term, the future outlook appears bleak.

Factors such as decreasing production rates, which fall well below capacity, declining cash flow, and the potential need for high-interest loans paint a discouraging picture for Lucid’s prospects.

Buy stocks now with eToro – trusted and advanced investment platform

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.