Nvidia’s (NASDAQ: NVDA) share price could be on the verge of a rebound, with technical indicators signaling a potential turnaround after a series of volatile trading sessions.

NVDA’s price movements have mirrored broader market sentiment, wiping out much of its artificial intelligence (AI)-driven rally from the past year.

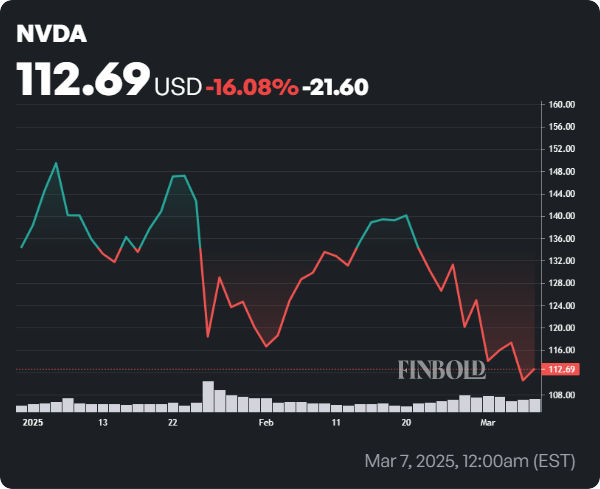

As of the last trading session, Nvidia closed at $112.69, gaining 1.9%. However, the stock remains under pressure, down nearly 9% for the week and 18% year-to-date.

What next for NVDA stock price

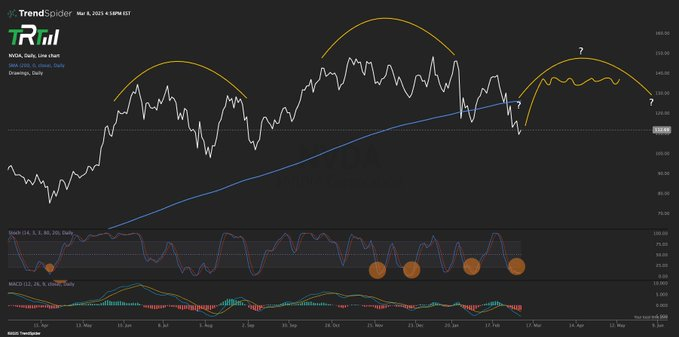

According to trading platform The Rock Trading, NVDA may be setting up for a bounce after recent oversold conditions. Their March 9 analysis suggested that the stock could rally toward the 200-day moving average (MA) near $127, with a potential push to $143 if momentum holds.

“NVDA is very much oversold, more so then Deepseek lows. It’s likely to rip back towards 200 MA currently $127, and probably straight in to $143 again,” the analyst said.

The analysis indicates that Nvidia’s stochastic relative strength index (RSI) has exited deep oversold territory, historically signaling strong rebounds. Meanwhile, the MACD indicator shows weakening selling momentum, further supporting a short-term rally.

However, the analysts warned that NVDA may be forming a head-and-shoulders pattern—a bearish reversal signal—suggesting that any recovery could be short-lived before a deeper decline.

On the other hand, Market Maestro also highlighted increased volatility and a potential trend shift for the chipmaker’s stock. In this case, NVDA is testing a key support zone between $112 and $128, marked as a “fair value gap.”

A break below this range could send the stock to $110 or even $70, while a strong rebound could push it back toward $150, a major resistance level.

The RSI has dropped to 41.38, nearing oversold territory. However, rising volume indicates heightened selling pressure, adding uncertainty.

NVDA stock’s fundamentals

Notably, Nvidia stock has shown lackluster performance despite reporting record revenue. For the fiscal fourth quarter, the technology giant posted $39.33 billion in revenue, surpassing the estimated $38.05 billion, with net income soaring to $22.09 billion, nearly doubling from a year ago.

The data center segment, now accounting for 91% of total sales, generated $35.6 billion, up 93% year over year. Blackwell, Nvidia’s next-generation AI chip, contributed $11 billion in revenue and is experiencing the fastest adoption in the company’s history. Looking ahead, Nvidia projects $43 billion in first-quarter revenue, implying 65% year-over-year growth.

Despite concerns over slowing expansion and competition from custom AI chips, Nvidia remains confident in its market position. In this light, the firm is banking on its next-generation Blackwell chips to drive the next wave of AI innovation.

These chips offer four times faster AI training, making AI inference twenty times cheaper than its predecessors. While the ramp-up in production has temporarily weighed on gross margins, this short-term issue will correct itself as efficiency improves.

Wall Street remains bullish on NVDA stock

Meanwhile, after the February 26 earnings report, a section of Wall Street remains mostly bullish on Nvidia stock.

For instance, BofA Securities raised its price target to $200 (from $190), maintaining a ‘Buy’ rating. Analyst Vivek Arya pointed to Nvidia’s leadership in AI compute and inference applications, highlighting Blackwell’s staggering $11 billion in sales—well above the expected $4 to $7 billion range.

JPMorgan reaffirmed its $170 price target and ‘Overweight’ rating, citing strong customer demand for AI compute and an accelerated Blackwell ramp.

Raymond James also maintained its $170 target, noting that Blackwell’s revenue is already outpacing its predecessor, Hopper. The firm highlighted the increasing importance of inference, with models like DeepSeek requiring significantly more compute power.

Needham stuck to its $160 price target, applauding Blackwell’s outperformance despite earlier overheating concerns. Analyst Rajvindra Gill revised gross margin estimates 100bps lower, projecting a slower recovery to ~75%. However, rising demand for inference is expected to sustain Nvidia’s AI momentum.

Summit Insights, in contrast, downgraded Nvidia stock to ‘Hold’, citing an unfavorable risk-reward balance. Analyst Kinngai Chan warned of slowing growth in the second half of FY26 as GPU supply catches up to demand.

Featured image via Shutterstock