In 1970, the American singer-songwriter Edwin Starr released a song titled “War,” in which he concluded that is, in fact, good for absolutely nothing. Despite this popular stance, the five decades since have seemingly proven that war is, in fact, quite good for several things, including the market performance of the so-called “war stocks.”

Despite this perception and U.S. officials’ propensity for trading these shares – sometimes even making highly suspicious investments – war hasn’t been entirely profitable for investors keen on companies like Boeing (NYSE: BA), Lockheed-Martin (NYSE: LMT), Raytheon (NYSE: RTX), or Northrop-Grumman (NYSE: NOC).

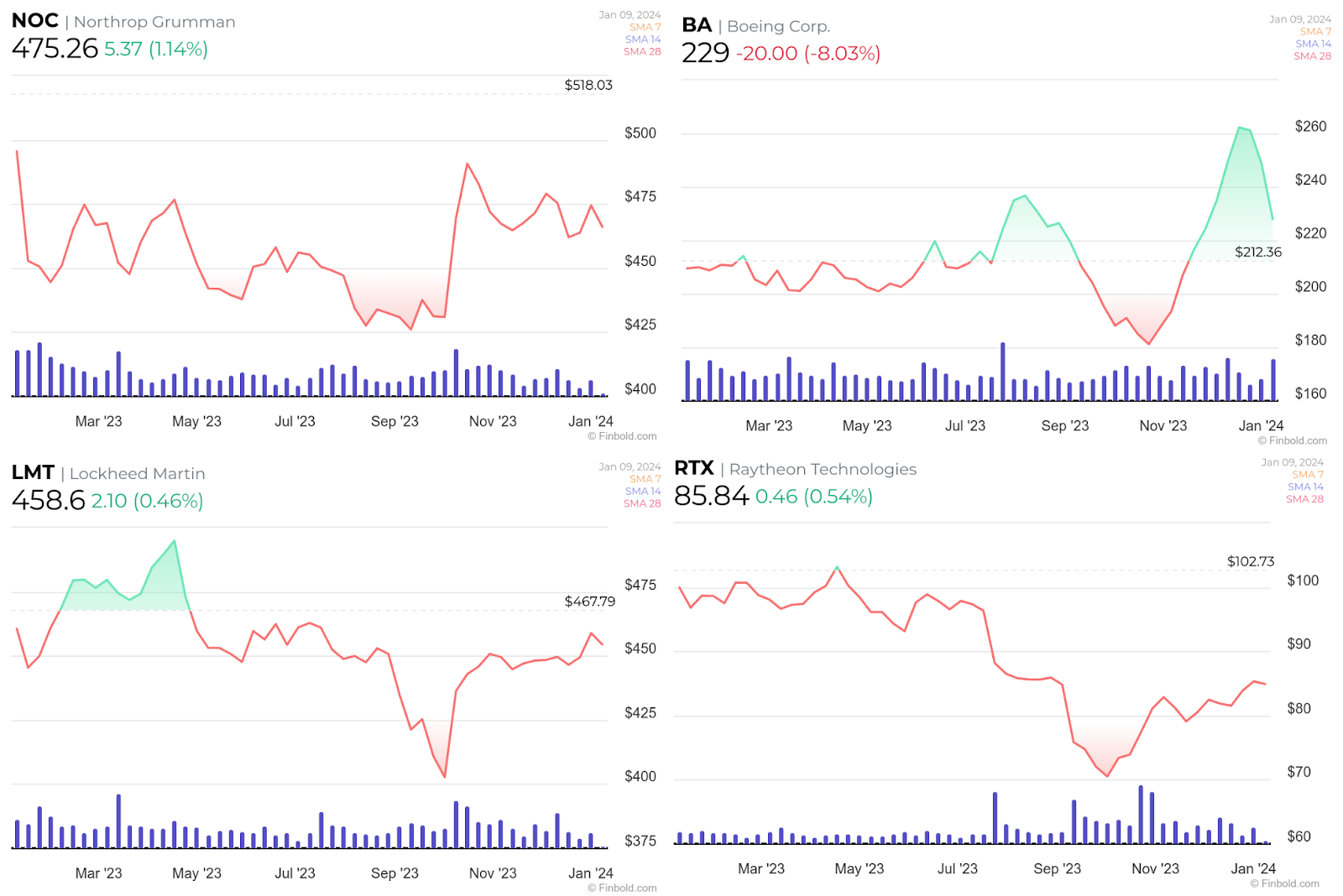

5-year trends of U.S. defense stocks

Out of the four most favored defense companies among American representatives, only Boeing has been, in the last 52 weeks, in the green. Furthermore, even the aeronautics giant is likely to continue losing ground following an alarming January 5 incident on Alaska Airlines Flight 1282.

Zooming further out to the last 5 years, several key trends can be identified. The four major companies experienced sharp and significant declines as the U.S. withdrawal from Afghanistan began in February 2020. They also almost universally started rising in the immediate aftermath of the Russian invasion of Ukraine but became either relatively stagnant or started declining in the summer months of 2022.

All four reignited their rise amidst the intense Russian rocket attacks in late 2022 but universally underwent major downturns as the Ukrainian summer counter-offensive of 2023 was called off with – at best – limited results, only to surge again following the October 7, 2023, Hamas attack on Israel.

At the surface level, such performance might indicate that these stocks react strongly to singular major events but soon lose steam – as is, indeed, a common criticism of U.S. public support for conflicts dating back to the end of the Second World War.

However, it is notable that the four war stocks also adhere relatively closely to the trends observable in the broader market throughout the 5-year period.

Their uptrends and downtrends also largely coincide with other major market-moving events, such as the COVID-19 pandemic, high inflation and interest rates, and a broader market rally observed with stocks and cryptocurrencies in late 2023.

Ultimately, it might appear that, despite the broad perception, investors in war stocks don’t profit nearly as much from conflict as is generally assumed.

