Micron Technology (NASDAQ: MU) has emerged as one of the biggest beneficiaries of the artificial intelligence boom, with its stock rallying sharply as demand for advanced memory chips continues to surge.

Amid the strong performance, investors are increasingly searching for a long-term prediction for Micron stock as the company strengthens its position in the AI infrastructure market.

As of press time, MU shares were trading at $1,133, having rallied by about 260% year-to-date.

The rally has been driven by surging demand for high-bandwidth memory (HBM), a key component in AI accelerators.

Micron is one of the few companies capable of producing HBM at scale, with reports indicating its HBM capacity is sold out through 2026.

The company has also benefited from tight memory supply, as demand for DRAM, NAND, and HBM continues to outpace production.

The favorable supply-demand balance has supported higher prices, stronger margins, and rising earnings expectations.

Against this backdrop, Finbold consulted OpenAI’s artificial intelligence model ChatGPT to assess Micron’s stock outlook over the next five years.

MU stock price prediction

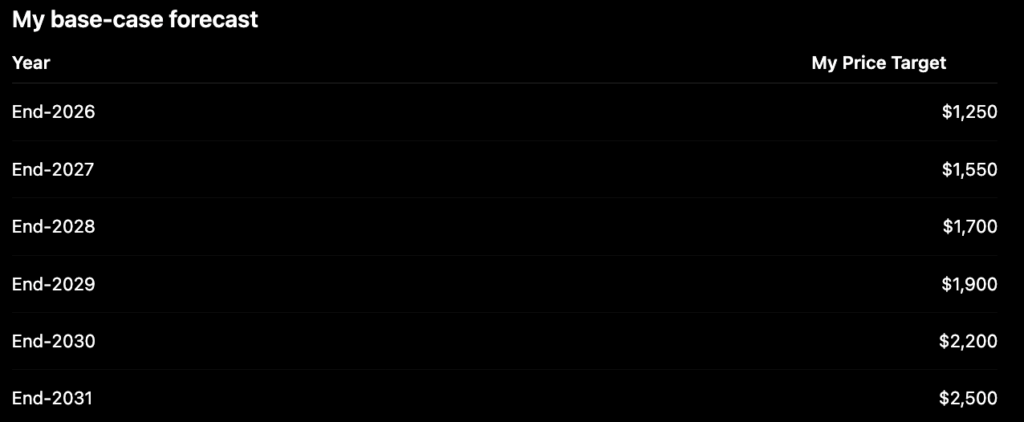

Based on current industry trends, ChatGPT projected a base-case scenario in which Micron stock reaches $1,250 by the end of 2026, $1,550 by the end of 2027, $1,700 by the end of 2028, $1,900 by the end of 2029, and $2,200 by the end of 2030.

Under this forecast, the stock would trade around $2,500 by 2031.

The prediction assumes AI spending remains strong throughout the decade, HBM demand continues to exceed supply through at least 2027, and Micron maintains its position as one of the leading suppliers of advanced memory products.

The model also noted that investors increasingly view Micron as an AI infrastructure company rather than a traditional cyclical memory manufacturer.

In a more bullish scenario, ChatGPT estimated that Micron could trade between $4,000 and $5,000 by 2031.

This outcome would require AI infrastructure spending to remain above expectations, continued supply constraints in the HBM market, and sustained pricing power as demand for AI systems expands.

However, the forecast also highlighted several risks, such as the memory industry has historically experienced periods of oversupply that pressure pricing and profitability.

Increased competition from rival manufacturers and any slowdown in AI spending could also weigh on future growth.

In addition, Micron’s strong rally has raised investor expectations, increasing the importance of continued earnings growth.

Looking ahead, Micron’s upcoming earnings report is expected to be a key catalyst. Investors will focus on HBM demand, pricing trends, margins, long-term supply agreements, and management’s outlook for AI-related growth.