Investing can be intimidating, especially when you are new to it. After all, it doesn’t come without risk. The good news is that plenty of different techniques are available, suitable for all investor types and risk tolerance, ranging from low-risk investments to high-risk, high-reward strategies for more seasoned investors.

But, as with everything in life, investing requires dedication and hard work. Therefore, a thorough understanding of investing and different investing strategies is crucial to achieving your financial goals. In this investing guide for beginners, you’ll understand why starting investing now can be a great idea and how to make your savings work for you.

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.

What is investing?

Anyone who has some money saved can invest but should have a thorough understanding beforehand. Deciding your investment strategy depends on how much money you can invest and the level of risk you are willing to take.

An investor isn’t always someone rich with unlimited capital like Warren Buffet or the founder of Amazon (NASDAQ: AMZN), Jeff Bezos. That is far from the truth; in reality, anyone with savings can start investing in their preferred and suitable areas.

Investments can be generally categorized as:

- Growth investments: usually in high-growth options like stocks with the expectation that they will generate above-average returns; however, they can be more short-term, come with greater risk, and require more consistent attention, analysis, and work.

- Defensive investments: generally in asset classes where profits can provide a lower, however consistent, return. For example, bonds are more stable, less risky, and generate a fixed income. It also entails buying mature and stable blue-chip stocks.

However, the growth and profits aren’t guaranteed and can always end with a loss, making investing, especially in stocks, risky. But there are several other low-risk options besides stocks that can make a good return over time for more risk-averse people, as well as using diversification to manage these risks.

For example, Ray Dalio, a billionaire investor and the founder of Bridgewater Associates, the world’s largest hedge fund, has called diversification his most important investing principle, learned throughout his career, especially for managing investment risks.

In the broader sense, investing in education can be investing, or expenses to solve a particular challenge can be an investment. It can also be about investing in commodities, such as gold, art, antiques, or other collectibles, where value can go up over time.

People can take a direct “do-it-yourself” approach using a mix of fundamental and technical analysis, invest in mutual funds, or use professional investment services.

Recommended video: How to invest for beginners.

Investing for Beginners:

- 17 Common Investing Mistakes to Avoid

- 15 Top-Rated Investment Books of All Time

- How to Buy Stocks? Complete Beginner’s Guide

- 10 Best Stock Trading Books for Beginners

- 15 Highest-Rated Crypto Books for Beginners

- 6 Basic Rules of Investing

- Dividend Investing for Beginners

- Top 6 Real Estate Investing Books for Beginners

- 5 Passive Income Investment Ideas

- How to invest $100, $5k, $10k, $20k or even $200k

Active vs passive investing

Investors can either actively invest and manage their own investments and generate techniques hoping for above-average gains, which requires attention, market analysis, and work.

Conversely, some may opt for passive investing in fixed-income bonds to generate more long-term passive income but require less constant attention.

One of the reasons for investing is simply making more money with existing money; the aim is to earn profits. Another reason for passive investing is that money and savings can lose value over time due to inflation.

With the inflation calculator, you can check how much your savings are worth in a few years. For instance, with an assumed 3% inflation rate for an item that costs you $50 today, this same item will cost $67.20 in ten years, or for instance, if you have $10,000 in savings, these savings would then be reduced to around $7,440 in ten years.

Keeping money in a savings account is often not enough, as it won’t outgrow inflation. For example, in 2021 the U.S. inflation rate was at 6.8%; in contrast, the average interest rate of a savings account in the U.S. was at a mere 0.06%.

How to start investing?

Even though everyone could and should invest, investing comes with a high risk, and assets are not guaranteed to increase or hold value over time. Sometimes people can earn significant dividends if the economic situation is good but lose money when investments drop in value during an economic downturn or recession. Before starting investing, thorough research is crucial.

For example, several assets would go up in value during a bull market, whereas they often decrease along with the contracting economy during a bear market. However, this is dependent on the asset and industry you have invested in.

A risk-averse person who wants to make their savings grow without it being affected by inflation might consider investing in bonds or real estate. In contrast, someone with high-risk tolerance may prefer investing in stocks. Historically, stocks have yielded higher returns than Certificates of Deposits (CDs), bonds, or other low-risk investment products.