Will U.S. defense stocks lose ground if more conflicts erupt?

Moral qualms and past performance aside, it is possible that, despite popular perception, the current decisions to supply Israeli and Ukrainian arsenals, as well as the need to restock the warehouses of other U.S. allies, might ultimately hurt major defense companies.

A crucial element behind their influence – and a justification for their high prices relative to Russian and Chinese manufacturers – is their reputation for designing and producing high-quality, cutting-edge equipment.

Recent years have put something of a dent in this reputation, as is evidenced by multiple reports that cast doubt on the efficacy of famous systems such as Patriot missile launchers with one Foreign Policy article from 2018 even calling it a “lemon.”

Similar allegations about high failure rates – especially given the high price tag of each individual missile – also emerged during the Russian aerial campaign of late 2022 and early 2023 – though the exact statistics are unlikely to be known for at least 20-100 years if the official records ever get declassified.

Are Western defense companies losing the qualitative edge?

Although not American, the well-regarded German Leopard tanks have suffered high attrition rates in Ukraine, and delivered U.S. Abrams tanks are yet to be seen on the front lines en masse for undisclosed reasons – though some have speculated that high maintenance costs or vulnerability to attacks by low-cost drones can explain their absence.

Other reports have cast doubt on the actual current technological advantage of Western defense industry giants. Perhaps the most bizarre of these are the allegations that drones of unknown origin have so far managed to monitor Bundewehr’s training facilities undisturbed since at least 2022.

Ultimately, the fog of war and other security concerns makes anything other than speculating difficult, and alarmism based on attrition or anomalous events is generally ill-advised, given that war guarantees a high human and material cost.

Still, given the recent trends, it is not unlikely that the reputation of major defense industry firms – and their stock market performance, by extension – might suffer dearly in the coming years.

Buy stocks now with Interactive Brokers – the most advanced investment platform

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.