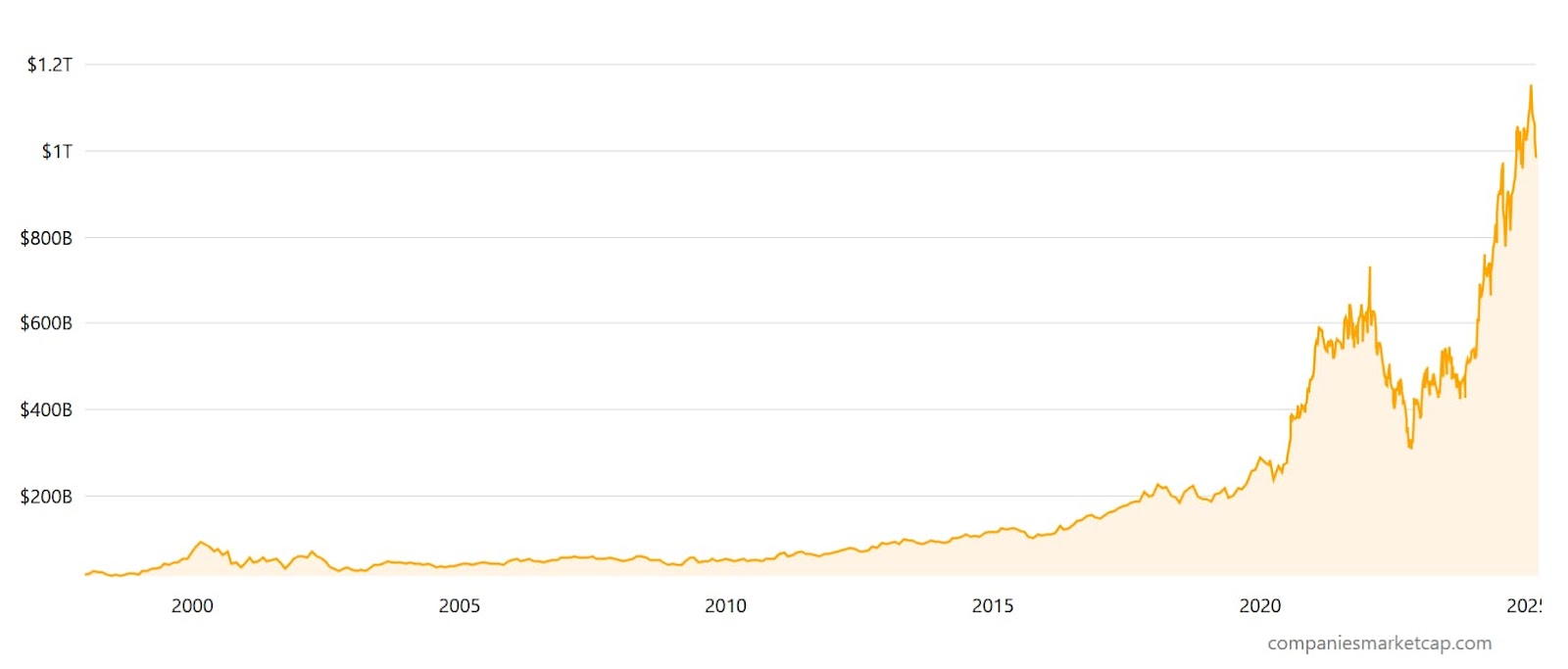

Having risen 49.56% in the last 12 months to its press time price of $192.33, it can hardly be said that Taiwan Semiconductor Manufacturing (NYSE: TSM) has been a poor performer during the ongoing artificial intelligence (AI) boom.

Despite the strong stock market performance, however, TSM’s shares likely remain relatively cheap due to the sheer importance of the company for the everyday operations of the modern world.

Why TSMC might be the most important company in the world

Indeed, TSMC controls a significant proportion of the chipmaking market share globally, with its pure-play foundry market share forecasted to hit 66% before the end of 2025.

Additionally, the company is a key supplier for well-known technology giants such as Apple (NASDAQ: AAPL), Nvidia (NASDAQ: NVDA), Advanced Micro Devices (NASDAQ: AMD), Broadcom (NASDAQ: AVGO), and many others.

Given the bullish expectations that AI will be profoundly transformative — and widely proliferated in the coming years — it should come as no surprise that the company manufacturing key components for the technology is expected to continue performing well.

Furthermore, while uses in artificial intelligence and other similar electronics are firmly in the public conscience, it is worth remembering that the modern world, in many ways, runs on microchips.

Beyond data centers, laptops, and smartphones, TSMC-manufactured semiconductors can be found in most cars and other vehicles leaving the assembly lines, numerous home appliances, medical devices, security systems, and on battlefields around the world.

In fact, despite energy remaining pivotal for the functioning of the world, it can easily be said that semiconductors are a serious contender to be what coal was during the Industrial Revolution and oil during the twentieth century.

Why TSMC stock could soar in 2025

The importance of TSMC is also evident in the company’s financials. For the entire year 2024, the manufacturer reported a record-breaking revenue of nearly $90 billion, with it recording more than $26 billion in the fourth quarter (Q4) of the year alone.

Considering the figures and the fact that TSM’s total market capitalization at press time on February 26 stands at $982.17 billion, while, for example, Nvidia’s stands at $3.1 trillion despite reporting a revenue of $60.9 billion for fiscal 2024, the semiconductor manufacturing giant has significant room for growth.

Still, despite TSMC giving a strong value proposition, it isn’t a riskless investment. To begin with, any investment in most companies in the sector, not just the firm itself would depend on one’s confidence the current trends will persist.

TSMC stock risks to consider

Indeed, many experts have been warning for years that an everything bubble has formed around big tech, with 2024 bringing many others who believe AI is in grave danger of collapsing and bringing the rest of the market with it.

For TSM to enjoy strong growth that would bring it in line with some of its most prominent peers, the ongoing boom would have to persist.

Beyond the potential economic calamities, the Taiwan Semiconductor Manufacturing Industry has something of a geography problem. To begin with, Taiwan is considered a province of China by the People’s Republic, and its status, according to most other countries, including the U.S., is ambiguous.

Not only does this fact ensure the island is a perpetual focal point of tensions, but it leaves some questions about its place in the global supply chain — an issue that is becoming especially pointed with President Donald Trump’s tariff-placing spree.

The additional dues imposed on or planned for numerous countries — including PRC and Taiwan — could also provide strong headwinds for TSMC shares.

Simultaneously, the factors that put TSM at risk could also prove a strong boon for the firm and its equity. The island’s unique geopolitical position all but ensures continued strong relations with Mainland China — and emergent AI powerhouse — while TSMC’s strategic importance led to its already operating foundries on American soil.