Where to invest depends on three things:

- Budget;

- Investing goals;

- Your risk tolerance.

What is more, you should consider the risk and return.

Risk and return correlation

The two most common investing strategies – active and passive investing – are driven by risk and return, each having its pluses and minuses.

To fully understand the benefits and downsides of each and which investment style fits your budget and risk tolerance best, let’s go through the correlation of risk and return so you can decide which is the right choice for you.

- Risk – you are a risk-averse person who may fear losing money.

- Returns – you are chasing those high-risk, high-return, short-term gains.

A risk-return tradeoff is an investment principle, and they go hand-in-hand in investing. Low risk generally means lower returns and profits gained over a more extended period, whereas high risk means higher returns.

Low-risk investing includes things like Certificates of Deposit (CDs) or bonds (for example, Treasury Inflation-Protected Security (TIPS), Treasury Bills, or Treasury Notes). At the same time, assets like stocks are considered riskier investments.

However, it is essential to note that even stocks can have different risk and return expectations and vary widely within the same asset class. For example, large-cap or blue-chip stocks, such as Microsoft Corporation (NASDAQ: MSFT) or Apple Inc. (NASDAQ: AAPL), can have a very contrasting risk-return profile than a small-cap stock trading on a smaller exchange.

Types of investments: different asset classes

There are several types of investments people can opt for, from stocks, cryptocurrency, or bonds to more practical things like art, collectibles, or real estate. However, there are three main types of investments, all of which you can invest directly (you manage your assets yourself) or indirectly (through mutual funds).

Historically, these three main asset classes are stocks (equities), bonds (fixed-income), and cash equivalents (savings accounts, money market funds). However, investing options can also include real estate, commodities, cryptocurrencies, or other financial derivatives that could be added to the asset class mix. The mix is a wide one, with some riskier than others.

Let’s go through every one of them to get a good overview of what they are and their risk and return correlation.

Stocks

When talking about investing, stocks are often the first thing that comes to mind. Investing in stocks and shares is a high-risk, high-return investment strategy. Companies go public and sell their stocks or shares to fund their business operations further, whether for expansion or new business ventures or simply profit from their success.

However, stocks carry a high risk, one of the highest out of all the investment types, but if approached in a sensible and disciplined manner, it is also one of the most rewarding ways to build up personal finances.

Tip

Because stocks are affected by the overall economic situation and market sentiment, companies can go out of business at any time, and the returns aren’t always guaranteed. For example, when investor confidence is high during bull markets, people buy and sell more stocks, driving up stock prices and vice versa.

Stocks can be classified based on market capitalization, which is the total shareholding of a company. It is calculated by multiplying the current price of the company stock with the total number of shares outstanding in the market.

Here’re are the key types of stocks based on market capitalization:

- Large-cap stocks or blue-chip stocks are big enterprises with a market capitalization of $10 billion or more. They are generally less volatile throughout economic downturns, making them a more stable and risk-averse investment. Some examples include Goldman Sachs (NYSE: GS), Alphabet Inc. (NASDAQ: GOOGL), BioNTech SE (NASDAQ: BNTX).

- Mid-cap stocks are companies with a market value between $2 billion and $10 billion; they are helpful to include in the portfolio for diversification. They tend to offer a good balance between growth and stability.

- Small-cap stocks are smaller companies with fewer publicly-traded shares than large or mid-cap stocks, somewhere between $300 million and $2 billion in outstanding shares. They are a riskier investment due to lack of resources; however, they can offer a higher return on investment in the long run.

- Penny stocks are companies trading for less than $5 per share, and even though some of them do trade on large stock exchanges such as the New York Stock Exchange (NYSE), most of them are over-the-counter (OTC) transactions.

- What is more, in terms of ownership, stocks can be classified as common stocks, where shareholders get voting rights and have a percentage of actual ownership, and preferred stocks, where dividends are paid out but holders have no voting rights.

Best Crypto Exchange for Intermediate Traders and Investors

-

Invest in cryptocurrencies and 3,000+ other assets including stocks and precious metals.

