![PayDo Review [2024] Multicurrency Business Account Features, Pros & Cons](/cdn-cgi/image/format=auto,quality=85/https://assets.finbold.com/uploads/2024/06/PayDo-Review-2024-Multicurrency-Business-Account-Features-Pros-Cons-1-1024x683.jpg)

Managing international payments can be challenging due to high costs, long transaction times, and multiple intermediaries. Opening a business account in a high-risk industry is not an easy feat as well. PayDo, a leading fintech company, offers a comprehensive solution.

In the scope of this review — the platform’s history, features, services, fee structure, and safety levels. To wrap up, we’ll give you a short list of PayDo’s pros and cons to highlight its strengths and weaknesses.

About PayDo

PayDo is a payment platform designed to make payment operations more convenient by allowing users to create multicurrency accounts with just one digital obligation-free contract. In addition, it offers comprehensive merchant and mass payment solutions, all conveniently managed within a single dashboard.

As a direct SWIFT participant with numerous Tier 1 correspondent banks, PayDo provides each client with a dedicated European IBAN upon account registration, containing essential details such as their name or business name.

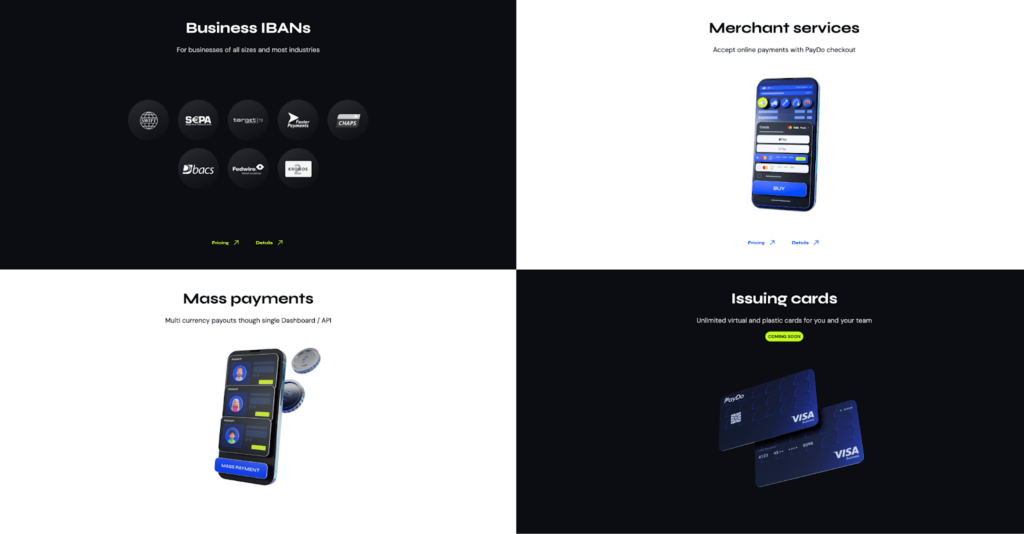

PayDo offers users the flexibility to use nine different payment schemes*:

- SWIFT

- SEPA

- SEPA Instant

- Faster Payments

- TARGET2

- Fedwire

- BACS

- CHAPS

- Kronos

* A payment scheme is a system that allows individuals and businesses to transfer money to one another. The more payment schemes you can access, the more destinations you can choose and currencies select.

