As the first half of 2026 comes to a close, market leadership has shifted toward companies with direct exposure to some of the year’s strongest investment themes.

Strong demand tied to artificial intelligence, energy security, and capital spending has driven standout gains, while more consumer-dependent businesses have struggled to keep pace.

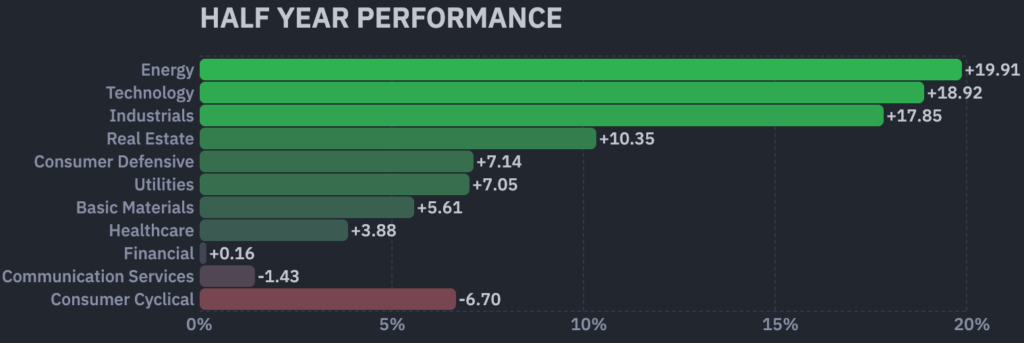

Sector performance data shows energy leading all major market groups with a gain of 19.91% through the first six months of 2026. The sector has benefited from higher oil prices and concerns over global supply disruptions.

Notably, crude prices rose amid tensions in the Middle East, boosting earnings for major producers such as ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX), while strong refining margins supported industry profits. Energy companies also benefited from growing electricity demand tied to AI data centers, increasing demand for energy infrastructure and services.

AI fuels technology sector rebound

Technology followed closely with an 18.92% return, fueled by continued investment in AI infrastructure, including semiconductors, cloud computing, and data centers. Strong spending by major technology companies boosted demand across the semiconductor supply chain, with hardware and infrastructure firms leading gains as investors favored businesses directly benefiting from the AI buildout.

Industrials gained 17.85%, making it the third-best-performing sector in 2026 so far. The sector benefited from spending on AI infrastructure, energy projects, manufacturing expansion, and defense programs, boosting demand for electrical equipment, power systems, and industrial machinery. Defense and aerospace companies also contributed to gains amid higher government spending and ongoing supply constraints in commercial aviation.

Real Estate gained 10.35% in the first half of the year, supported by improving credit conditions and expectations for stronger transaction activity. Consumer Defensive and Utilities posted gains of 7.14% and 7.05%, respectively, while Basic Materials rose 5.61% on the back of industrial activity and commodity demand. Healthcare advanced a more modest 3.88%.

Worst-performing stock sectors

At the other end of the market, consumer cyclical was the weakest-performing sector, falling 6.70% as higher borrowing costs, inflation concerns, and softer consumer sentiment weighed on discretionary spending. Communication Services declined 1.43%, while Financials were largely flat, gaining just 0.16%.

Overall, the first half of 2026 was marked by a shift toward sectors benefiting from AI investment, infrastructure spending, and energy-related tailwinds, while consumer-focused industries lagged amid ongoing economic pressures.

Whether that leadership persists in the second half will likely depend on commodity prices, AI spending trends, interest rate expectations, and broader economic conditions.