As equity markets move deeper into 2026, more stocks are showing potential to join the $1 trillion club despite recent volatility.

Notably, several candidates are supported by strong fundamentals, including earnings momentum, sector-specific tailwinds, and near-term catalysts.

These factors align with broader market optimism that equities could push to new highs in the coming weeks.

Against this backdrop, Finbold has identified two stocks that could reach the $1 trillion market-cap milestone by the end of March.

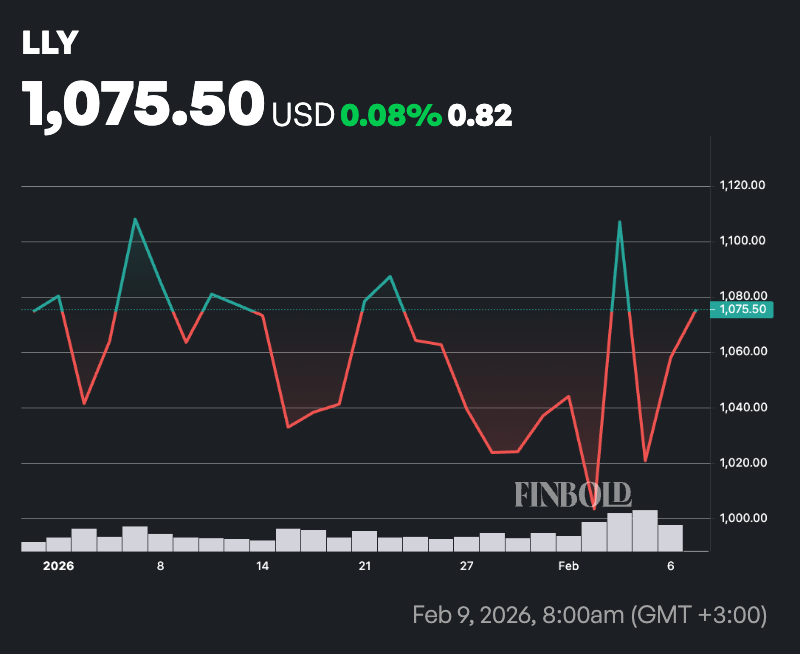

Eli Lilly (NYSE: LLY)

Eli Lilly (NYSE: LLY) is the closest candidate, with a market capitalization of about $948.6 billion. It needs a gain of roughly 5.4% to reach $1 trillion.

The stock’s growth is being driven by accelerating demand for its GLP-1 portfolio, led by Mounjaro for diabetes and Zepbound for obesity. Recent results showed revenue growth of more than 40% year over year, while management issued 2026 revenue guidance of $80 billion to $83 billion, well above market expectations.

That outlook reflects expanded supply, improved manufacturing capacity, and broader insurance coverage for weight-loss treatments, easing earlier bottlenecks.

At the same time, Eli Lilly’s late-stage pipeline is boosting investor confidence. The oral GLP-1 candidate orforglipron is advancing through regulatory milestones and could expand the market by removing injections, while next-generation obesity treatments like retatrutide have posted strong clinical data, reinforcing expectations of sustained pricing power and market leadership amid rising competition.

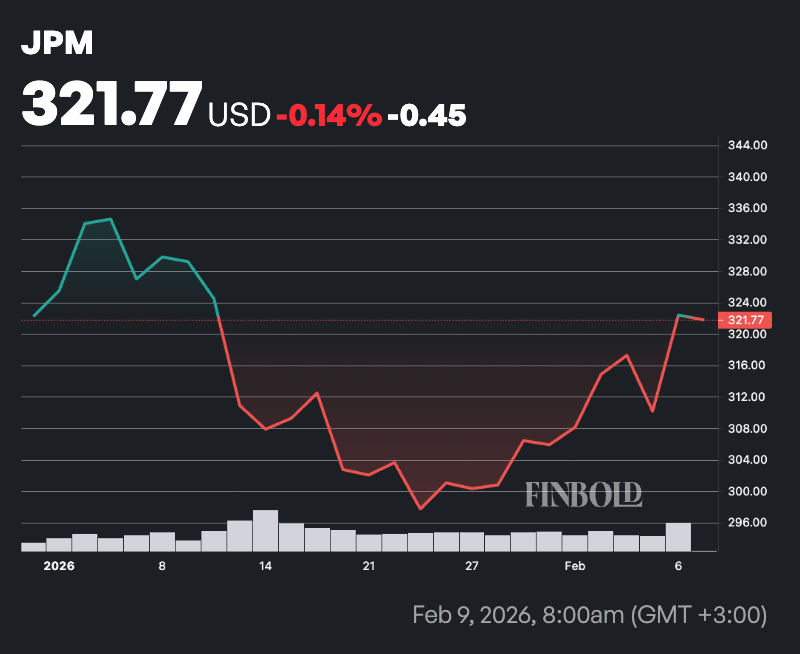

JPMorgan Chase (NYSE: JPM)

In second place, JPMorgan Chase (NYSE: JPM) is further from the milestone but remains the most credible trillion-dollar contender in the financial sector.

With a market capitalization of about $877.7 billion, the bank would need a gain of roughly 14% to reach $1 trillion. While larger, that move is achievable given JPMorgan’s scale, profitability, and leverage to macroeconomic trends.

The bank’s latest earnings showed strength across investment banking, trading, and consumer businesses, despite higher costs from technology spending and balance sheet adjustments.

Management expects expense pressures to ease as the year progresses, while revenues remain supported by steady market activity and stable credit conditions. Expectations for U.S. interest-rate cuts later in 2026 have also helped reduce concerns over net interest income volatility.

Meanwhile, capital returns remain a key support for JPMorgan’s valuation. In this case, potential Basel III regulatory relief could enable higher share buybacks and dividend growth, while continued investments in artificial intelligence and automation aim to improve efficiency as cost growth peaks.

Featured image via Shutterstock