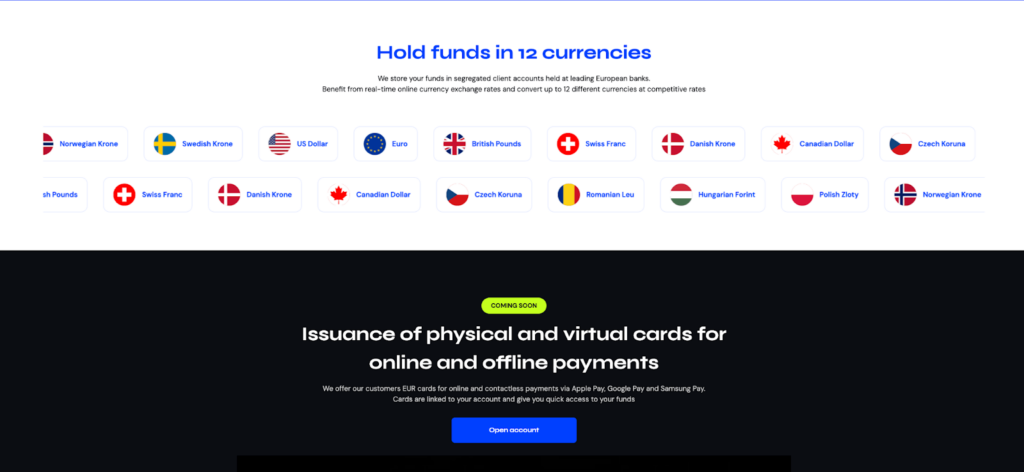

Additionally, the platform supports transactions in 24 different currencies, including Euro, USD, GBP, CAD, AUD, CHF, DKK, PLN, NOK, SEK, CZK, HUF, RON, BGN, BHD, AED, CNY, HKD, ILS, JPY, MXN, SGD, TRY, and ZAR. This multicurrency capability is one of PayDo’s unique advantages, complemented by PayDo’s SWIFT transactions’ T+1 settlement period (next-day delivery) and instant payment delivery for Euro (SEPA Instant)/GBP (FPS), which ensures fast and efficient service.

PayDo will soon offer both physical and virtual VISA Euro cards for online and offline transactions. The cards will enable customers to make purchases online and through contactless methods such as Apple Pay, Google Pay and Samsung Pay. These will be directly linked to their accounts. PayDo users have access to their funds whenever they need it.

In total, PayDo serves a wide range of industries. Most notable examples include the following:

- e-Commerce;

- Digital Marketplaces;

- Affiliate Marketing;

- IT and Software Companies.

- Import and Export;

- Video Game Studios;

- iGaming;

- Forex;

- Cryptocurrency and Blockchain;

- Payment Gateways (ISO).

In reality, PayDo can serve more than 95% of EMIs and banks out there.

Account Types Available With PayDo

There are three account types available with PayDo:

- Personal Account;

- Business Account;

- Merchant Account.

1. Personal Account

For individuals, PayDo offers a comprehensive solution tailored for managing multicurrency payments globally. Here’s what the PayDo Personal Account brings:

Features:

- Cross-Border Transfers. Users can send and receive international transfers, hold 12+ currencies, and make purchases on thousands of supported sites.

- Supported Currencies and Payment Schemes. Users can send and receive payments in around 150 countries and in over 12 currencies, including Euro, GBP, and AUD via SEPA, SWIFT, and Faster Payments. Storing funds in different currencies is free.

- Dedicated IBANs. These are available in two forms – as GBP account details as well as multicurrency account details.

- Paying at checkout with available balances. Make purchases on websites supporting PayDo checkout.

Top-Up Methods

- Bank Transfer

- Credit/Debit Cards

- Alternative Payment Methods (APMs)

- Local payment methods*

* Users from Brasil, Egypt, and other emerging markets can top up their account not only via bank transfer or card, but also local payment methods.

Additional Services:

- Payments to/from Other PayDo Users. Transfers between PayDo users are facilitated through internal transfers.

- Real-Time Reporting. Users can get detailed reports for convenient payment management and download their payment history for a custom period in PDF or Excel formats.

- Money Exchange. Clients can instantly convert money at favorable rates, with storing funds in different currencies being free and transparent.

Security

- Fund Safeguarding. As an EMI, PayDo stores user funds in segregated client accounts held at leading European banks. Client’s money are always available and protected, even if PayDo becomes insolvent.

- 3D Secure (3DS). Each card transaction is protected by 3DS technology. Users receive a unique one-time password via SMS to confirm transactions, involving the acquirer, issuer, and compatibility domain.

Cards

- VISA Euro Cards (Coming Soon). Clients will be able to apply for both physical and virtual VISA Euro cards for online and contactless payments via Apple Pay, Google Pay, and Samsung Pay. These cards will be linked to user accounts for quick access to funds.

For additional information, please watch this video.

2. Business Accounts

PayDo offers an advanced suite of financial services tailored to meet the needs of corporate clients, providing extensive global capabilities and robust security measures.

Key Features

- Dedicated IBANs with Multiple Currencies. Corporate clients receive dedicated European IBAN details with their company name for both sending and receiving payments. These IBANs support multiple currencies.

- Multicurrency and Multiple Jurisdictions. Access to multicurrency IBANs in jurisdictions such as the UK, Germany (DE), Denmark (DK), Switzerland (CH), and Lithuania (LT).

- SWIFT and SEPA Access. Business accounts include access to SWIFT, SEPA, SEPA Instant, and Faster Payments (FPS) networks. There are a total of nine payment schemes available.

