Michael Burry, famed for ‘The Big Short,’ has seen his top holding, Alibaba (NYSE: BABA), receive a notable upside price revision from Wall Street, with analysts highlighting the potential boost from artificial intelligence (AI).

As of Q4 2024, Alibaba accounted for 16.43% of Burry’s Scion Asset Management portfolio, emerging as a key winner in his holdings.

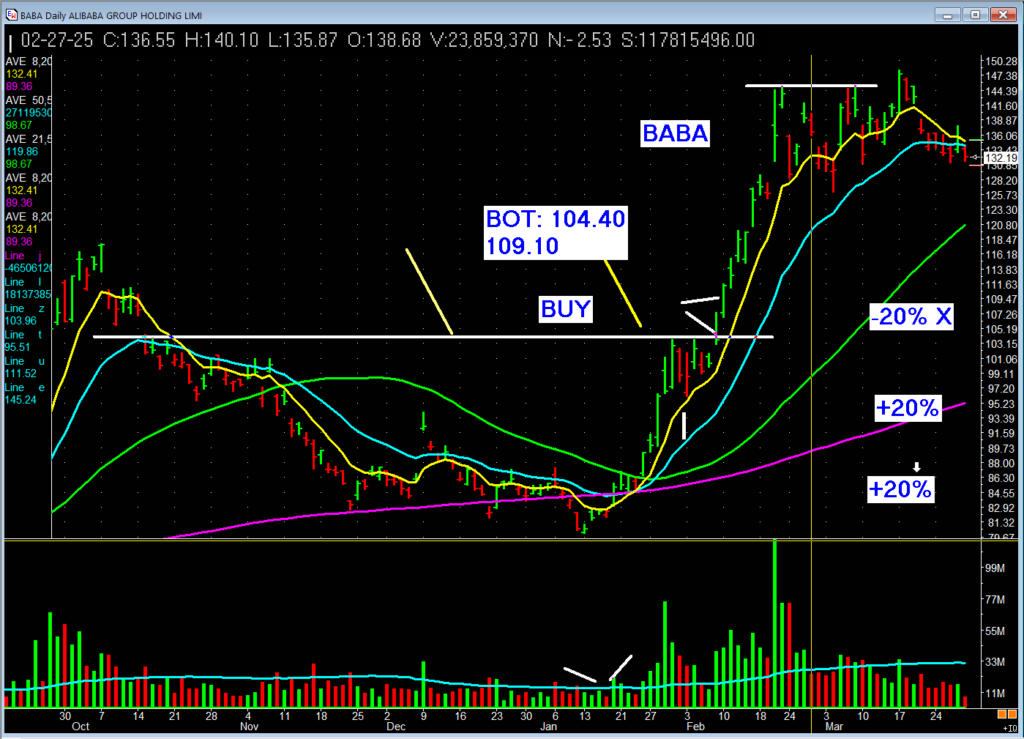

BABA has seen increased volatility in recent trading sessions, aligning with the general stock market movement. At the close of the March 28 session, Alibaba was trading at $132.43, down 2.36%. Year to date, BABA remains among the best-performing equities, having gained over 55%.

Picks for you

Commenting on the current price setup, stock trading expert Patrick Walker, in an X post on March 28, observed that the stock is consolidating after a strong rally but remains in good shape.

Walker noted that BABA’s breakout from key levels around $104.40 and $109.10 led to gains of over 20%. Despite the current pullback, the stock is experiencing a healthy consolidation within a strong uptrend.

Analysts update BABA stock price

On Wall Street, Mizuho Securities has raised its price target on the Chinese technology giant to $170 from $140, a 20% increase. The company maintains its ‘Outperform’ rating and is named a top pick in the Asia internet sector.

In an investor note on March 28, Mizuho analyst James Lee highlighted Alibaba’s positioning in the AI landscape as a key driver for the upgrade. Notably, BABA saw steady capital inflows earlier this month after announcing its new AI model, QwQ-32B. Benchmarks suggest it matches or outperforms DeepSeek’s top model, R-1.

Additionally, Lee stated that Alibaba’s foundation for scaling AI models toward artificial general intelligence (AGI), its platform for accelerating customer application deployment, and its potential to deliver end-user solutions across industries are key bullish catalysts for the stock.

“We believe the company has rock-solid building blocks for AI investments—scaling models toward AGI, building a platform for model APIs to accelerate application deployment for customers, and ultimately providing end-user solutions directly across industries,” Lee said.

At the same time, the analyst expressed optimism about Alibaba’s non-core businesses, projecting that losses from units outside its Taobao and Tmall Group (11% of EBITDA) could break even within two years.

Mizuho further lifted its fiscal year 2026 cloud revenue growth forecast from 13% to 17% year-over-year, citing a stronger product roadmap and improving sentiment around enterprise IT spending in China.

The revised $170 price target reflects a valuation of 12 times FY26E EBITDA, up from 10 times previously, driven by multiple expansions in China’s tech sector and improving macroeconomic conditions.

Overall, Wall Street is bullish on the Chinese e-commerce giant, projecting that Alibaba is poised to capture more market share. For instance, on March 13, Citi maintained a Buy rating with a $170 price target. The firm’s bullish stance is based on Alibaba’s ongoing inroads into AI, noting that the technology will open up new commercialization opportunities.

On February 26, Benchmark reiterated its ‘Buy’ rating with a BABA price target of $190, driven by estimated growth in e-commerce and cloud computing.

Meanwhile, on February 24, Bernstein upgraded its BABA rating to ‘Outperform’, raising the price target to $165 due to Alicloud’s potential under a Sum of the Parts valuation.

Alibaba fundamentals

Beyond the positive analyst outlook, Alibaba stock is backed by bullish fundamentals, showing strength after pandemic-induced losses.

Notably, with a recovering Chinese economy, Alibaba will likely see more growth, with retail sales increasing year-over-year for two consecutive years. As retail spending rises, e-commerce, Alibaba’s core business, could see double-digit growth.

Investor confidence is also returning after uncertainty as Alibaba’s leadership has solidified its corporate strategy following management shake-ups and the reversal of previous plans to spin off key businesses.

This newfound stability makes it easier to be optimistic about the company’s long-term prospects. At the same time, the Chinese government appears to be more favorable toward the country’s technology sector.

Disclaimer: The featured image in this article is for illustrative purposes only and may not accurately reflect the true likeness of the individuals depicted.