-

0% commission on stocks - buy in bulk or just a fraction from as little as $10. Other fees apply. For more information, visit etoro.com/trading/fees.

-

Copy top-performing traders in real time, automatically.

-

eToro USA is registered with FINRA for securities trading.

Bonds

In simple terms, a bond is a contract between two entities – corporations or governments issue bonds because they need money to borrow large sums of money.

People can then buy these bonds (e.g., give money to these banks and corporations) in exchange for a fixed-income interest. These fixed interest payments, also known as coupons, are usually paid out to investors every six months.

As opposed to stocks, bonds are a low-return, low-risk asset class that investors would use to offset risk. Whereas stocks offer the highest potential in terms of returns, bonds balance the high risk and generate a lower yet more steady income.

Bonds are less vulnerable to market volatility; however, they do come with certain risks such as credit risk, repayment, or interest rate risk. Like stocks, corporate bonds are usually traded on an open market through brokers.

Cash equivalent

The third typical asset class is cash equivalents, which lets you have access to your cash while earning interest to protect your other investments. These are also low-risk, low-return investment options, which also help to avoid losing money to inflation.

Cash equivalent examples include:

- Savings accounts;

- Money market accounts;

- Certificates of deposit (CDs).

These investments usually generate a stable return on investment; however, they aren’t designed for long-term investment goals like retirement or high returns. It is an excellent way to keep your cash available for other investments or not lose money to inflation.

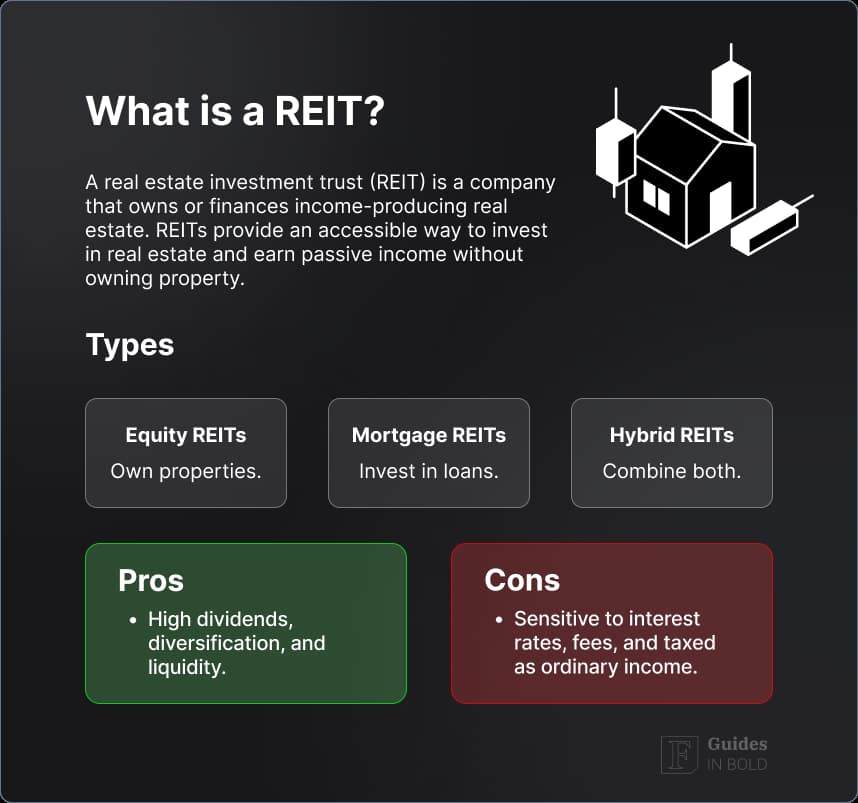

Real estate investing

For people who prefer a steady income and a stable return on investment, real estate investing can be a great idea. When purchasing a home or property, there are several factors to consider, such as the overall economic condition, varying real estate prices in certain areas due to crime rates or school ratings, up-and-coming areas, and rent prices in the area.

Even if you don’t have the total amount together, people looking to invest their savings in real estate can apply for loans to cover the rest. It still makes a good investment; however, be aware to check whether you can also earn a profit after renting it out.