- High-Value and High-Risk Transfers. PayDo supports high-value transfers of up to 3 million Euro and is friendly towards high-risk transactions.

What Makes PayDo Unique

- Global Reach. Supports cross-border and third-party payments to/from over 140 countries, making it ideal for international operations.

- Wide Correspondent Banking Network. Ensures reliable transaction routing. If a payment fails with one correspondent bank, it is automatically routed through another, guaranteeing successful transfers.

- Transparent FX and Instant Conversions. Provides real-time currency exchange rates and instant conversions within the dashboard, with no minimums and no hidden fees.

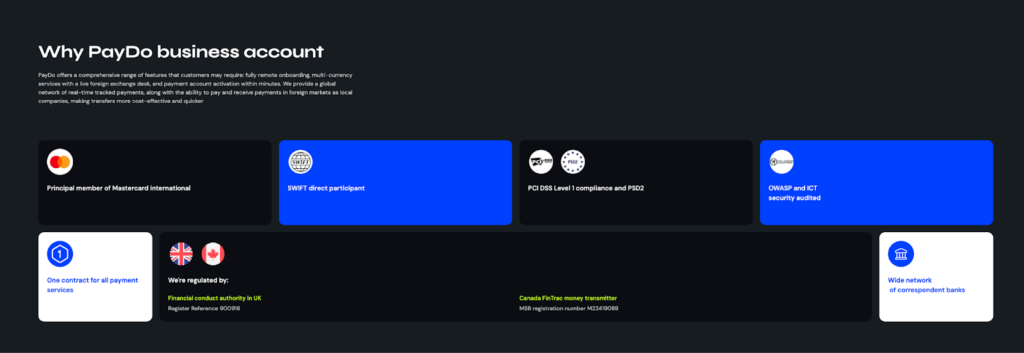

- Principal member of Mastercard International. PayDo can issue its own Mastercard-branded credit or debit cards and acquire transactions directly, without needing a third-party bank.

- SWIFT Direct Participant. PayDo users can directly send and receive international payments via the SWIFT network, which is a global system for secure financial messaging.

- No Hidden Fees. Transparent pricing with no hidden charges, ensuring clear and predictable costs for all transactions.

- Settlement from Merchant Providers. Consolidates settlements from various merchant providers into one place, simplifying financial management.

Additional Services

- Merchant Solutions. Businesses can leverage PayDo’s merchant solutions to accept over 350 payment methods, enhancing their ability to cater to a global customer base.

- Mass Payments. Facilitates bulk payouts to employees, freelancers, and contractors in various currencies. Integration via API allows seamless management directly from business systems.

- Physical and Virtual Cards. PayDo will soon offer unlimited virtual and physical VISA Euro cards for businesses, providing flexible payment options for online and offline transactions.

Security and Compliance

- Advanced Security Measures. Ensures the highest level of security with PCI DSS Level 1 compliance*, OWASP audits**, and real-time fraud detection.

- Regulatory Compliance. Fully compliant with the Financial Conduct Authority (FCA) regulations in the UK and FINTRAC regulations in Canada.

* This is the highest level of compliance and is required for organizations that process over 6 million card transactions per year. Being Level 1 compliant means an organization has met the most stringent security requirements, ensuring the highest level of protection for credit card data.

** These audits involve reviewing and testing web applications to identify and fix security vulnerabilities. OWASP audits check web applications for security weaknesses to protect against hacking and data breaches.

User Experience

- Simple Onboarding. Fully remote onboarding process, typically completed within five business days with standard documentation.

- Comprehensive Dashboard. User-friendly dashboard for managing all financial operations from a single interface, ensuring transparency and ease of use.

3. Merchant Account

With a PayDo Business Account, owners have the opportunity to establish a merchant account, offering a powerful and comprehensive checkout solution. Here’s an updated overview of what the PayDo Merchant Account brings:

Key Features

- PayDo Checkout. A secure, user-friendly payment page that helps merchants collect payments from customers across both desktop and mobile devices. It offers a high acceptance rate with an intuitive flow and top-notch user experience (UX).

- Payment Methods. Supports 350+ global and local payment methods, including cards, bank transfers, and alternative payment methods (APMs):

- Prepaid cards

- Cash-based payments

- E-wallets

- Mobile wallets

- BNPL

Covers 170+ countries, providing extensive reach for merchants.

