Alibaba (BABA) has announced the decision to halt the initial public offering (IPO) of its Freshippo grocery division and abandon plans to spin off a cloud unit.

The cloud unit, integral to Alibaba’s foray into generative artificial intelligence, has been a focal point for the company’s expansion efforts, but the company contributes its decision to the impact US regulations will have on exports of computing chips and semiconductor manufacturing equipment to China.

“We believe that these new restrictions may materially and adversely affect Cloud Intelligence Group’s ability to offer products and services and to perform under existing contracts, thereby negatively affecting our results of operations and financial condition,” the Chinese e-commerce giant said in a statement.

This development poses a significant challenge to Alibaba’s longstanding plan to divide into six separate entities, a strategy aimed at appeasing regulators in Beijing and driving growth.

Alibaba has also chosen to put an IPO of its Freshippo grocery division on hold to evaluate market conditions and other factors.

Despite this setback, Alibaba reported second-quarter adjusted earnings of 49.24 billion yuan (approximately $7.2 billion USD) and an 8.5% annual increase in revenue to 224.79 billion yuan (around $31 billion USD).

Additionally, the company unveiled its inaugural annual dividend, demonstrating its commitment to delivering shareholder returns, with a proposed cash payout of $1 per American depositary share.

This move, endorsed by the board of directors, will cost the company $2.5 billion.

Is Alibaba a buy now?

Since its IPO in 2014, Alibaba has experienced positive returns in December only twice.

The average return during the December periods has been negative 5.12%. This historical performance in the stock price suggests that the month has generally been challenging for Alibaba’s stock, with negative returns being the norm.

This could present an ample opportunity to acquire the stock just ahead of the festive season, potentially allowing for gains that could fund a delightful holiday at the beginning of 2024.

For those who believe in the business’s fundamentals, a strategy of holding for longer period can be a more suitable approach. However, it is crucial to maintain vigilance, taking into account the ongoing challenges faced by the company and the significant uncertainty that influences its future trajectory.

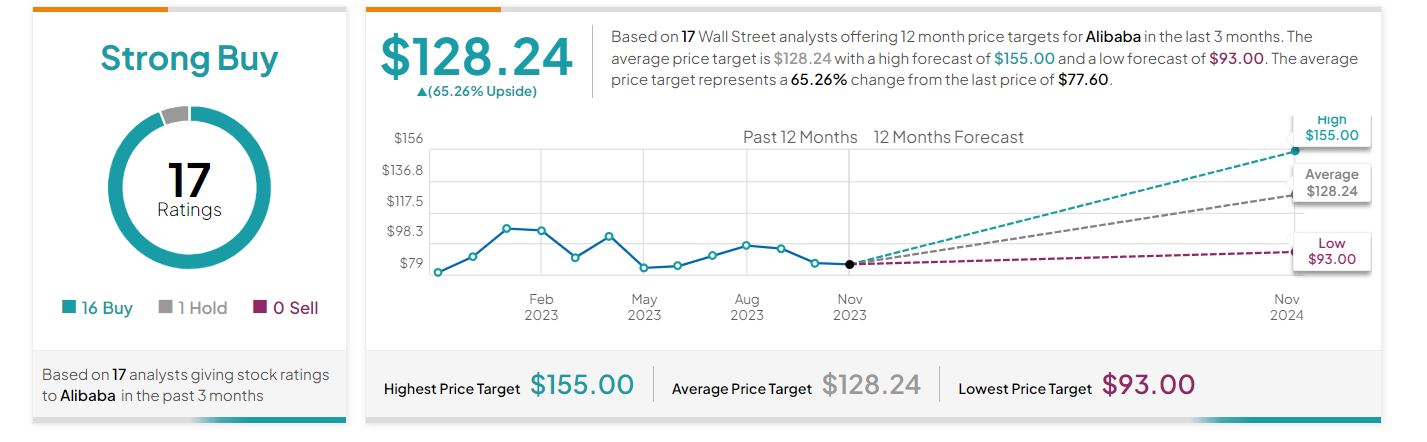

A synthesis of projections from 17 analysts on TipRanks over the previous quarter indicates a 12-month average price target of $128.24 for Alibaba. This suggests a potential upside of 75% from its current price, leading to an overarching strong buy recommendation. In the current month, Alibaba has received 16 Buy ratings, 1 Hold rating, and 0 Sell rating.

On a more positive note, the stock has the potential to reach $155, which would be a significant gain for investors.

Despite this positive outlook, the e-commerce giant, which surged during the early months of the COVID-19 pandemic, has disappointed investors, with its shares plummeting 74% since its all-time high in 2020.

Nevertheless, Alibaba experienced a 14% growth surge in the previous quarter.

Analysts are anticipating a return to the usual single-digit growth pattern in the upcoming reports, with projected earnings to increase by 10% and reach $2.11 per share. This aligns with the consistent trend of surpassing analyst profit targets observed in the company’s past performance.

Buy stocks now with Interactive Brokers – the most advanced investment platform

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk.