While Palantir’s (NASDAQ: PLTR) share price has enjoyed a massive spike, one lingering concern is the company’s ability to sustain this momentum due to the equity’s current high valuation.

Some analysts view the software firm’s venture into artificial intelligence (AI) as a key catalyst for further growth. Nevertheless, there are worries that the stock is already pricing in this potential growth, making it susceptible to a crash if it fails to meet future targets.

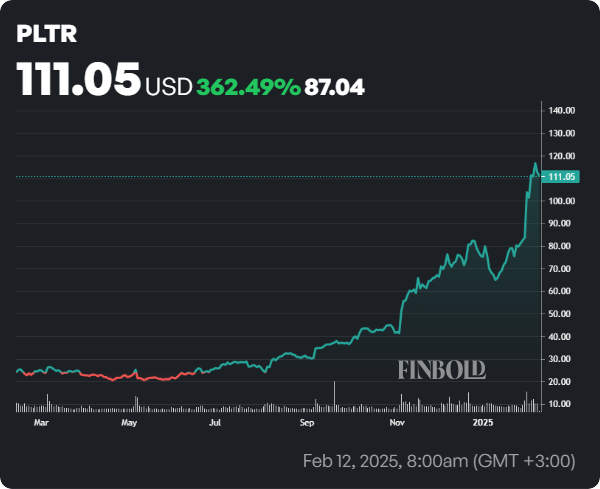

The sustained PLTR stock momentum has seen the equity rally almost 50% year-to-date, ending the last session at $112. Over the past year, the stock is up a staggering 350%.

At the current price, Palantir’s price-to-earnings (P/E) ratio stood at 592 as of February 12, significantly higher than its peers. With such a lofty valuation, the equity is vulnerable to a potential correction.

AI sets PLTR stock crash timeline

In this regard, Finbold turned to OpenAI’s ChatGPT-4o for insights into when the software giant might face a downturn. According to the AI tool, with a high P/E ratio, a sharp drop could be imminent unless Palantir’s earnings growth justifies its premium valuation.

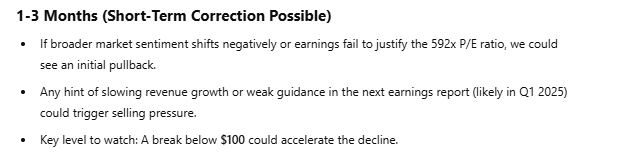

ChatGPT noted that the first signs of weakness could emerge in the next few months. If market sentiment shifts negatively or Palantir’s earnings fail to impress, investors might begin taking profits.

The next earnings report, expected in Q1 2025, will be critical—any hint of slowing revenue growth or weak guidance could trigger selling pressure. A key support level to watch is $100; breaking below this could accelerate the decline within one to three months.

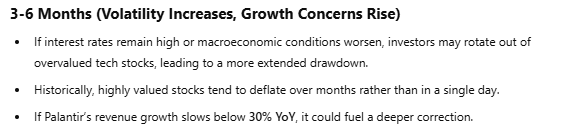

In a second scenario, which might unfold between three to six months, the AI tool suggested that investors may rotate out of high-valuation tech stocks like Palantir if interest rates remain elevated or macroeconomic conditions worsen.

The OpenAI tool acknowledged that, historically, stocks with extreme valuations tend to experience extended declines rather than sudden collapses. To this end, if Palantir’s revenue growth slows below 30% year-over-year, investor confidence could erode, leading to further downside.

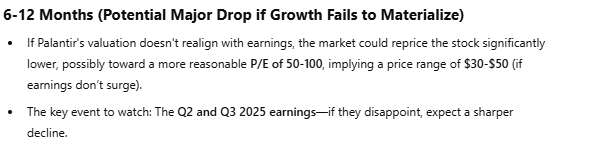

On the other hand, within the next six to 12 months, ChatGPT stated that if Palantir’s valuation remains disconnected from earnings, the market may significantly reprice the stock.

In this case, the AI platform suggested that if earnings don’t experience a substantial surge, Palantir could decline to a more reasonable P/E range of 50 to 100. This scenario would place the stock price between $30 and $50. With these timelines in mind, the Q2 and Q3 2025 earnings reports will be pivotal—disappointing results could catalyze a steeper fall.

Wall Street’s concerns on PLTR stock

The overvaluation concerns have also been echoed by some Wall Street analysts, who remain bullish on PLTR for the long term but foresee trouble in the short term. One major highlight of this outlook was shared by Jefferies, which maintains that PLTR faces a potential downside of over 60% due to valuation concerns.

As things stand, Palantir’s recent momentum was triggered by the company’s impressive Q4 2024 earnings report, which beat most analysts’ estimates. Adjusted earnings per share came in at $0.14 versus the expected $0.11.

Revenue was $828 million, surpassing the forecasted $776 million. The company also provided upbeat guidance, projecting Q1 revenue between $858 million and $862 million, well above the $799 million estimate.

Part of this growth heavily relies on Palantir’s significant contracts with government and commercial clients. Therefore, it is pivotal for the firm to continue attracting clients to justify its current valuation.

Featured image via Shutterstock