People looking to invest in real estate without buying a property can instead buy shares in the real estate investment trusts (REITs). Like stocks and bonds, REIT stockholders earn income through these investments, which comes either through rent or mortgages of those properties.

REITs offer an excellent and stable return on investment, with above-average dividends and long-term investment; however, they can also be affected by economic downturns and recessions.

Commodities

Commodities include precious metals, gold, oil, grains, animal products, or currencies. Commodities are actual products or raw materials used by different industries, such as manufacturing.

Investors buy them using commodity futures or contracts – an agreement to sell a certain quantity of a particular commodity at a specific price by a certain date – typically for more experienced investors. It isn’t as easy as investing in stocks or bonds.

Prices are highly dependent on the market demand; for example, the Covid-19 pandemic in 2020 caused oil prices to tumble due to restrictions on travel and tourism, increasing supply, making commodities a relatively high-risk investment.

Hedge funds and private equity

Private equity enables businesses to raise capital without going public – previously thought of only for investors who meet a particular net worth requirement. Companies that haven’t or can’t go public can raise funds through private investors. However, this has changed in recent years, and investing in them has become more available.

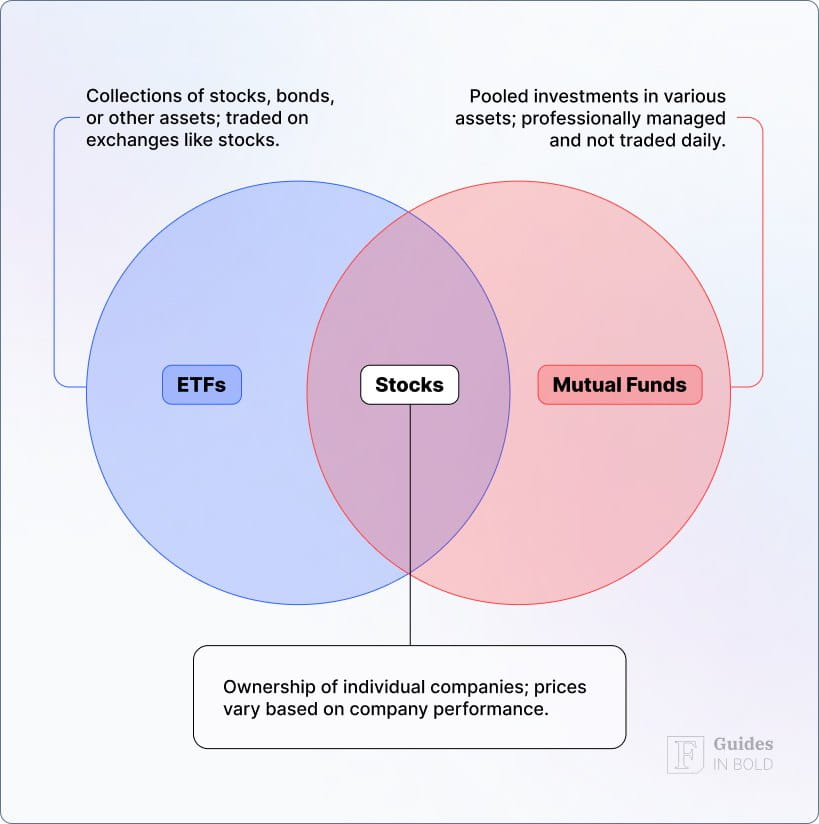

What are mutual funds?

Investing is done either directly or indirectly – you can directly invest in stocks, bonds, or other assets or choose to invest in a mutual fund. A mutual fund can mean both an investment and a company that brings together several different stocks, bonds, or other asset classes and is managed by fund managers.

The key difference is that you do all the work, research, analysis; all your investments are separate; however, you can take complete control and responsibility. You can let the experts do that for you when investing in mutual funds, but you have less say over which ones.

What are exchange-traded funds (ETFs)?

Exchange-traded funds are similar to mutual funds, with the exception that they are bought and sold on stock exchanges, whereas mutual funds are sold from the issuer. Similarly to mutual funds, an ETF can also hold several different assets such as stocks, bonds, commodities, or currencies.

The key benefits and advantages of ETFs are diversification, lower costs, the option to invest in more alternative investments, and it is also more tax efficient.