- One-Click Payments. Customers can link their cards to PayDo and pay with a single click, eliminating the need to re-enter card details for each transaction.

- Smart Payment Selection. Automatically localizes payment methods based on the payer’s country, determined by browser and IP geolocation. Clients can make purchases in payment methods they are familiar with.

* It can be prepaid cards, cash-based payments, e-wallets, mobile wallets, BNPL, and many more.

Security and Compliance

- PCI DSS Level 1 Certification. Ensures the highest level of data security compliance, protecting card information and transactions.

- 3D Secure (3DS). Provides extra fraud protection, requiring customers to complete additional verification with the card issuer during payment.

- Built-In Anti-Fraud. Automated, self-optimizing fraud management solution with real-time monitoring of all transactions.

- Chargeback Protection. Reduces the number of chargebacks to zero by processing payments through the PayDo account balance. PayDo experts handle chargeback requests, verifying claims to minimize fraud.

Integration and Onboarding

- API Integration. Integration is simplified through API (Hosted Page or Server to Server) or via popular eCommerce platform plugins (such as Woocommerce WordPress, PrestaShop, Opencart 3.0+/v2.3).

- Unified Contract. Access all major payment methods with one contract and single API integration. No need for multiple contracts for each payment method.

- Automated KYC. Automated Know Your Customer (KYC) process triggered after account creation and based on transaction amount. It includes ID card verification, face recognition, and document verification.

- No Rolling Reserve. PayDo does not hold a rolling reserve, making funds readily available for use and settlement.

Additional Benefits

- Routing & Cascading. Smart routing and cascading features direct transactions to channels to approve them, reducing declines and increasing acceptance rates.

- Transparent FX and Instant Conversions. Real-time currency exchange rates and instant conversions within the dashboard. No minimums and no hidden fees.

- High-Risk Friendly. Supports high-value transfers of up to 3 million Euro and is friendly towards high-risk transactions.

- Pricing. Competitive Tier 2 & 3 pricing models.

- Comprehensive Dashboard. Manage all financial operations from a single interface, ensuring transparency and ease of use.

While PayDo accommodates most business models, certain conditions may apply to specific types of businesses. Integration is simplified through API (Hosted Page or Server to Server) or via popular eCommerce platform plugins (such as Woocommerce WordPress, PrestaShop, Opencart 3.0+/v2.3). For additional information, please contact the PayDo Sales Team.

Services Provided by PayDo

PayDo offers several services to personal and business account owners:

- Cross-border Multicurrency Transfers;

- Merchant Solutions;

- Mass Payments;

- Online Payments;

- Debit Cards (coming soon);

- Foreign Exchange.

1. Cross-border Multicurrency Transfers

In traditional banking, multicurrency payments can be complex and often come with additional fees and documentation requirements. PayDo simplifies this with a multicurrency business account, offering quick verification and support for nine payment schemes across 140+ countries. With a dedicated IBAN, it enables transfers (up to 3 million Euro) and global payments in 24 currencies. No additional fees included.

What are Payment Schemes?

Payment schemes are different systems or networks used to transfer money between banks and financial institutions. These schemes ensure that payments are processed quickly and securely. Here are the main ones supported by PayDo:

- SWIFT. A global network used for international money transfers between banks. It is widely used for cross-border payments.

- SEPA. The Single Euro Payments Area scheme is used for Euro-denominated payments within Europe, making cross-border Euro transactions as simple as domestic ones.

- Faster Payments (FPS). A UK-based system that allows for quick payments within the UK, usually processed within seconds.

- SEPA Instant. A faster version of SEPA that enables real-time Euro payments within Europe, processed almost instantly.

These payment schemes allow businesses to send and receive money efficiently, both domestically and internationally, enhancing their global reach and operational flexibility.

2. Merchant Solutions

PayDo’s merchant solutions boost sales and ensure rapid payments. By accepting over 350 payment methods, merchants can cater to customers worldwide, leading to larger purchases and instant transaction processing. The platform supports multiple currencies and offers a convenient checkout experience with local payment methods and languages.

Types of Payment Methods Supported

- Bank Transfers. Direct bank transfers for easy payment processing.

- Credit and Debit Cards. Including Visa and Mastercard, allowing broad acceptance.

- Vouchers and Prepaid Cards. Options for customers preferring pre-paid methods.

- Cash Payments. Available in certain regions through partners.

- Alternative Payment Methods (APMs). Support for a variety of popular local and international APMs.

