Changes in the banking sector occur now at an accelerated pace, a bank now sees changes in a year that used to take decades to play out. These changes are reflected in loan-to-deposit ratios as well as what is put on the balance sheet of banks which in turn influences the bank’s performance.

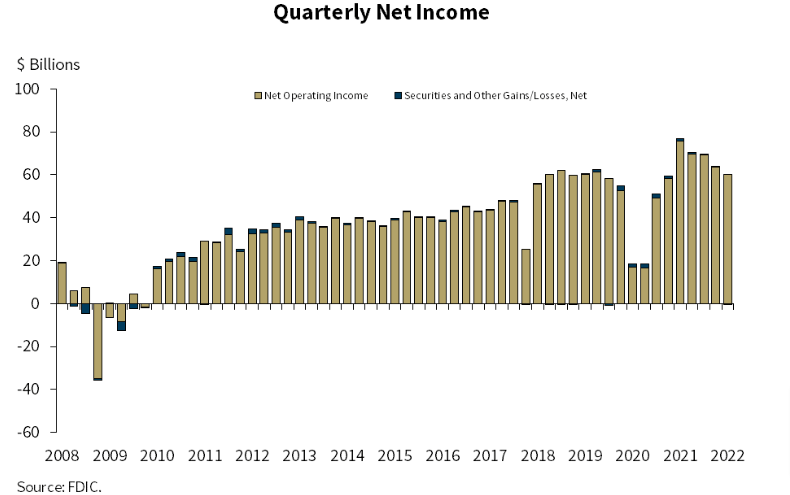

The banking industry quarterly net income dropped by 22%, in Q1 2022, compared to 2021, according to an FDIC report released on May 24. With community banks reporting a slight decline in net income, the credit quality improved, with net interest margins remaining stable quarter-over-quarter (QoQ).

After going through the pandemic, the banking sector shifted its attention to gaining a better understanding of the current situation in order to expedite reform. However, 2022, made it all the more challenging with inflation rising and the war in Ukraine causing various market disruptions.

Meanwhile, the FDIC Acting Chairman Martin J. Gruenberg offered an explanation on the state of the banking industry in the FDIC press release:

“The banking industry reported a decline in net income driven by an increase in provision expense. Capital and liquidity levels remain strong. In addition, loan growth and credit quality metrics remain generally favorable. Looking forward, inflationary pressures, rising interest rates and continued pandemic and geopolitical uncertainty will likely be headwinds for bank profitability, credit quality, and loan growth.”

Deposit growth and reserve ratios

On the whole, deposits in banks continued to increase for Q1 2022, led by the growth of insured deposits totaling $230.7 billion, an increase of 1.2% QoQ. Compared to the historical levels, the deposits remain elevated while the growth rates are below outlier quarters in 2020 and 2021.

Similarly, assets of banks that are listed as “problem banks” increased by $3 billion, to a total of $173.1 billion, which is comparable to the 2013 levels. Yet, the number of banks listed as “problem banks” has declined and is at the lowest since quarterly banking performance data collection began in 1984.

Conversely, the Depositor Insurance Fund (DIF) balance was $123 billion, a decrease of $100 million, for the quarter, representing the first decline in more than a decade. Insured deposits increased by 2.5% for Q1 to $10 trillion. These factors contributed to the decline of the reserve ratio by 1.23%, not taking the surge of deposits seen during the pandemic, a decline in reserve ratios that hasn’t been seen since 2009.

It would be hard to argue that the banking industry hasn’t made great strides since the 2008 crash, leading to some banks imploding and customers losing their savings. Bank shares at the time have seen massive re-ratings, but as it seems now, the balance sheets of banks are steady and still improving.