An expert has projected that the United States economy might be headed for a recession in the new year, with timing mostly hinging on a notable shift in the bond market.

Specifically, Samantha LaDuc, founder of LaDuc Capital and a macro-to-micro strategic technical analyst, highlighted the behavior of yield spreads—specifically the gap between short-term and long-term interest rates—as a crucial indicator of recession risk in an X post on December 28.

However, she clarified that the real concern isn’t when these spreads initially invert but rather when they shift back to a normal, positive slope, a process known as dis-inversion.

Indeed, her assessment was supported by data illustrating the relationship between yield curves and recession cycles, which have historically served as reliable indicators of impending economic slowdowns.

According to the data, there is a clear pattern: while yield inversions have often signaled recession risks, the shift back to favorable spreads—the dis-inversion—has consistently marked the beginning of recessions.

This normalization of the yield curve, according to LaDuc, is the true timing mechanism for when a recession is likely to begin. With this in mind, LaDuc projects that a recession could hit by the end of 2025.

“Recession tell- my bet: end of 2025. The problem – to market returns and jobs – is not when these spreads turn negative (invert), but when they dis-invert (turn positive), as this chart illustrates,” she said.

The recession might be here already

Similarly, Gordon Johnson of GLJ Research warned on December 17 that the U.S. economy may be nearing or is already in a recession despite a strong stock market.

He cited troubling labor market trends, noting that recessions often follow when unemployment exceeds its 36-month moving average. Johnson believes the economic challenges will emerge early in Donald Trump’s presidency.

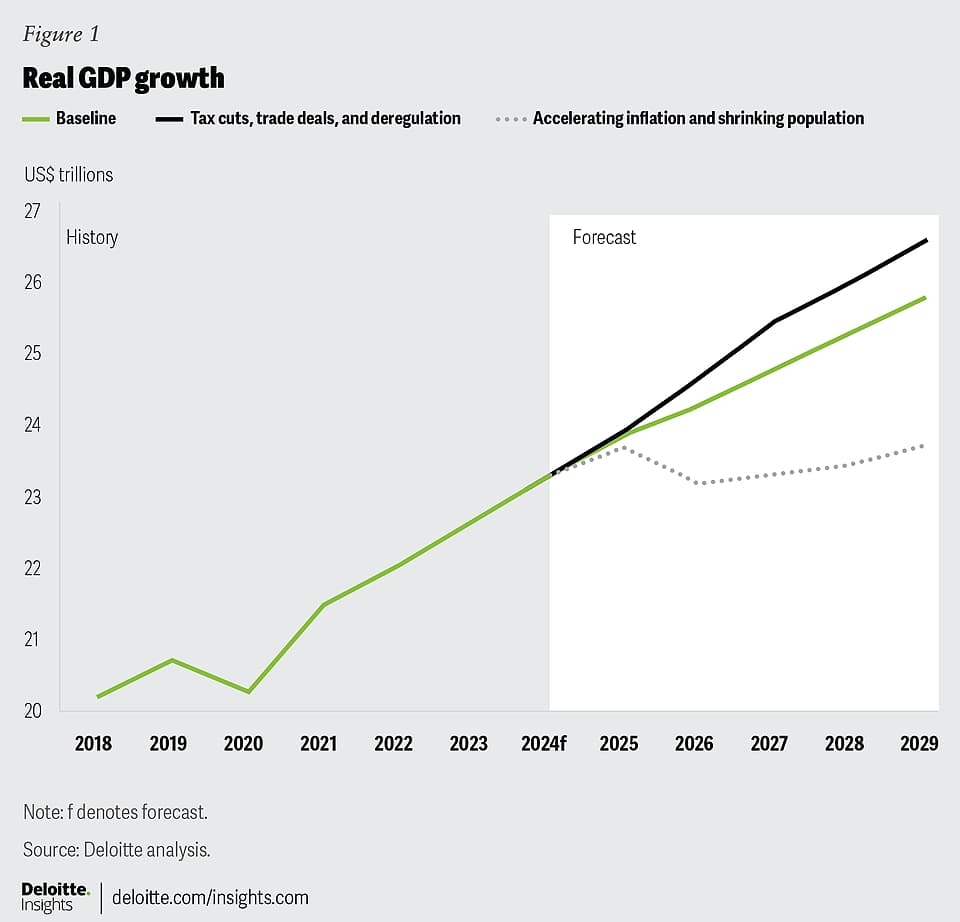

On the other hand, a recent report by Deloitte indicated that the likelihood of a U.S. recession depends on the incoming Trump administration’s policies.

In the baseline scenario (50%), moderate growth is expected, with GDP slowing from 2.4% in 2025 to 1.7% in 2026, but no recession.

The tax cuts and deregulation scenario (30%) predicts stronger growth, with GDP rising 2.7% annually, avoiding a recession altogether.

However, the firm noted that the inflation and shrinking population scenario (20%) poses the highest risk, forecasting a contraction of 2.1% in 2026 due to aggressive tariffs, deportations, and deep spending cuts, leading to a recession similar to those in 2009 and 2020.

Federal Reserve’s intervention

Fears of a possible recession in 2024 cooled down after the Federal Reserve moved to implement its first rate hike in about four years.

Interestingly, economist Henrik Zeberg has maintained that an economic crash is in store, warning that the Fed’s move is too late to rescue the economy. According to Zeberg, investors should anticipate the stock market and cryptocurrencies to hit record highs, which will usher in a collapse.

It’s worth noting that recent forecasts indicate an increasing possibility of a recession in the United States, with most analysts differing on the timing. However, individuals, such as author and investor Robert Kiyosaki, believe the crash is already here.

Conversely, some market observers argue that the chances of a recession in the United States are lower. According to an October Bank of America (BofA) Global Fund Manager Survey, most global investors don’t expect a hard landing in the next 12 months.

On the other hand, following strong September U.S. employment data, Goldman Sachs (NYSE: GS) reduced its recession forecast from 20% to 15%. Due to strong labor and retail data, the banking giant had previously raised recession risks to 25% in August but revised it back to 20%.

Featured image via Shutterstock