Notable Payment Methods

- PIX (Brazil). A popular instant payment system in Brazil.

- Interac (Canada). A widely used debit card service in Canada.

- Fawry (Egypt). A prominent payment method in Egypt for both online and offline transactions.

Compliant with PCI DSS Level 1 and using 3D Secure, PayDo adds an extra layer of security. Features like one-click payments, instant KYC, and the ability to save card details enhance convenience. Besides, PayDo offers an elaborate chargeback prevention feature to make sure acceptance rate is high.

3. Mass Payments

PayDo’s mass payment service facilitates multiple payouts. By integrating via API, businesses can manage payouts directly from their websites, making it ideal for distributing salaries, paying freelancers, and handling payouts for players. Users can send funds to hundreds of PayDo accounts with a single click, whether from the PayDo Business dashboard or their CRM systems.

Benefits

- Quick and Reliable. Ensures fast and reliable payouts, tailored to meet the diverse needs of various industries.

- Seamless Integration. Can be integrated with popular e-commerce plugins and business systems, enhancing operational efficiency.

- AML Compliance. All payments within PayDo stay AML-compliant*, ensuring security and regulatory adherence.

- Customer Trust. Builds trust among customers by offering a seamless and reliable payment experience.

*AML compliance means following rules and procedures to prevent money laundering. By being AML-compliant, PayDo ensures that all payments are checked and monitored to prevent illegal activities, keeping the payment process safe and secure.

This process supports multicurrency transactions, which allows businesses to manage their global cash flow efficiently and reduce administrative overheads. The service is tailored to meet the diverse needs of industries, ensuring quick, reliable, and cost-effective payouts.

4. Online Payments

PayDo offers a secure and convenient online payment experience. Here are some notable features coming with the service:

- Bill Payments. Users can easily pay bills and set up automatic payments for recurring expenses.

- Purchase Management. Make purchases online with secure transactions.

- Save Recipient Details. Securely save recipient details for quick and easy future payments.

- Real-Time Transaction History. Provides real-time access to transaction history, allowing for quick expense tracking and detection of unauthorized transactions.

- Secure Environment. Ensures the highest level of security with advanced encryption and fraud detection measures.

- User-Friendly Interface. Offers a user-friendly dashboard for easy navigation and management of finances.

- No Account Maintenance Fees. PayDo operates on a pay-as-you-go basis with no account maintenance fees.

5. Debit Cards

PayDo clients will soon have the option to order VISA Euro cards (both physical and virtual) under their company’s name. These debit cards will assist the holder in managing regular payments for online tools used by software engineers, facilitate payments for advertising campaigns to promote products, and enable companies to pay employee salaries and engage in smart budgeting strategies.

6. Foreign Exchange

PayDo’s foreign exchange (FX) services simplify managing multiple currencies with support for over 24 currencies and integration with major payment schemes like SWIFT and SEPA. Users enjoy real-time exchange rates with no hidden fees, instant currency conversions, and comprehensive features such as detailed transaction histories and real-time reporting.

Ideal for businesses, freelancers, and e-commerce platforms, PayDo facilitates cross-border payments in over 140 countries, ensuring security and compliance with international standards. Funds are safeguarded in segregated accounts at leading European banks, providing a reliable and efficient solution for global financial management.

How to Get Started With PayDo

Getting started with PayDo is free and rather straightforward. To open an account, simply head over to the PayDo homepage and click on the Open account button (as shown below):

Next, you will be redirected to a new page where you’ll have to provide your email and come up with a password. If you wish to create a business account, click on the Create a business accountbutton at the bottom (as shown below):

Once you’ve provided your email and chosen a password, click on the Create an account button. Next, go to your email inbox and open the account confirmation email sent by PayDo. There, you will find a link you can click on to confirm your email (as shown below):

