Dell Technologies (NYSE: DELL) is gaining momentum as investors respond positively to the company’s surging demand for artificial intelligence infrastructure.

The company has evolved from a traditional PC and server provider into a major AI player, a shift that has fueled strong gains in its stock price.

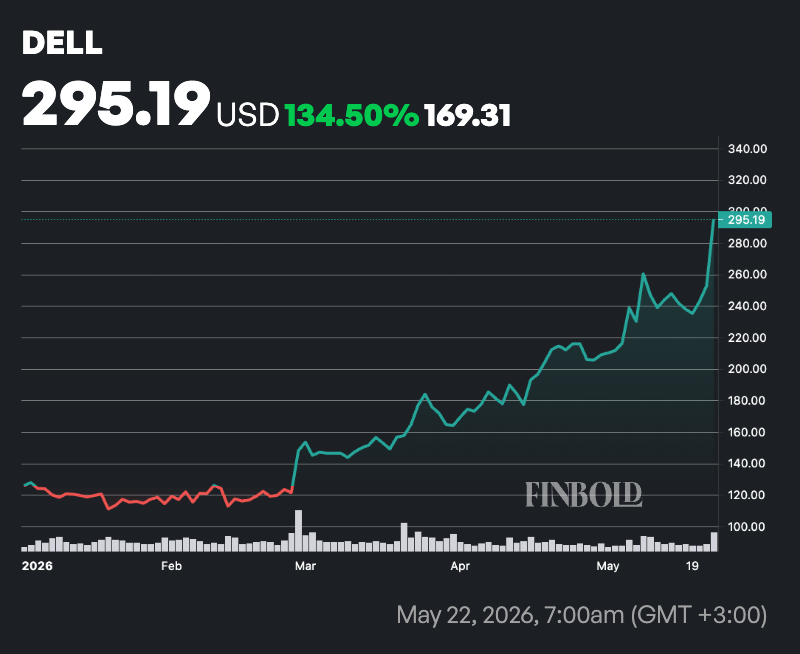

By press time, DELL stock was trading at $295 after closing Friday up nearly 17%, while the equity has rallied 130% year-to-date.

The main driver behind Dell’s rally is the explosive demand for AI-optimized servers and infrastructure. Dell ended fiscal 2026, which concluded in January 2026, with a record $43 billion AI server backlog.

In the fourth quarter alone, the company reported about $34 billion in AI-related orders and shipped between $9 billion and $9.5 billion in AI servers, marking a 342% year-over-year increase.

At the same time, Dell’s broader financial performance also underscored this momentum. Fiscal 2026 revenue rose 19% year-over-year to $113.5 billion, while adjusted earnings per share climbed 27% to $10.30.

The Infrastructure Solutions Group, which includes servers, delivered particularly strong results, with AI contributing a rapidly growing share of total revenue.

Looking ahead, Dell raised its long-term outlook through fiscal 2030, projecting annual revenue growth of 7% to 9% and adjusted EPS growth above 15%, driven by continued AI infrastructure spending.

The company also forecast strong AI revenue growth in fiscal 2027, reinforcing confidence in its expansion trajectory.

Wall Street bearish on DELL stock

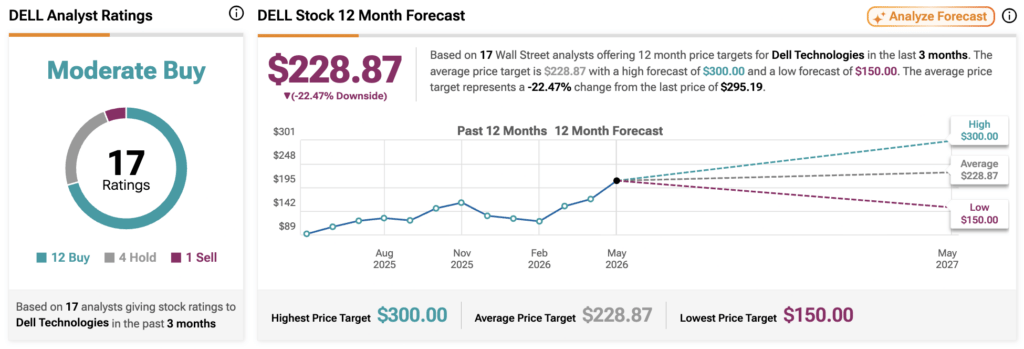

Despite the stock’s strong growth, Wall Street analysts are projecting downside potential for DELL shares over the next 12 months. According to data from 17 Wall Street analysts tracked by TipRanks, Dell maintains a ‘Moderate Buy’ consensus.

Of these, 12 analysts recommend buying the shares, four suggest holding, and one advises selling. The average 12-month price target stands at $228.87, implying a potential downside of approximately 22.5%, while the highest target of $300 and the lowest target of $150 reflect differing views on the stock’s valuation and potential technology sector headwinds.

On May 22, Wells Fargo analyst Aaron Rakers reiterated an ‘Overweight’ rating and sharply increased his price target to $270 from $180, citing Dell’s strengthening AI momentum and favorable positioning ahead of earnings.

A day earlier, Morgan Stanley analyst Erik Woodring lifted his target to $170 from $110 while maintaining an ‘Underweight’ rating. Although the firm acknowledged Dell’s long-term AI growth prospects, it remained cautious about the stock’s rich valuation following its recent rally.

BofA Securities also turned more optimistic, with analyst Wamsi Mohan raising his price target to $280 from $246 on May 18 while maintaining a ‘Buy’ rating. The revision reflected continued strength in AI server demand and improving enterprise adoption trends.

JPMorgan followed with its own upward revision on May 15, increasing its target to $280 from $205 and maintaining an ‘Overweight’ rating. The bank cited easing memory-related cost pressures and growing earnings contributions from AI servers.

Not all firms turned more constructive, however. UBS analyst David Vogt downgraded Dell to ‘Neutral’ from Buy on May 11, though he still raised the price target to $243 from $167. UBS said Dell’s business fundamentals remain solid but argued the stock’s recent surge has created a more balanced risk-reward setup.