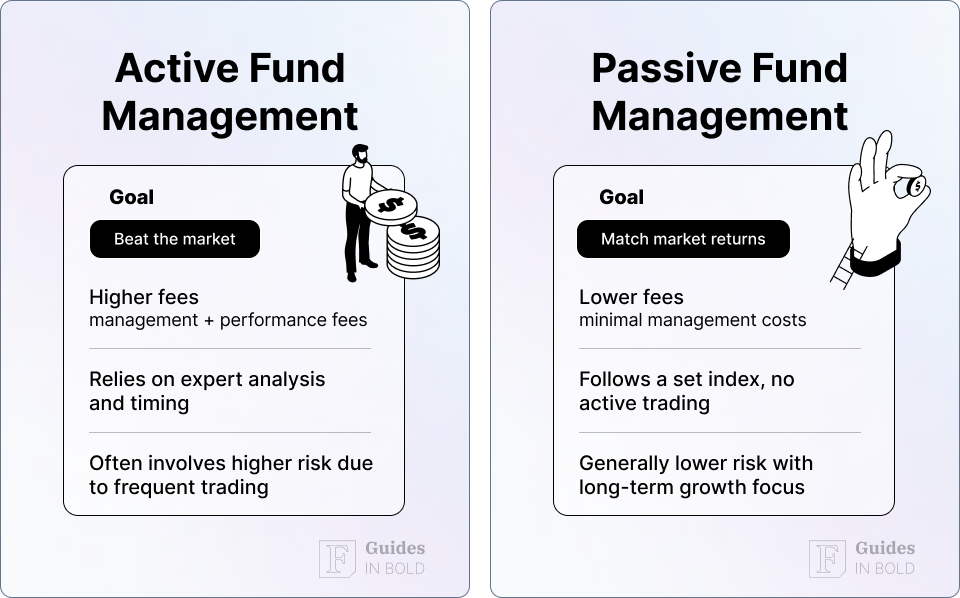

Active vs passive fund management

When investing in mutual funds or ETFs, there are two main management approaches to consider: active and passive. Active fund management involves professional fund managers who actively select and trade investments to outperform a specific benchmark or achieve specific investment goals. This hands-on approach requires thorough research, market analysis, and frequent trading, which can lead to higher management fees.

In contrast, passive fund management aims to replicate the performance of a specific index, such as the S&P 500, by holding a portfolio of assets that mirror the index. This strategy is less intensive, resulting in lower management fees and expenses. While active funds may offer the potential for higher returns, they also carry a higher risk of underperformance. Passive funds, on the other hand, provide consistent exposure to broader markets with lower costs, making them a popular choice for long-term investors.

What is asset allocation?

Perhaps you have already heard the expression that applies very well to investing – don’t put all eggs in one basket. It is essential to diversify your portfolio to offset the risk and not put all of your money into the same asset classes when investing.

Asset allocation is about how you spread your investments across different categories, such as stocks, bonds, or real estate. Asset classes don’t move in sync, which reduces the risk in your portfolio against market volatility. For example, one can offset the risk from investments like stocks by investing a part of the capital in bonds.

Investment strategies

Every investment carries a risk to a certain degree. However, some investment strategies are riskier than others, and some require more focus, research, and work than others. The good thing about investing is that it can be flexible, and you can choose the one that best fits your risk tolerance and expectations.

Think about which fits your possibilities: budget, time, aim, and risk tolerance. There are two different general approaches to investment strategies – active and passive investing.

As the name suggests, active investing is someone willing to take a hands-on approach and track short-term price fluctuations for maximum returns. On the other hand, passive investing is a long-term strategy with a buy-and-hold mentality where wealth is built by buying securities that follow market indexes.

Let’s compare the common four investing strategies:

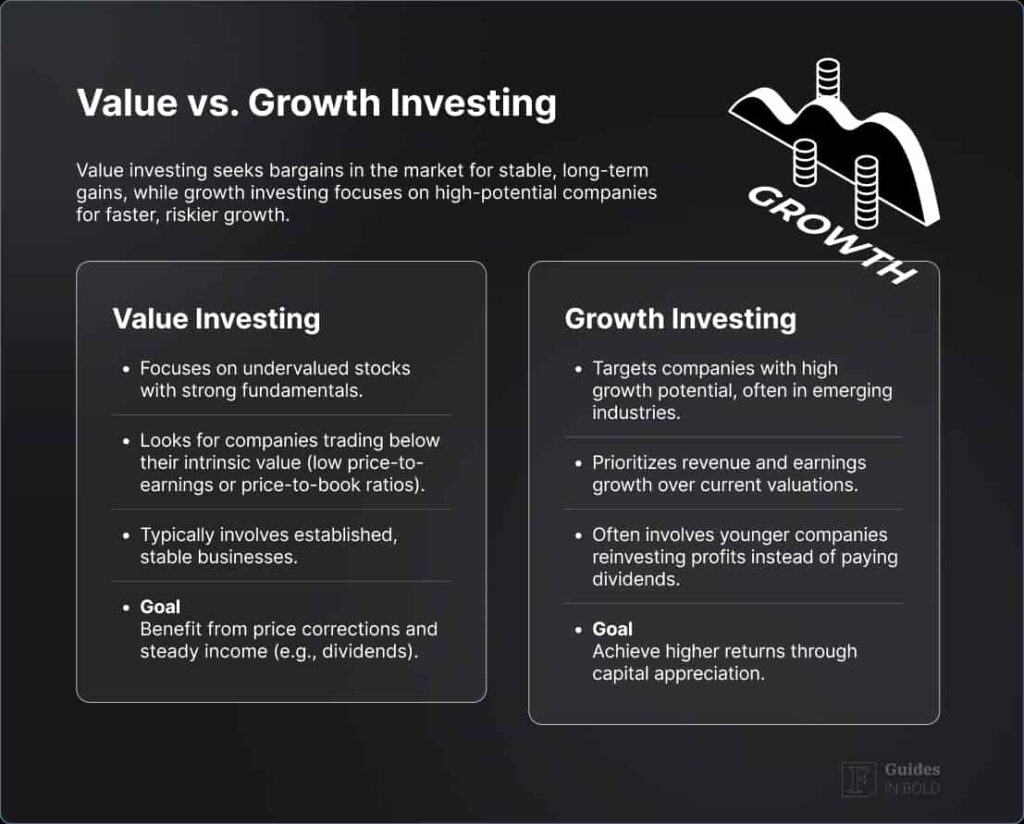

1. Value investing

Value investing is a buy-and-hold strategy that means buying undervalued stocks and holding them for an extended period hoping they will regain value over time. It is about assuming some companies are currently at their low point; however, expect them to gain significant value soon.

Also called intelligent investing, it is a strategy that requires close market analysis and attention to the current events to see which stocks may be undervalued. Often compared to bargain-hunting – getting a pair of boots with an 80% discount.

It is a high-risk investment strategy, and for it to work, one has to commit long-term and ride out the low points.

2. Growth investing

Growth investing is about looking at what could offer the most potential in the future, e.g., what is going to be the next trend. However, it may sound speculative and requires and involves the considerations of the current market happenings and trends, the economic situation, and specific industries stocks are thriving to evaluate their potential to grow.

For example, when internet-based technology companies took over in the 1990s. Or now, one could analyze whether there is a future and further growth ahead for e-commerce before investing in Amazon (NASDAQ: AMZN) or if electric cars will take over in a few years before investing in Tesla (NASDAQ: TSLA).

Growth investors can also assess the potential by looking at the company’s recent financial performance – a growth stock should be continuously growing and have a strong track record for earnings and revenue.