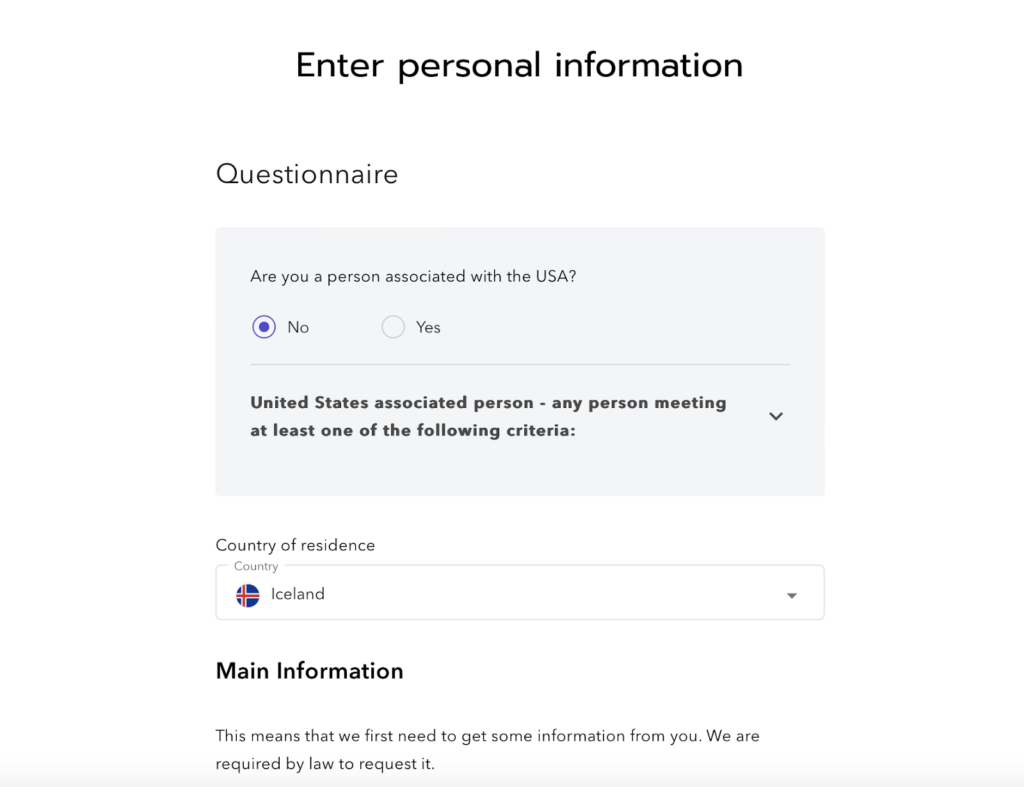

Once you’ve clicked on the link in the email, your email will be verified. Then, you can go back to the PayDo website, log in with your email and chosen password, and proceed to fill out a short questionnaire before exploring the platform:

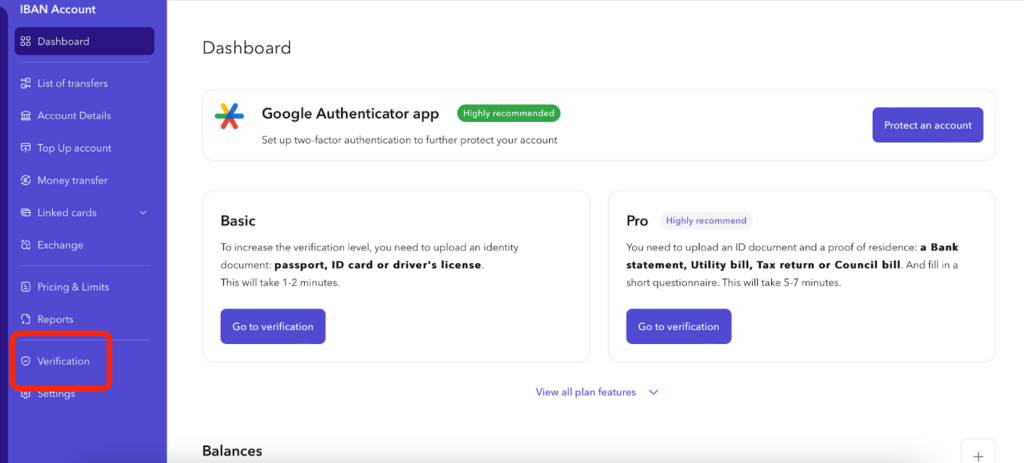

Once you’ve completed the questionnaire, you’ll be redirected to the main PayDo dashboard. First, you should verify your account. To do so, go to the main PayDo interface and click on the Verification option on the left-hand side (as shown below):

