Upstart (NASDAQ: UPST), a rising name in artificial intelligence (AI)-driven lending, is drawing attention following a strong earnings report that has fueled the equity’s growth.

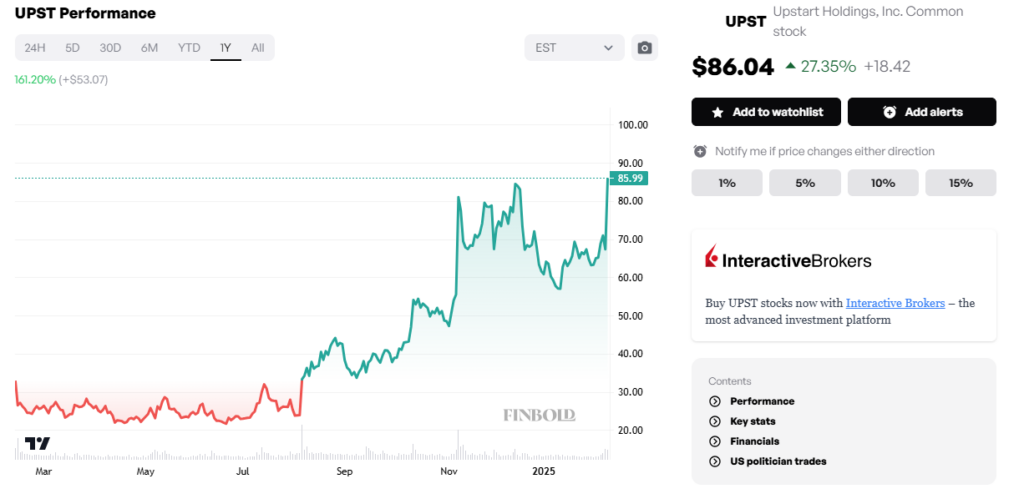

As of press time, Upstart’s stock was trading at $86.04, surging 29% in the past 24 hours and extending its recent upward momentum. Over the past year, the stock has skyrocketed 161%, reaching a new 52-week high.

The latest UPST spike reflects investor confidence in the financial company after beating revenue estimates for Q4 2024. Upstart reported $219 million in Q4 revenue during the last three months of 2024, marking a 56% year-over-year increase and a 35% jump from the previous quarter.

The revenue breakdown indicates that fee-based returns reached $199 million, up 30% annually and 19% sequentially. Net interest income came in at approximately $20 million, while origination volume surged 33% quarter-over-quarter and 68% year-over-year.

Wall Street updates UPST stock price

Following the blockbuster earnings and resulting stock rally, several Wall Street analysts are also taking note of Upstart’s potential, with many revising their price targets upward.

For instance, Mizuho’s Dan Dolev hiked his target from $90 to $110, citing Upstart’s impressive revenue guidance for the full year 2025, which is now 20% higher than consensus. Despite challenging macro conditions, such as prevailing uncertainty around interest rates, Dolev believes improved risk models will fuel further stock gains.

Meanwhile, JPMorgan’s (NYSE: JPM) Reginald Smith upgraded Upstart to Neutral from Underweight and lifted his price target from $57 to $79. He noted that the company’s underwriting improvements and increased funding availability have driven origination volume and margins to their highest levels since 2022.

“We see Upstart’s model improvements as a force multiplier that has the potential to boost conversions/transaction volume and unlock operating leverage (e.g., better yield on marketing spend). We are upgrading shares to Neutral (from Underweight) and raising our December 2025 price target to $79 (from $57),” Smith said.

Adding to the bullish sentiment, Citi’s Peter Christiansen raised his price target from $87 to $108, emphasizing Upstart’s AI-driven risk separation and a projected 60% revenue growth for FY25.

Upstart fundamentals

Beyond the impressive earnings report, Upstart has several underlying fundamentals that could drive further stock growth. At the top of the list is the company’s focus on AI-driven lending, its biggest advantage.

This technology sets Upstart apart from traditional financial institutions as it does not solely rely on conventional credit metrics. Notably, Upstart incorporates nontraditional data points to assess creditworthiness. This approach allows the company to approve a broader range of borrowers, particularly younger applicants or those with limited credit histories.

Although uncertainty remains regarding the next interest rate cut decision, the current low-rate environment is favorable for Upstart’s growth. Lower interest rates encourage borrowing, which, in turn, increases loan originations and drives.

In contrast, a high-interest rate environment can put significant pressure on the company as cautious lending partners pull back, forcing Upstart to hold more loans on its balance sheet.

In conclusion, Upstart’s strong fundamentals and bullish analyst sentiment position it for long-term growth. The stock offers an attractive entry point at its current price. Still, risks such as interest rate shifts and competition could impact future performance, making it a promising yet cautious investment.

Featured image via Shutterstock