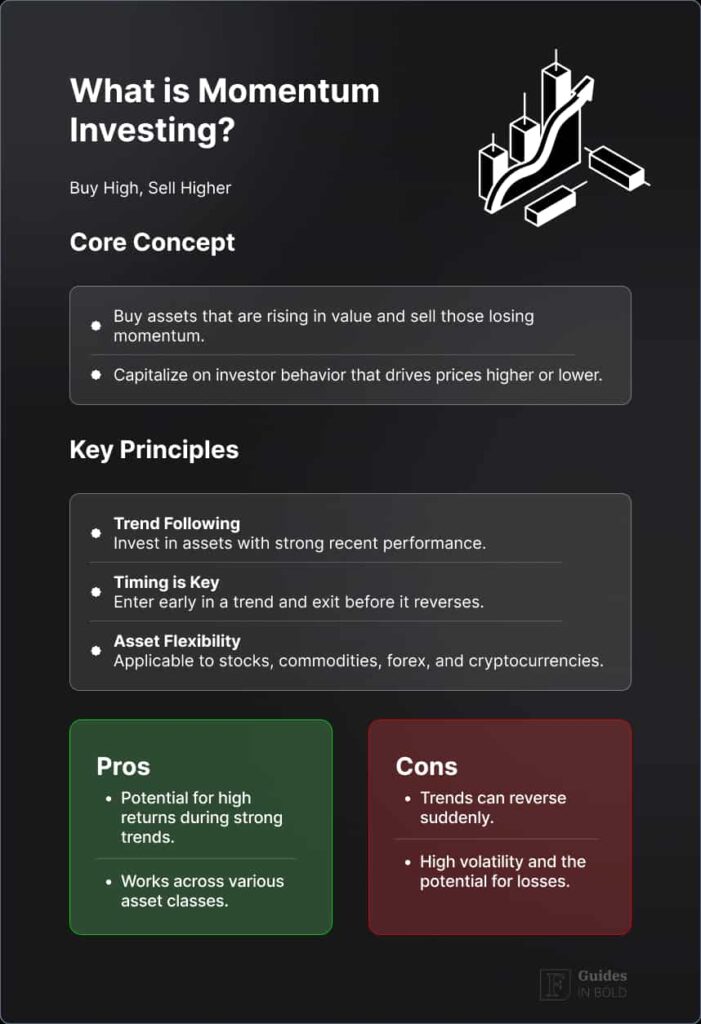

3. Momentum investing

Momentum investing is based on a data-driven approach, looking for signs and patterns that would impact their investment decisions. This strategy seeks to gain profits on both undervalued and overvalued stocks. Investors buy stocks that have performed well in the past and short-sell the ones that performed badly in the past; this strategy can generate high returns over a few months’ holding periods.

Momentum investors use a strictly data-driven approach to trading and look for patterns in stock prices to guide their purchasing decisions, a form of active trading.

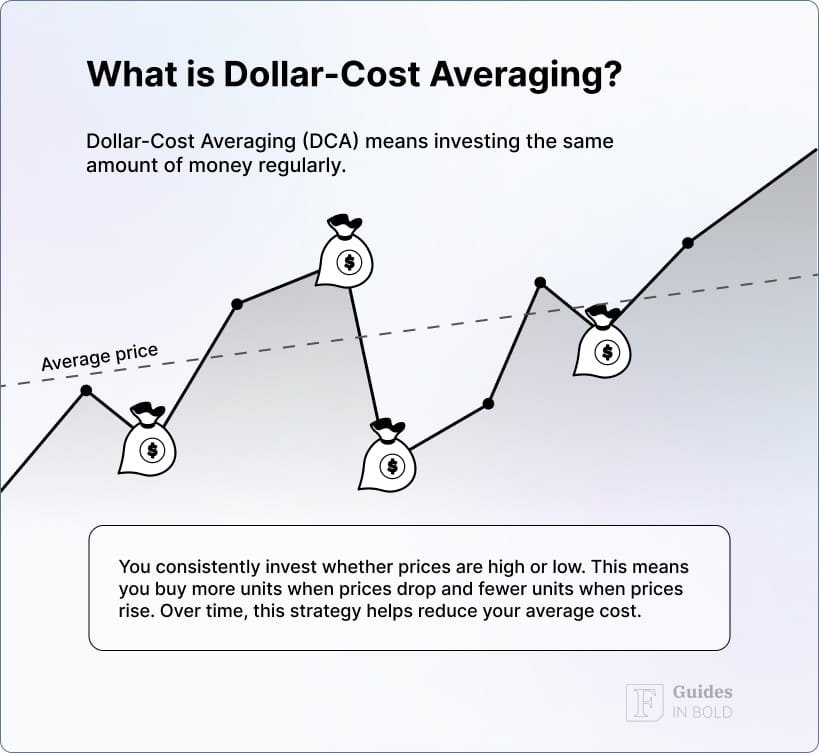

4. Dollar-cost averaging

Dollar-cost averaging (DCA) is another main investment strategy that essentially involves splitting the lump sum of money invested in one company stock into smaller amounts over a period of time.