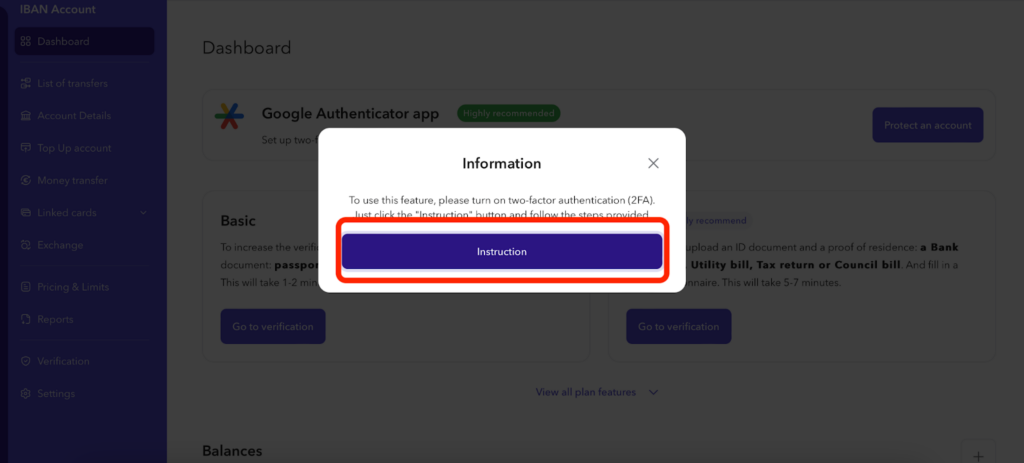

A new menu will pop up, so just click on the Instructions button (as shown below) and follow the platform’s verification instructions.

Here, you can find all the relevant information on how to pass complete verification successfully.

Once you have verified your account, you’ll be able to explore PayDo’s features freely.

Is PayDo Safe?

As a regulated Electronic Money Institution (EMI), PayDo operates under the UK’s Financial Conduct Authority (FCA), ensuring your money is handled with care and accountability.

PayDo also has mandatory user verification to meet the stringent PCI DSS Level 1 compliance standards for merchant services, meaning every aspect of the platform is designed with your safety in mind.

When it comes to safeguarding your funds, PayDo keeps customer funds separate from the company’s own accounts and securely held in banks.

The platform also incorporates real-time fraud detection, biometric authentication like Face ID/Touch ID, and 3D Secure (3DS) for card payments to ensure that your money stays safe.

The Payment Card Industry Data Security Standard (PCI DSS)

The Payment Card Industry Data Security Standard (PCI DSS), developed by the Payment Card Industry Security Standards Council (PCI SSC), ensures the security of payment data for cardholders across major international payment systems like Visa and MasterCard.

It applies to various entities involved in payment processing. Compliance is crucial for businesses to protect sensitive data and maintain customer trust. Non-compliance can result in significant financial losses and damage to reputation.

3D Secure

3D Secure technology, created by Visa and MasterCard, adds a layer of security to online payments by sending a unique one-time password via SMS to confirm transactions. It involves the acquirer, issuer, and compatibility domain.

PayDo uses 3D Secure to safeguard transactions. While 3D-Secure reduces fraud risk, some find it cumbersome, and its availability varies among merchants and banks.

Financial Services Compensation Scheme and Data Safeguarding

PayDo, as an Electronic Money Institution (EMI), ensures the safety of electronic money, including digital currencies and e-wallets. Unlike banks, EMIs like PayDo keep customer funds separate from operational funds, in compliance with The Electronic Money Regulations 2011 (EMR 2011) and The Payment Services Regulations 2017 (PSR 2017), which guarantees customer funds are always available for withdrawal.

In contrast to traditional financial safeguards like the Financial Services Compensation Scheme (FSCS), PayDo employs specialized techniques to safeguard funds. These methods include keeping all necessary funds in accounts at UK, EEA, and Swiss credit institutions, ensuring real-time protection and monitoring of funds, and meticulously managing financial matters in-house.

Unlike banks, EMIs like PayDo do not participate in the FSCS since they do not invest or lend client funds. Instead, they adhere to stringent safeguarding requirements set by regulatory authorities. In the event of PayDo facing insolvency, customer funds remain unaffected.

Why Do Users Choose PayDo?

Using PayDo, both private entities and businesses can potentially have numerous benefits not always available with traditional banking methods. For instance, you can collaborate with clients across over 140 countries worldwide, facilitating easy fund transfers, with quick online payments for goods and services becoming readily accessible through well-known systems like SWIFT, SEPA, and Target2.

Moreover, PayD is integrated with over 2500 online merchants, and for business owners, opening a digital PayDo account proves advantageous in providing modern, efficient services to customers. These accounts allow for centralized transaction management accessible from any location, at any time through a single account, as well as quick checkout from PayDo.

