Leadership turmoil at Lucid Group (NASDAQ: LCID) has sent its stock tumbling, though Wall Street remains cautiously optimistic.

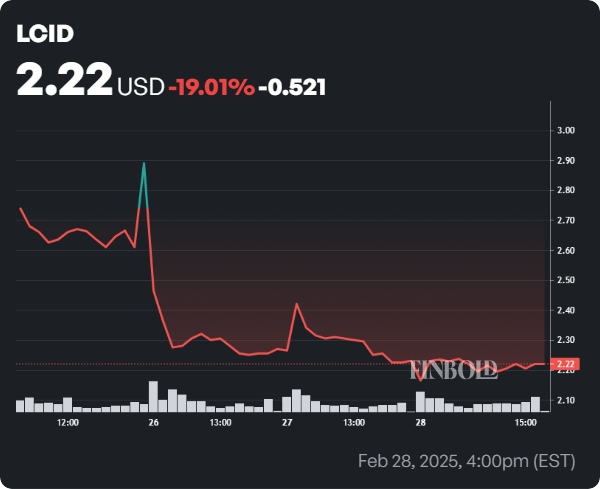

The electric vehicle maker’s (EV) shares tumbled 25.4% over the past week, closing at $2.22, with a year-to-date decline exceeding 26%. Still, LCID showed signs of life, climbing 1% to $2.24 in pre-market trading on March 3.

Why Lucid stock is crashing

The decline erased hopes of holding above the $3 resistance level, fueled by news of CEO Peter Rawlinson’s unexpected exit after steering Lucid through its Initial Public Offering (IPO) and Air model launches. The shift to an interim CEO has spooked investors.

Picks for you

Additionally, bearish sentiments seem to have engulfed investors despite Lucid’s claim that production capacity isn’t a concern after its Q4 2024 production of just 3,099 vehicles.

Indeed, the company is planning to double production in 2025, but there is no clear evidence that Lucid has the capacity to meet the targets.

Financially, Lucid’s 2024 revenue rose to $807 million from $595 million in 2023, though it still posted a staggering $2.7 billion net loss.

While Lucid is facing a challenging period, the firm is potentially banking on key fundamentals, such as strong financial backing, sufficient cash to sustain operations through 2026, and support from Saudi Arabia’s Public Investment Fund (PIF), reducing bankruptcy risk.

The upcoming launch of the Gravity SUV could also attract more customers and boost revenue, making Lucid stock a possible bargain.

Wall Street sets LCID stock price

Meanwhile, Wall Street analysts at TipRanks project modest gains for Lucid over the next 12 months. Specifically, a consensus of nine analysts predicts that LCID stock will trade at an average price of $2.39, a 7.66% increase from its last close.

The highest forecast is $5, while the lowest projects LCID at $1 within the next year.

The average rating for LCID stock is ‘Moderate Sell,’ with four analysts recommending ‘Sell’ while only one sees Lucid as a ‘Buy.’

Among the analysts, Stifel experts on February 27 lowered Lucid’s price target from $3.50 to $3, maintaining a ‘Hold’ rating. The revision reflects concerns over the luxury EV maker’s financials, including a -132.4% gross profit margin and high cash burn.

The analysts pointed to the Gravity SUV and a mid-size platform launching in 2026 as key to Lucid’s long-term success, potentially expanding its market and improving profitability.

A similar bearish outlook came from Redburn-Atlantic on February 24, which downgraded Lucid from ‘Neutral’ to ‘Sell’ and slashed the price target from $3.50 to $1.13. Analyst Tobias Beith noted that while Lucid’s engineering efficiency is a strength, competitors may surpass it by 2030. He pointed to challenges in scaling production, cash flow issues, high vehicle costs, and difficulty securing funding, suggesting significant capital may be required.

Finally, BofA Securities downgraded Lucid stock to ‘Underperform’ from ‘Neutral’ while slashing its price target from $3 to $1. This update was prompted by concerns over Lucid’s ability to deliver future products, which may impact its longer-term volume projections.

Featured image via Shutterstock