The main reason for this is to reduce the impact of price volatility so that investments are broken down into lower, but frequent, intervals. These smaller amounts are then invested regularly and it doesn’t matter if the prices go up or down.

How are investments taxed?

It is nice to see your stocks go up in value or receive dividends; however, don’t forget to think that all investments are taxed – that includes common assets like stocks but also crypto tax when investing in cryptocurrencies.

If you want to determine how your investments are taxed for the given tax year, you must first clarify if they generated income. If so, the usual income tax applies, and taxing is considered ordinary. However, if you have sold an investment, it would count as capital gain income and affect the way it is taxed.

Pros and cons of investing in stocks

Pros

- Build wealth

- Earn passive income

- Choose the investments that suit your risk tolerance and budget

- You don’t have to be an expert – you can use professional investment services to invest

- You can start from smaller investments

- Access investments any time

- Inflation-proof your savings

Cons

- No matter the type of investment, all asset classes carry risk to a certain extent

- Many investments come at a very high risk

- You can lose all of your money

- Returns aren’t guaranteed

- It takes time to generate sizeable returns

- Stock market can be extremely volatile and depends on the economic situation

- Investments aren’t recession-proof

In conclusion

Before committing to investing, make sure to do enough reading, consideration, keep up with the current finance news, and do a thorough research. Investing isn’t rocket science, but it does require a thorough understanding of the risks and rewards each investment asset class carries.

You should also ask yourself: what kind of investor am I? Think about what level of risk you are willing to take, whether you are a risk-averse or risk-tolerant person, and how you could realistically invest.

Important

1. Do not invest more than you can afford to lose;

2. Don’t put all your eggs into one basket and make sure to diversify;

3. Plan your trade, and trade your plan.

4. Do not invest in things you don’t understand.

5. Always do your own research (a.k.a. DYOR).

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.

FAQs about investing:

What is investing?

Investing is the act of putting money into assets like stocks, bonds, real estate, or commodities – anything where value can go up over time and generate more money over time. Anyone with some savings can invest; however, should make sure to have a good understanding on how it works beforehand. The growth and profits aren’t guaranteed and can always end with a loss, making investing, especially in stocks, risky. But there are several other low-risk options besides stocks that can make a good return over time for more risk-averse people.

What are the risks of investing?

Investments come with a risk, and assets are not guaranteed to increase or hold value over time. Sometimes people can earn significant dividends if the economic situation is good, but lose money when investments drop in value during an economic downturn or recession.

A risk-averse person who wants to make their savings grow without it being affected by inflation might consider investing in fixed-income bonds or real estate. In contrast, someone with high-risk tolerance may prefer investing in stocks.

What are the 4 types of investments?

There are four main types of investments: stocks (equities), bonds (fixed-income), and cash equivalents (savings accounts, money market funds), and real estate. However, there are several types of asset classes people can invest in: stocks, cryptocurrencies, or bonds, to more practical things like art, collectibles, or real estate.

Investing options can also include other financial derivatives that could be added to the asset class mix, which is a wide one, with some investments riskier than others.

What are common investing strategies?

Every investment carries a risk to a certain degree, but the good thing about investing is that it can be flexible, and you can choose the one that best fits your risk tolerance and expectations: your budget, time, aim, and risk tolerance. There are two different general investment approaches – active and passive investing. Most common investing strategies include value investing, growth investing, momentum investing, dollar-cost averaging, or income investing.

How are investments taxed?

Investments are taxed at different rates – either as income or as capital gains, and ultimately. Moreover, it depends on the type of investment and how long they hold on to the assets. To determine if and how your investments are taxed, first clarify if they generated income; if they did, the usual income tax applies. When you sell an investment, however, it would be taxed differently as capital gains.