PayDo Fees

PayDo fees are personalized, both for personal and business accounts.

For private users, details such as Monthly IBAN fees and SEPA and SWIFT transfers will vary based on the country of your residence, as will transfers between different PayDo accounts and exchanges between available currencies in the account. Some actions, such as account registration, are free for all users. To check exact fees, personal users are encouraged to head over to PayDo’s official Personalized Pricing calculator.

Business account fees will likewise vary based on a number of factors. The most important things to take into account are the country of incorporation of your business, the industry you’re working in, the age of your enterprise, and the projected monthly turnover volume. To calculate exact fees, business account holders can visit the PayDo IBAN pricing page.

Pros and Cons of PayDo

Pros

- Registration and account maintenance are free;

- There are personal and business accounts;

- Supported by over 2500 online merchants;

- Regulated by the Financial Conduct Authority (FCA).

Cons

- PayDo is not as commonly used as some other, more established payment services;

- There is no dedicated mobile app on either iOS or Android.

PayDo Platforms and Social Media Channels

You can discover all the crucial details about PayDo and its development on the official website, blog, and social media channels:

- Website: Find the most important information about PayDo’s payment services and account registration on the official PayDo website;

- Blog: You can also find important updates, news, and educational posts on the PayDo official blog.

PayDo social media platforms:

- LinkedIn: PayDo has a presence on the largest business-oriented social media platform. Besides, the company offers its own Fintech Digest;

- Facebook: You can follow PayDo on Facebook for quick, regular updates;

- Instagram: Check out the PayDo Instagram page for news, updates, and announcements;

- TikTok: Follow PayDo on TikTok for video content on the product;

- YouTube: Subscribe to the PayDo YouTube channel for video updates and educational content.

Conclusion

In this review of PayDo, a multicurrency transfer platform and debit/virtual card provider, we explored its history, features, services, fee structure, and safety measures. In conclusion, we can say that PayDo offers streamlined payment operations, allowing users to create multicurrency accounts with one digital contract.

As an authorized partner of major card processors like Mastercard, PayDo provides dedicated and pooled Euroopean IBANs for seamless fund transfers and offers flexible payment solutions. It also caters to both personal and business needs, offering features like personal accounts, business accounts with merchant capabilities, and soon, VISA Euro corporate debit cards.

While PayDo boasts many advantages, such as being regulated by the FCA and offering free registration and account maintenance, there are considerations to be aware of, including personalized fees and restrictions on certain types of transactions. Overall, however, PayDo provides a modern, efficient solution for international financial transactions, making it a potentially compelling choice for users worldwide.

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.

PayDo FAQs

What is PayDo?

PayDo is a financial services company that facilitates international online financial transactions, catering to businesses, private entrepreneurs, merchants, freelancers, and other kinds of professionals looking for a straightforward and convenient method for accepting and sending payments. Its chief goal is to streamline the process by minimizing bureaucracy and the required documentation for launching transactions.

Is PayDo legit?

Yes, PayDo is a legit payment service. As a regulated Electronic Money Institution operating under the Financial Conduct Authority (FCA), it maintains mandatory user verification to meet the stringent PCI DSS Level 1 compliance standards for merchant services. Additionally, customer funds are kept separate from the company’s accounts and securely held in banks, providing an extra layer of protection.

Note also that although PayDo accounts aren’t covered by the Financial Services Compensation Scheme (FSCS) like those you open with traditional banks, mandatory safeguarding measures ensure that if the platform goes out of business, you will still receive 100% of your money back.

Is PayDo audited?

PayDo has undergone PCI-DSS Lvl1 and OWASP audits.

What are the fees like at PayDo?

At PayDo, fees are personalized for both personal and business accounts. For personal users, fees for Monthly IBAN, SEPA, and SWIFT transfers — as well as transfers between PayDo accounts and currency exchanges — depend on their country of residence. Business account fees also vary based on several factors, including the country of incorporation, industry, age of the business, and projected monthly turnover volume.

What do clients say about PayDo?

In general, the product can boast with decent reviews. While there is still room for improvement, the bigger chunk of PayDo reviews are really great.

Can I open a PayDo account for free?

Yes, you can open a PayDo account for free.

Is there a dedicated PayDo mobile app?

No, PayDo does not have a dedicated mobile app.

What countries is PayDo available in?

PayDo is available in a number of countries, including the United Kingdom, Austria, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, and Sweden.